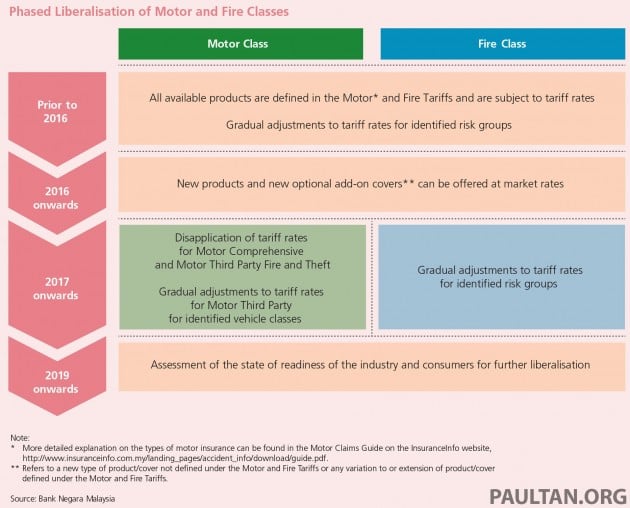

As announced in 2012, and reaffirmed in 2014, the liberalisation of motor insurance tariffs in Malaysia will commence from July 1, 2016. In short, motor insurance premiums will soon be based on a list of risk factors, instead of the current overly simplified and regulated pricing policy.

Bank Negara Malaysia (BNM) confirmed the move in its Financial Stability and Payment Systems Report 2015, released today. The report includes the roadmap towards the full liberalisation of motor insurance tariffs – a gradual move towards pricing of motor policies that is more reflective of risks.

To minimise the impact of the move (to both consumers and insurers), an orderly transition plan has been laid out. The existing insurance tariff requirements – relating to pricing and coverage limits – will be phased out, but not immediately. Refer to the diagrams below for the full roadmap.

In the first phase (the first year of implementation, starting July 1), the industry will be allowed to offer “new products” and optional add-on covers at market rates. This can include, for example, additional policies to cover engine hydro-lock (water entering the engine in lightly flooded areas, separated out from the currently costly flood damage insurance), lost car key replacement, and perhaps even the availability of courtesy cars.

Prices of these new products will not be regulated, and as such will be determined by the market. Insurance providers will be open to price them as they see fit, to attract consumers. This will provide an early platform for insurers to refine their offerings and pricing policy, while consumers get additional choices to fit their individual needs.

The second phase (2017 onwards) will see the disapplication of tariff rates for comprehensive and third party motor insurance. Here, premium rates will no longer be regulated, and will be determined by the market. Risk-based assessments will also be introduced in Malaysia.

As such, various risk factors not included in the current motor tariff, such as residence location, vehicle make and model, use of vehicle, occupation of owner, claims history, gender and age will be taken into consideration, similar to the system employed in countries like the UK.

In other words, the insurance premium rates you pay will depend on how much risk you are perceived to carry – for instance, owners of makes and models with high repair costs, owners of high-performance vehicles, owners with fewer years of driving experience or those who live in crime-prone areas may have to pay higher premiums. And the rates offered to you will not be regulated, so prices may vary across different insurance providers.

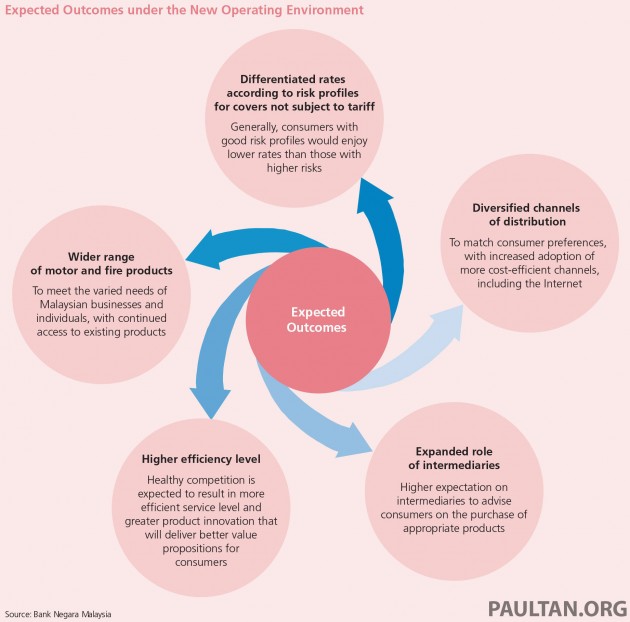

Enhancements to consumer protection will also be introduced, to ensure proper governance over product design and pricing. Insurers are expected to assess the risks appropriately and consistently for fair treatment of consumers. The standard scope of coverage disclosure will be increased, so consumers can easily compare between insurers to make informed purchasing decisions.

