We’re now at the Matrade Exhibition and Convention Centre, where MITI is announcing the National Automotive Policy (NAP 2014) very soon. Keep refreshing the page for live updates.

– The Minister has arrived. He has started his speech.

– TIV for Malaysia 627,753 in 2012, 652,120 in 2013, forecast is 670,000 units in 2014.

– For 2013, export is less than RM1 billion worth of passenger cars. Import cars RM9-10 billion.

– 550,000 people reliant on industry – 250,000 manufacturing, 300,000 aftermarket

– Motorisation level in Malaysia is 361 cars for every 1,000 people. Meanwhile, Indonesia is 21 per 1,000, Thailand is 157 (2013).

– Thai Eco Car and Indonesian LCGC policies taken as comparison.

– Auto industry contributed RM30 billion to national GDP in 2013.

Objectives of NAP 2014:

– promote competitive and sustainable domestic auto industry including national auto companies.

– make Malaysia regional hub in energy efficient vehicles (EEV).

– promote increase in value-added activities in a sustainable manner.

– promote increase in exports of vehicles and auto components.

– promote participation of Bumiputera companies in total value chain of domestic auto industry.

– safeguard consumers interest by offering safer better quality products.

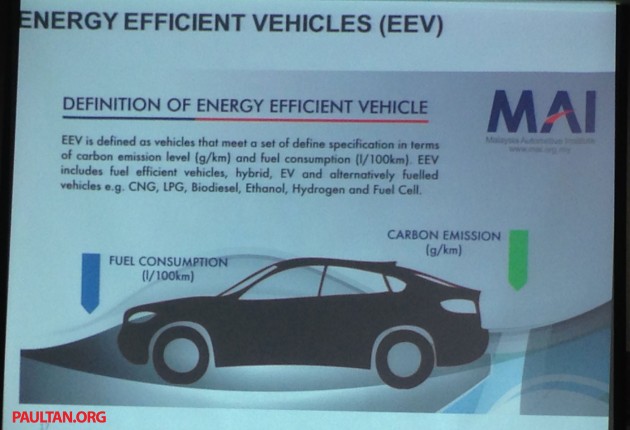

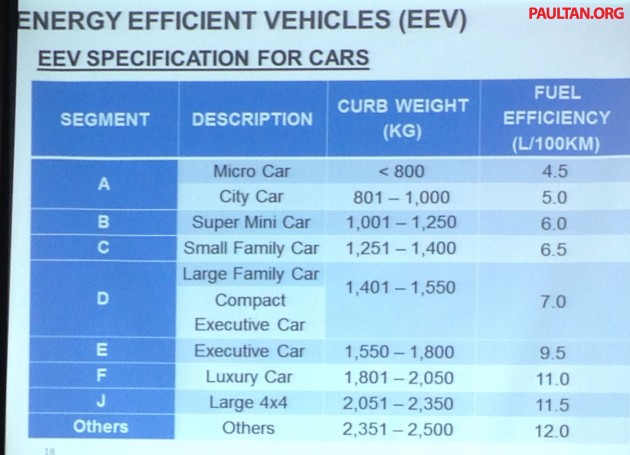

Classification of EEV

– includes cars and motorcycles

– currently taking only fuel consumption into consideration, CO2 have to wait till Euro 4 fuel, which the government is currently studying – results of this study to be announced two months from now.

Customised incentives for both FDI and DDI

– Pioneer Status, Investment Tax Allowance, grants (R&D and training), infrastructure facilitation, better tax rates, expats and others.

– No conditions.

– More than RM2 billion worth of grants and soft loans will be allocated for the EEV segment until 2020. Funds allocated will be RM1.89 billion in soft loans and RM175 mil in grants.

Targets towards 2020

– additional 70,000 jobs in manufacturing and 80,000 in aftermarket, making for a total of 150,000 new jobs.

