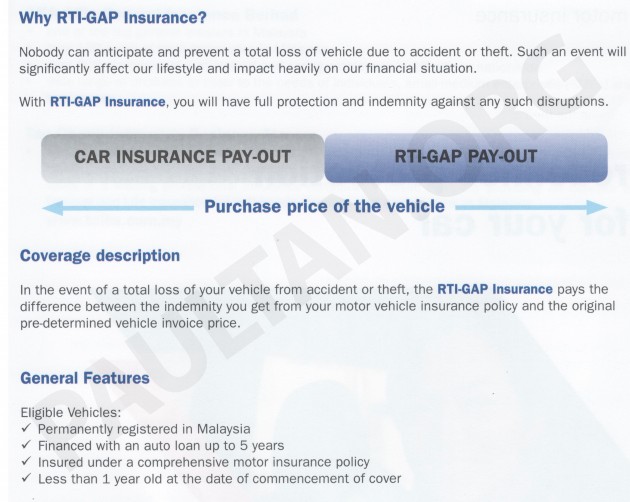

Tan Chong Insurance Business Stream (TCIBS) and AXA Affin General Insurance today launched the availability of RTI-GAP Insurance for Nissan cars in Malaysia.

RTI-GAP basically means Return to Invoice-Guaranteed Asset Protection. This type of insurance is actually pretty common and sometimes even mandatory to be purchased in first world countries, but we’re only just seeing it introduced in Malaysia this year.

This type of insurance basically ensures that you won’t have any problems covering your outstanding hire purchase loan if your Nissan is stolen or is declared a total loss because of damage. It also helps you easily replace your car with another Nissan of similiar value.

Let’s say you bought your Nissan at RM80,000 and after three years the value drops to RM50,000. If something happens to the car at that point of time, you will only be reimbursed the market value of RM50,000 by your motor insurance. And if you still owe the bank RM60,000 at that point of time, you will have to fork out RM10,000 extra to pay off your hire purchase loan.

This is where RTI-GAP insurance comes in. It will pay the difference between the market value and the original purchase price. This means you will get a payout of RM30,000 which is the difference between the RM50,000 market value and the RM80,000 original purchase price. You can then use RM10,000 for the difference in hire purchase outstanding and RM20,000 to pay for the downpayment of a new Nissan to replace the one that was declared a loss.

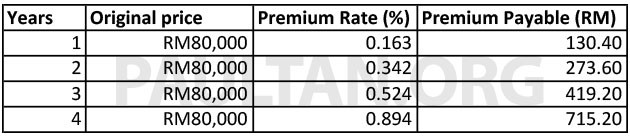

You are allowed to buy RTI-GAP insurance for up to 5 years but in Nissan’s case, you are already protected for your first year under the “Nissan for Nissan” scheme if you buy your motor insurance through TCIBS. This means you have the option of buying coverage for the 2nd year up to the 5th year.

Here are some sample premium rates for an RM80,000 car, excluding 6% GST.

This premium is only payable one time upon purchasing the car so think of it like an “MRTA”. Tan Chong says they are also working to see if they can bundle the premium under the hire purchase loan. If you buy coverage for three years and sell the car before the three years are up, you can get a refund on the balance coverage period.

The maximum applicable purchase price that can be insured under RTI-GAP is RM385,000 and the maximum benefits payable is RM115,000. RTI-GAP insurance is only applicable for private registration cars.

There is a similar program of this type offered by Nasim Sdn Bhd called Peugeot Protect.

Looking to sell your car? Sell it with Carro.

Nissan Serena e-Power

from RM154,800

Nissan Serena e-Power

from RM154,800  Nissan Kicks e-Power

from RM113,800

Nissan Kicks e-Power

from RM113,800  Nissan Navara

from RM98,600

Nissan Navara

from RM98,600  Nissan Almera

from RM83,888

Nissan Almera

from RM83,888  Nissan Leaf

from RM168,888

Nissan Leaf

from RM168,888  Nissan NV200

from RM79,800

Nissan NV200

from RM79,800

can a secondhand car take RTI Gap insurance?

consider to get a secondhand Nissan soon, might take 60K loan.

max is 5 years. and the car must be bought new; coverage starts at the end of 1st years.

and i think this only works if you plan to buy another nissan to replace the current nissan.

the catch is actually simple.

nowadays ppl always complaining that car depreciate a lot compare to the days of the 80s and 90s.

when actually it is unlikely not the case.

you see back in the 90s max loan is 20% and tenure is 5 years. only in 95 it went up to 6 yrs. and then later 7 yrs and by year 2000 – 9 years.

because of this, loan balance is always lesser than market value (even trade in value) so car owners did not feel they were losing when it comes to sell the car or written off.

a simple calculation is like this

take a toyota corolla altis 1.6 selling at 100k (the previous series, now no more 1.6)

2 buyers.

1st customer pays 10% deposit = 10k.

loan only 5 years.

2nd buyers instead of paying 10%, opted to go full loan using marked up figures. in this case, he will go altis 1.8 at 110k. (take note banks wont approve for toyota cars since every models is marked in registration card. example vios E instead of general statement like Proton persona without mentioning it is B line or H line. this is just a case study)

the second buyer also will go out to 9 yrs loan.

some 10 yrs ago, banks and insurance were using simple calculations to know a car’s market value. now, they look at actual market trend – including mudah.my.

A.

car value new – 100k

1st year – 90k (minus 10%)

2nd year – 81k (minus 10%)

3rd year – 73k (minus 8k)

4th year – 65k (minus 7k)

5th year – 58k (minus 7k, rounding)

1st buyer

car price – 100k

loan – 90k

max 5 yrs – total amount 103k.

mthly 1725.

at 4th year (48th mth) car total loss. he already paid 83k.

balance to pay 20k

car value 65k

amount he got – 45k.

(that was how our grandfathers manage to change cars in style some 20-30 yrs back)

B. 2nd buyer

car price – 100k

loan – 100k (marked up price)

max 9 yrs – total amount 127k.

mthly 1175.

at 4th year (48th mth) car total loss. he only paid 56k.

balance to pay 71k

car value 65k

amount he got – 0k. instead he is owing the bank 6k (need top up)

this is the difference of then and now.

why it happened, one may ask? car price too high.

why too high? government asking excise duty 75% + GST 6%

typo error.

in 4th paragraph i should be 90% max loan, not 20%.

apologies

But why GT86 not same amount of yen as AE86 when both first launch? Mesti tongkat salah kan.

Thanks for the calculations. WHy price too high? Plotong. That’s why I said before, Proton supporters are national threats.

In regards to gap insurance.. most US car sites discourage it as a way to minimise insurance spend. But I don’t know..for the premium seems a good deal. But like you say, only those with long repayment and low downpayment are hit when insurance claim. Or go my route, save on the depreciation with a 2nd hand car all the way until (maybe) I got a million bucks.