However, this will not apply to third-party insurance of certain identified vehicle classes. Premium rates for these classes (unspecified as of yet) will continue to be regulated, with gradual adjustments to be made.

It’s said that currently, there’s a large discrepancy between third-party insurance premium collection (RM520 million) and the incurred claims and expenses of these classes (RM680 million). Given the sizable pricing gap relative to risk, a full deregulation of rates will inevitably result in steep premium increases. Thus, a more measured approach is being taken for these vehicles classes (third-party insurance).

The move to liberalise the motor insurance market is expected to provide greater pricing flexibility between insurance providers, which will promote competition between them. Consumers will largely benefit from this open market, with insurers competing to offer better coverage, services and of course, pricing. More streamlined practices will also minimise delays in claims settlements.

In the long run, vehicle owners with lower risk profiles will be charged lower premium rates, while those with higher risk profiles will be properly incentivised to undertake measures to reduce their risk exposures. Consumers will also be open to customise the coverage limits or purchase optional extensions as they please – pay less for lower coverage, or pay more for a more comprehensive policy.

Looking to sell your car? Sell it with Carro.

Guess everybody like to pay fr more these days without any complaints…i’m sure more high risk will be recorded vs low risk

No matter of high risk low risk… its suppose to be have another roadmap prior this. The vehicle makers & dealers should allow buyers to CONFIGURE own accessories to serve the individual needs.

Most users need only 2 major items:- (1)safety features like ABS w/ BA, VSC, TC, etc… (2)Navigation. Which should come standard. ANY OTHERS SHOULD BE OPTIONAL. Such as lamp type upgrade, body kits installation, remove radio set if the radio set available not meet your taste; etc…

Insurance company cannot control what automakers configure on their vehicles.

Configuring features based on individual need means more cost and time involved

This new system which will raise tariffs and premiums is because Insurance companies cannot sort out their own fraud which they know exist.

To all the insurance companies, pls don’t pretend to be innocent. You all know damn well that every adjuster of yours is working hand in hand with the police, investigation officer and the car workshop to get kickbacks. I myself had many accidents.

Infact the last accident I had, I sent my car to my own friend workshop, he said he will repair everything for RM1000. I tried another workshop, he assessed the repair to about RM1200. I thought, nevermind, I will send for insurance claim and I can save the RM1000.

So, I sent the car to the panel workshop. After repairs and all that, out of curiosity, I simply called the insurance company up to find out how much was the bill, it was shockingly RM8000. Yes, 8x the actual amount if I had the car repaired by myself.

We all know what happens. The IO (Investigating Officer), the Adjuster, as well as the bengkel and the ulat ulat runner boys will get their kickback. Biggest kickback would be the adjuster. At least he makan few thousand for his personal pocket.

The Insurance companies know about all this. Hundreds of cases happen everday. But they close an eye. They pass the problem and burden to the consumer with higher premiums.

Zeti of BNM, you know this happens but you too close an eye. This results in higher burden and premiums for the public and now, this new system, which is utter bogus.

Bank Negara, please read the above. I repeat, you also know about all this. But BNM just keep quiet. You all just close an eye because the problem now goes back to the consumer with higher premiums.

With all this shit going on the Insurance industry dare to increase the car premiums for the motor industry every year and now, do this system which will make them more money.

That is Malaysia for you. The rakyat suffer the most because there is no proper enforcement and the insurance industry is full of cheats.

Everybody suffers when everybody along the line gets kickbacks from the police office, the police cameraman, the adjuster, the bengkel and the runner boys (ulat ulat).

The Motor Insurance Industry collected no less than RM100 billion in premiums last year. It is not fair that we public have to pay higher premiums because they cannot sort out the fraud in their own backyard.

You should report it to police and MACC..then if you lost trust in them..not much you can do…

Partially agree. But do you think Insurance campanies (IO) feel happy when they pay the claims to workshops for the above case you mentioned?. They (IO) will review the quotations from several panel workshops as well. They will not blindly accept everything what adjusters assessed. Somtimes IO will blacklist crooks workshops and end up with molotov cocktails thrown at their house’s porch. Something to ponder. Report to BNM??? No. The Police??? Yes. And no further investigation. Business as usual for all.

