Ford Malaysia recently launched a special “Let’s Fiesta!” Chinese New Year promotion that will go on till February 28. The promo offers the chance to own a new Ford Fiesta from as low as RM588 per month, although monthly repayment does increase progressively by the year.

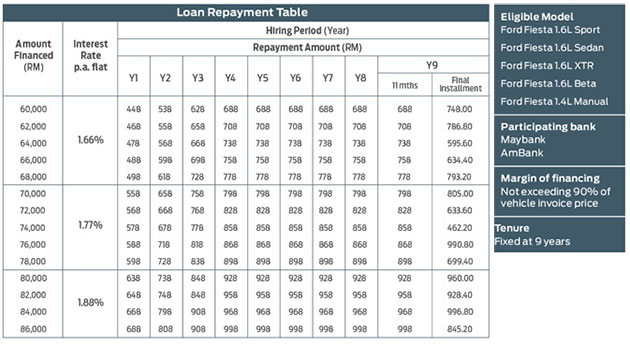

The RM588 per month calculation is based on the Fiesta 1.6L Sport (on-the-road with insurance in Peninsular Malaysia) with a nine-year financing period and RM76,000 loan amount. The margin of financing must not exceed 90% of the vehicle invoice price. Participating banks include Maybank and AmBank.

Buyers of the Fiesta get a five-year or 200,000 km warranty. For further peace-of-mind, new Fiestas also come with the Ford Extended Service Plan (ESP), a free service maintenance programme that covers parts and labour for up to three years or 60,000 km, whichever comes first.

Looking to sell your car? Sell it with Carro.

This isn’t for fresh gradute only ?

so many idiots here try to calculate.

hello its been stated on the chart clearly (MBB/AmB) as step up loan..

why waste ur time recalculate.

simple looo

no money no need to think.

u work get money

and buy laa…

spend ur money why keep.

keep2 also no point; u die end up ur kid/cucu get free from ur saving..

spend now.

enjoy life.

worry later.

money sure can find :)

9 years? Car rosak also still paying.

after 4th year, absorber start to kaput. engine mountings start to wear. oil seals start to show leakages.

paintwork full of scratches

car already depreciate but installment went higher instead. many ppl already regretted buying kia spectra and citra under similar scheme. its not worth it. only desparate car companies market their products like this. other than offering super long warranty or free services for 2 years. only 1 reason – they need to clear stocks before its too late without offering huge discounts

now they realized the 5 years plan by VW has getting result, and all non Japanese is moving towards that direction to get the market.

Honda is also giving 5 year warrenty for some of its models…..isn’t Honda Japanese?

5 years warranty?

Very, very …… Tempting

How are spare parts cost? Anyone knows

How is this a promotion?

Can i ask how is the monthly compared from 1st year till x year?

if its 10% dp then every month rm588 even on the 9th then its an irresistible promotion.

a promotion to those who appreciate and can afFORD.. get it?

how about ford focus titanium +? any promo for that?

unfortunately no.. can go to Ford Malaysia website to find out.

http://www.ford.net.my/promotions/promotion_cny.asp

This is a good car

588 x 108 = 63,504

Hurm…

LELONG>>>LELONG>>>>JUAL MURAH>>>LAMBAT TAK DAPAT

RM588 x 9 years x 12 months = RM63,504.00

Correct ah???

Halo. No such thing.. Total repayment is 88,000 include interest. 12,000 interest. For 588 starter package

10% downpayment for RM76K, means minimum RM68,400 loan. Even if its 9 years with 0% interest, the instalment is RM633 per month.

How come they come up with RM588? Unless if the buyer pays 30-40% upfront which most Malaysians cant afford to!

Correction, its RM76K loan max. If spread over 9 years, principal loan outstanding is RM703 per month and it doesn’t include with interest charges.

most probably first few years Rm 588, then skyrocket to RM 900+

Please look at the repayment table. It is first year 588, the rest is getting higher and higher

That’s odd. By my calculations, with MYR 76k loan amount, even with 0% annual interest, your monthly installment is closer to 650 MYR for a 9 year tenure. This must be a stepped installment payment. If not they’re losing money.

way to go captain obvious, next time read till the end before commenting something that is SO OBVIOUS!