– Export this year is RM5 billion, target to double to RM10 billion by 2020

– TIV will be one million units by 2020, while total production volume is expected to be 1.25 million units, of which 250k will be export.

Exemption until Dec 31, 2015 for CKD hybrids, Dec 31, 2017 for CKD EV

Impact on car prices

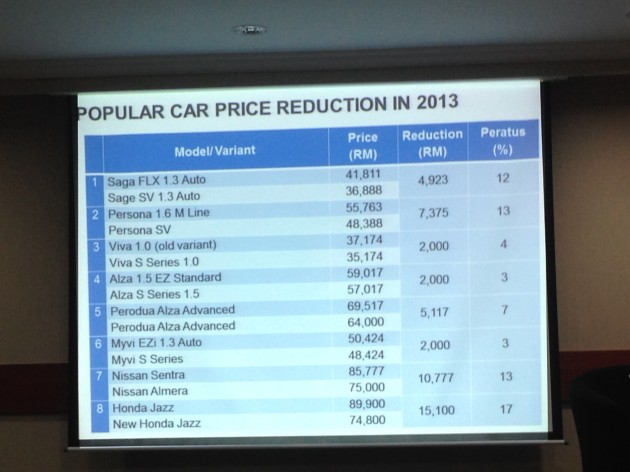

– In 2013, popular cars as per table above, with lower price tags accounting for about 30% of market share.

– In 2014, more new models and variants will be introduced, prices of these are expected to be more competitive.

– Example, price of new Alza in January 2014 was lower by 2-7%.

– These new models/variants are forecasted to capture 55% of market share.

Car prices

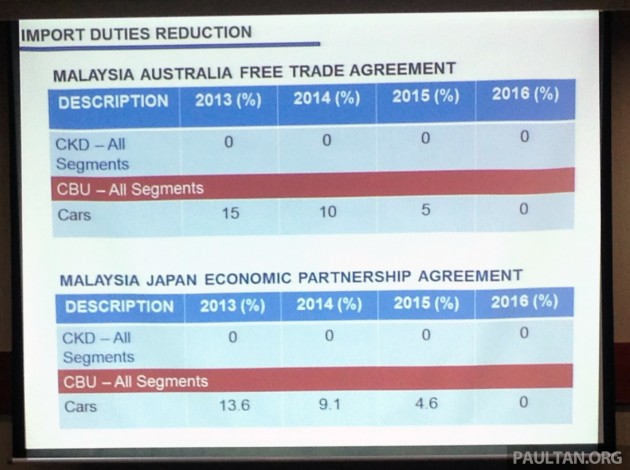

– Car Price Reduction framework, gradual car price reduction of 20-30% by 2017

– done through liberalisation of auto industry.

– Excise now 65-105%, average paid by most companies is 50%.

Approved Permits

– At the moment, AP policy remains.

– NAP 2009 had earlier specified for termination of open AP by Dec 31, 2015 and franchise AP by Dec 31, 2020.

– The government has decided that an in-depth study will be undertaken to assess impact of this termination on Bumiputera participation in the auto industry.

CBU Hybrid and Electric Vehicles

– Stocks carried over from last year continue with import/excise exemption until stocks are sold. But full import/excise exemption for CBU hybrids and EVs has been discontinued.

Looking to sell your car? Sell it with Carro.

AI-generated Summary ✨

Comments express skepticism and disappointment about the effectiveness of the NAP 2014 announcements, questioning whether car prices will truly drop or if the policies are just political promises. Many criticize the ongoing AP system, alleging it still benefits crony manufacturers and inflates prices, with some calling for its abolition. There are concerns over the lack of clear details on tax reductions, import duties, and whether hybrid and EEV incentives will benefit consumers. Several feel the measures are insufficient and suspect they are mere "sandiwara" to deceive the public, with some urging a boycott of new cars or switching to second-hand vehicles. Overall, sentiments lean toward distrust and dissatisfaction, believing that real car price reductions and industry reforms are still far from achieved.