This’s a SCAM from MIT in Malaysia, Malaysia car price are sky high yet Government helping AP cronies to “increase the price more’??? by premium the insurance…

Better if the insurance can cover RV lost! Sounds like a-must-have coverage for Very Worrying (V.W.)

That is called GAP insurance.

useless, Those good drivers NCB ??? NO CLAIMED SINCE DRIVING / How ?? bonus ??? ti[pu insurance i dont know.

Im sure bashers will soon say ini mesti semua salah ….. even though its their own fault for driving like a suicidal maniac bent on taking others with them to afterlife

Risk of riding bike is higher compare to driving a car. So do driving proton more likely to die in accident than driving a Infinity. Then raise the life insurance premium too.. pkmak!

Older proton Yes, But compare the Myvi to the iriz, Myvi kompem die lenyek one.

Do u own an iriz and had an accident with a myvi? How can u be so certain of this??

If compare current toyota with current P1, konpem toyota become from moving coffin to final coffin.

Say NO toyota, say NO to moving coffin!

How about claim due to lost car or car being banged without knowledge.

Anybody supporting this new sys or think this is a good move well wait till you have to pay more…welcome to the new era mf kers

Veterans like us should be honoured with low premiums with sensible driving. Must take into account diseases suffered as well.

OMG so complicated..no airbags very high risk? if airbags using TAKATA airbags even Higher Risk right?? Run-flat tyres and Ceramic brake would reduce risk?

must buy expensive cars before July…that’s for sure. correct move anyway as our cars insurance premium among the lowest in the region, but motor insurance claims among the world highest!!!!

so everybody in the region implement something shitty (like gst), we implement also is it? and because other people claim excessively and insurance company cannot control their own adjuster, i have to pay more is it? good move.

Sound good to me, as long as year of the car are not been defined as a risk factor. Maybe a car condition, if needed, probably better.

If u a regular motorist in the Klang Valley u can easily knw some class or brands of cars tend to be driven recklessly…inc Hilux, all Prodon models, Perodua, Vios (especially those bought 2nd hand), pickup trucks and big luxury vans eg Alphard and VW Golf Passat and Fiesta

But luckily Proton not, since u only mention Prodon.

Nice generalisation, I bet you generalise races too

“Gradual adjustments to tariff rates for Motor Third Party for identified vehicle classes” – makes you wonder if this is a way for Malaysia Automotive Institute (MAI) to fast-track their car scrappage programme, by making it financially difficult to insure classic cars.

After 1 July for sure insurance premium will go up up up!

I believe there will be a price war n rates will go down

basically if your male and below 25 years old driving a modified sports car you’re insurance premium will by sky high…

imagine in the uk mod add turbo charge premium goes up by 132%

upgrade suspension +25%

bodykit +57%

how many insurance companies are in the UK? 250

Malaysia? probably less than 30

Car prices in UK? How much vs car prices in malaysia.

The car is cheap, if u only intend to keep it in ur garage. Otherwise running the car when ur young is even more expensive than total car ownership in MY. Not to mention repair cannot be done by ur mudguard lou under the tree

This will cause the low risk drivers to be in loosing end and much the same for insurance company. The blacklisted drivers will just continue drive WITHOUT insurance. Why do you think the number of uninsured vehicles & drivers are increasing high on upward trend? They bang into you & run away cannot be traced. You cant sue the driver caused its not registered & previous owner no longer owns it.

more nonsense by insurance companies to earn more

Why pass the blame to the insurer. The premium calculated based more on claims incurred rather than profit earning. Are you aware so many cars stolen everyday.Compare your premium paid against the claim on stolen car. example RM 3,000 for RM 200,000 vellfire. Obviously car with anti theft and tracking device pay less compare to none. Isn`t it fair to the insurer and consumer?

Ahya, All money suckers. Always help the insurance company profit. Not all old cars are high risk. Loading, loadings, Check lot of less than 5 years car involved in accidents ,if not wrong. also, driving fast is not the cause of accidents. Most important, Alert n concentration while on driving. No hand phone, Change channels or radio. take things. Be alert , and look far.

Higher risk residence location = lower income areas = higher rates?

What about the Betterment Clause on cars greater than.5years old???