Beware of 2 + 3, the last 3 is very difficult as it is insurance-based, and you know le this thing…

sounds like a good deal indeed…

This promotion is not the way it’s been understood.. You start paying RM588/month for the first year, then subsequently you’ll have to pay a higher instalment reaching RM900++/month at the 9th year…

As usual, cheating and fooling customers..

whats your problem?

The table shows what you need to pay the following year no? I dont think its their problem if people cant read.

Besides, the total amount you pay in interest works out the same anyway. Just that they let you pay less for the first year la.

they said is RM76k loan amount..even with 0% interest, every mth at least RM703.70 for 9 years..108 mths installment.

clearance stock before facelifted version arriving soon.

if you need a 9 year loan, you cant afford the car.

yes indeed, best is three, max’s five, don’t go for nine years, else later u’ll cry mother, cry father …. :P

This is not valid here in Malaysia where car prices does not tally with real economy. You’ll end with only 12 people buying cars.

Wahh..is it real..??if u cant afford 3 yers repayment than u cant afford that car..??

HOLYSHIT!! i can’t even afford a new Saga MT which is 38k…

Good, clear stock clear stock. Turbo faster come!

Yea man. Can’t wait for the Ecoboost engines.

read this guys….http://www.ford.net.my/promotions/promotion_cny.asp

Go to www.ford.net.my and take a look at the loan repayment table. It should help potential buyers to have a clearer picture of how much more to pay in the following years.

Is it really a good time to buy a new car? With GE13 coming and new NAP to be announced later?

I don’t think opposition will win, because of the most creative corrupted government. They are all in to win this election, with the help of corruption. The only way to win against this corrupted government is 80% of Malaysian vote against them. Want cheaper car, vote wisely.

remind me of fabuluos gym khana’s video with full mod ford fiesta ..now affordable at rm588….

IMHO, this is not a good deal and a very confusing / non-flat rate interest rate .

Here’s why. *Alert* Lots of math calculations ahead.

All calculations make use of OTR.

Let’s take the RM 588 installment. Working backward, with RM 76K being the 90% loan amount, that works out to selling price of RM 84,444. ( RM 76 K x (100/90)).

That points to the Fiesta 1.6 Sports hatchback, RM 84,888. So you put down payment of RM 8,888 (Wah ! Very Ong !), and that gives you RM 76 K loan amount.

Actual Total Interest Charged.

Let’s sum up the total amount to be paid.

Year 1, (RM 588 x 12) = RM 7,506

Year 2, (RM 718 x 12) = RM 8,616

Year 3, (RM 818 x 12) = RM 9,816

Year 4 – Year 9 (Month 1 – 11) ( RM 868 x 77) = RM 66,836

Year 9 (Month 12) = RM 990.80

GRAND TOTAL = RM 93,764.80

Thus Interest = RM 93,764.80 – RM 76,000 = RM 17,764.80

That interest is 23.38% of the loan amount, (RM 17,764.80 / RM 76,000), it being equivalent to FLAT rate interest of 2.60% per year, (23.38% / 9 years). The interest itself is very good. It’s not a bad deal.

However, the catch is the PERCENTAGE of increment from Year 1 – Year 4. Here’s the breakdown.

Year 1 – Year 2: ((RM 718 – RM 588) / RM 588) x 100% = 22.11%

Year 2 – Year 3: ((RM 818 – RM 718) / RM 718) x 100% = 13.93%

Year 3 – Year 4: ((RM 818 – RM 868) / RM 868) x 100% = 8.06%

How the above applies is your salary increment, (if there is one in the first place !), has to match the above raise the percentage above for the next 3 years ! If it doesn’t, you’re screwed ! What job and in what industry will give you an increment of 8% in 1 year, let alone 22% ?!

In short, take this offer if and only if you can afford to set aside the maximum installment amount, this case being RM 868, right from the start. Don’t go near this if you are not within 90% and above of this amount.

nice calculation….but got error.

Year 4 – year 9 (1-11th month) total is only 71 months and not 77 months.

Work harder maybe can get promoted? Then you are able to afford this.