I believe even the lowest risker will pay more premium than nowadays premium……another strategy to suck citizen money….

maybe in a market with many players you could probably expect lower rates but in malaysia, it just be a cartel fixing up prices so they could slaughter us nicely..hopeful but in doubt

First business is to charge skyhigh premiums for moving coffins like toyotas & P2. Then watch SL beg his jepunis overlords for VSC, TC & 6 airbags

Typical la. Cronies are queueing up for their turn.

Civic Turbo and VW owners will have a hard time starting July.

The only people they’ll categorise as low risk are stay at home adults who are healthy and take their cars out just once a week. The rest are high risk.

With a downward market trend, add this on top, good luck to sales.

Unreliable cars insurance premium like Protons and VWs must be sky high.

obviously soon, everyone will be using in car cams

at least young rich punk driving around in merc, bmw, feraris will hv to pay more

Urmm, the car might be registered in the father’s name, and address in an exclusive neighbourhood. Imagine if dad is 50 years old, and CEO of a company. Premium would be very low. Unless they charge premiums based on horsepower (which they should)

hilux sure attracts higher insurance premium since lack of safety features compared to other trucks

Some companies don’t even insure hilux due to high prone of theft

Female drivers are high risk. Female drivers in Peroduas should be put at highest risk.

Male Proton drivers and Government servants should be at lowest risk.

Cars with automatic transmission should be put at high risk as well. Most vehicles in accidents are automatics.

In countries with risk based insurance, Female drivers enjoy better (in much cases, MUCH better) rates.

While female drivers may get into accidents, they usually are small fender benders. Men on the other hand does it in style with BIG accidents. Which do you think is more expensive?

So eat your heart out the day when you consider putting your self as 2nd driver under your significant other’s drivers insurance.

please raise everything ASAP! don’t wait until July bro, i know that most of insurance agent have no patient to book their porsche, bmw, lambo, bla bla bla…

So a woman (women live longer and are theoretically safer drivers), has 2 kids (so must be responsible), works as an accountant (again, a responsible person), drives a Volvo (with all the safety prevention and airbags,etc) and address of the car is in Putrajaya (doesn’t actually have to live there though), that means insurance must be very low correct? What this could mean is cheaper cars (of course can’t even come close to safety of a Volvo) will end up having higher premium. A 23 year old person, first job, no kids, drives a Myvi (thats all he can afford), lives in Puchong (cos thats all he can afford) will pay sky high premiums. Don’t forget to add 6% GST after that, thank you very much. How is he going to afford paying for the hire purchase and premium? Things are gonna get even more expensive in the coming year. Lucky petrol is “cheap” for now.

More ingenious ways of sucking money from the poor rakyat.

Rates will go up. Regardless of whether you are high risk or low risk. This is the nature of things. But if you are high risk, your rates will go up A LOT.

If I were to take a guess.

1) Proton/Perodua cars will be more expensive to insure (just like why interest rates are higher)

2) Older cars will be more expensive to insure. Those like me which have a few old cars in the stables will sweat bullets.

3) Metropolitan residents (IE. KV, Penang, JB) will be more expensive

4) shared parking (ie condo)/ street parking will be more expensive.

5) Young drivers…much more expensive..goes without saying

6) Cars without ESC, airbags will be more expensive

7) Those that drive for work – (ie. Salesmen) or those that commute long distance.

8) Performance or modified vehicles will be more expensive by a lot. Dream about owning a cheap used sportscar. Forget it.

9) Theft prone cars will go up. Own a Hilux? Good luck.

And if you have any prior convictions, forget about driving and take public transportation.

I have dealt with these sort of risk based insurance before. If you are a young driver, your insurance premiums may end up more expensive than the car.

The ONLY good thing I can see if that people may be slightly safer and cars with poor safety equipment will not sell. Otherwise it’s a bag of nightmares waiting to be unleashed.

For the record, I’m not against risk based insurance. But -in my opinion. The country isn’t ready for risk based insurance. At least not until;

1) Our disposable income increases

2) Cars are cheaper so we can change cars with better safety

3) We lack a comprehensive public transportation system that allows for alternatives for those priced out of car ownership.

Besides, our existing insurance is NOT Cheap (due to the overinflated value of our cars), contrary to what most think. Take away NCB and the costs are quite high relative to our income.

Well said and nicely summed up man 4G63T DSM. You nailed it far better than I could have ! haha

I especially agree with your second to last paragraph; indeed, Malaysia is not yet ready for this kind of customized motor insurance. As far as I know, it’s been long since used in the U.K. and many other developed countries, but we’re simply not at their level yet. This is fundamentally different from the recent emissions-based tax in Thailand, because emissions tax depends on the car, not the drivers. Even the end-of-life scrapping scheme is not driver-reliant. Any price hikes due to 5-star ASEAN NCAP compliance (or ESC as standard) will also be a car-reliant increase.

This is why I’m worried and a bit apprehensive about this new risk-based insurance policy. For once, the customer has become the topic of debate, together with the cars themselves. Malaysians must be able to see this.

Is there any insurance for my current insurance?

Your car premium will be higher if :-

1. Car parked outside of the house.

2. Parked tepi longkang.

3. Owner stays at non-guarded housing area.

4. Your taman have kids playing outdoors.

5. Your car have 4 tyres.

And finally

6. If bird s*it on your car.

Last year premium increased because of the GST. This year going to increase because of this BS. Next year?

Why dont the NCD are increasing? Why dont you increase it to 70-80% instead of 55%?

If you IDIOTS cant come up with ideas to ease our(THE RAKYATS) living, please dont come up with the ideas that ease their(THOSE CRONIES) living.

What about insurance for commercial vehicles; lorries, buses and vans? They need to cover extensively the ‘victims’ when they get into accidents or bang into other people. The heavy vehicle drivers are the worst offenders; always hogging the middle and fast lanes, overloading, brake failure, bang into cars parked by the roadside, gelek the motorcyclists and pedestrians, lorry hantu, etc. etc. These people somehow seem to get away very lightly as if they have some kind of protection.

I believe this system is not compitable to be implemented in Malaysia yet. They have to consider all factors, incl wages, cost of living, excess surplus, etc etc. Plus malaysian already paid premium (ridiculously high price) for our cars.

no longer be regulated? how to prevent collusion amongst competitors? just like whats happening in telco biz now.

This is mostly bad news for us Malaysians, but it was only a matter or time. It’s true, our motor insurance regulations are extremely primitive, and some of us end up subsidising others. By nature, certain types of cars are always cheaper or more expensive to insure than others for many externally dependent reasons.

For example, any hot hatch or performance car will have higher insurance rates. This is because insurance companies know that the type of people who buy hot hatches are not exactly known for safe driving. On the other hand, cars that older people like to drive, Toyotas and Nissans, these cars will have lower insurance rates, because their buying demographic tend to emphasise and value safety and order.

Speaking about safety, insurance companies also assess the safety features of a car. This means a car with ABS, ESC and 6 airbags will have a lower insurance rate than an exact same model without ABS, ESC and only 2 airbags. ABS and ESC have been universally proven to reduce the chances of accidents occurring in the first place, and more airbags mean that if an accident occurs, the occupants will have higher chances of surviving. A dead customer is no good for insurance companies, if they lose you, they lose money !

If you drive an older car, expect insurance rates to go up. This is because insurance companies know that old cars are more prone to age-related mechanical problems that could raise the chances of an accident occurring. Most old cars are also extremely unsafe, many don’t even have a single airbag or ABS.

These are just a few aspects I’ve touched on, there’s a whole bunch of other stuff that Western countries/ Japan considers in motor insurance. In a nutshell, this is not entirely bad, but rather, it is bad for most and good for some. Basically, if you drive a new 5-star safety rated car, you can sleep comfortably… if you drive an old car, an Axia, Myvi or Saga… then you have reason to worry.

Conclusion is what ever new system they introduce will result in higher premium. Another strike by our beloved gov. Thank you guys…. i luv u all…

The way I see it – the rich will pay less whereas the poor will pay more. Do we really need to widen the income gap further? Is this policy even prudent for the long term?

Take away the colourful and bombastic words, NO where is it stated in the Road Map that comprehensive motor insurance for cars will BE REDUCED. In fact if you read the announcement carefully, it is the insurance companies desire to protect themselves by cut down excessive claims and frauds in adjusting the tariffs. And they are talking about THIRD PARTY INSURANCE AND FIRE INSURANCE where the insurance companies make the most losses. And they have an escape clause that they can exercise in 2019 just in the case the insurance companies get screwed by their own rules. There’s nothing good or joyful for the normal motorists. In fact you be damned by higher insurance premiums with colourful and bombastic English. Wake up guys, the insurance companies want guaranteed profits without the risks !!!!!

I’m believe we are cheated, as today found out the new calculation higher than old calculation RM100 – RM 200 pay extra. The calculation not transparent at all. Truly Liar~~~