Just want to highlight some errors (correct me if I’m wrong);

Total amount to be paid:

Year 1: RM588 x 12 months = RM7,056

Year 2: RM718 x 12 months = RM8,616

Year 3: RM818 x 12 months = RM9,816

Year 4-8: RM868 x 12 months x 5 years = RM52,080

Year 9: (RM868 x 11 months)+RM990.80 = RM10,538.80

Grand total = RM88,106.80

Hence,

Interest = RM88,106.80 – RM76,000 = RM12,106.80

That is 15.93% of the loan amount; which leads to an annual rate of 1.77% (same as advertised).

The percentage of annual increment:

Year 1-Year 2: [(RM718-RM588)/RM588)] x 100% = 22.11%

Year 2-Year 3: [(RM818-RM718)/RM718)] x 100% = 13.93%

Year 3-Year 4: [(RM868-RM818)/RM818)] x 100% = 6.11%

OMG…great deal for those who cant afford high loan for the begining years.

I just want to say

your analysis is AWESOME!

And paultan should consult your opinion if they have such articles again. Unless, it’s a paid article.. lol

There is actually another way to look at this.

The first few years lower instalment can offset for the higher insurance premium that needs to be paid, if one does not have NCB.

While towards the second half of the loan, car value dropped and NCB kicks in, resulting in much lower insurance costs, which can be contributed back to offset the rising monthly instalment payment.

can u help me with my business model and revenue model but i cannot pay much…probably belanja makan..serious ni..

nice analysis but to simply look at it, the increment is around rm 50 to rm 100+ per year. Most salary would increase more than that per year. So most people can afford this payment scheme. The disadvantage of this scheme is the loan amount deduction is less on early years. So this mean that if you want to sell the car in short time, this scheme is not good for you.

Pity Malaysian need to pay 9 years for this mini car.

Pity Malaysian, we has a world most creative corrupted government, ranking no. 1 for most creative and interesting corruption activities.

ya ya ya.. blame the government that u missed your monthly car loan for the car you can’t afFORD.

(if u have any)

This reminds me of the Volvo S40 promo in about 2005, first year payment Rm1188 etc than increasing gradually, but in the end useless, as the price discounted from RM188k to Rm169k if im correct..thats the problem with buying these ” cold stock” cars

a lot of the commentators seems to say 3yrs loan max, but honestly I ain’t gonna pay 2k a month on a car say, a Vios. Lets be realistic. I guess Alot just TKSS only, most of you fellas seem to say it because that’s what you wanna do not what you’re doing.

By the way my company pays for interest so makes no sense for me to take a shorter loan period.

Some of the comments here stating the conspicuously unbelievable 588 x 108 pricing is BEFORE paultan update the post with the complete repayment sheet.

Kinda misleading when this was first posted. Cheers.

..and i was wondering why are there so many people posting such funny remarks. thanks mr confused.

local financial always like ppl to caring burden forever , fixed 9 years Zzzzz

any improvement with the auto gearbox..comment at ford facebook page really make me think twice b4 buying this car…

Malaysia really corrupted. Even a small car like this need to pay 9 years installment. Time to change, not car, Government.

change ur mindset sir.. this is an automotive blog.

singing here wont do any good if you dont vote! make noise is easy, taking the responsibility to vote is another. dont just talk, use your right

They want to clear current stock to make way for the facelift version to be launched here soon. But taking 9 years to pay off a car is too long. Don’t do it.

Went to Ford show room today. Was told 1.4 manual no more stock. Was told 1.6 only left 1 colour.

Also, they said new stock coming in March 2013.

So, I thought I could book 1.4 manual but went home without anything. Ford, please don’t mislead us with the advertisement if you don’t have any car for the customer.

Also, was told there was no 7 airbag for 1.4 cc. Why their website and brochure printed with 7 airbags??

Seriously misleading !

I know it’s the norm here but paying 9 years for a car is silly. Even before you are halfway paying back the loan the market value of your car is below the balance of your loan.

At this stage it is cheaper to let the bank re-possess your car than pay back the loan if you want to change car. But in Bolehland you can’t just do that. The bank can sue you for the balance if they cannot recover the balance of loan from repossessing and selling your car.

Escalating instalment plan should be avoided. This assumes that your income will rise as you age but what if it doesn’t? Remember that inflation is also rising and you may have more expenses like eduction as your children grows. This is not the way to afford a car which you can’t afford now.

And yes, I agree with the comments of “poor Malaysians needing 9 years to pay off a small car”. Only in Bolehland.