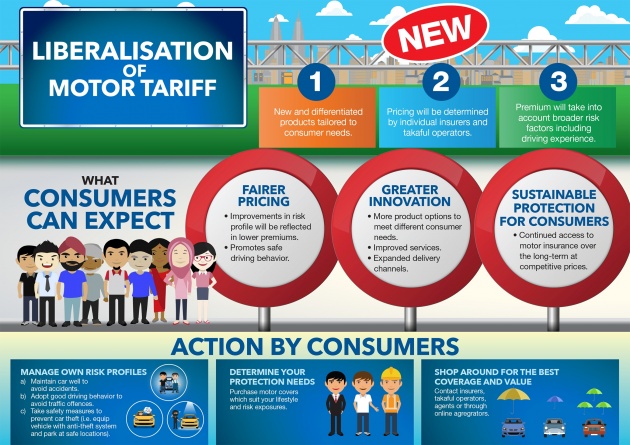

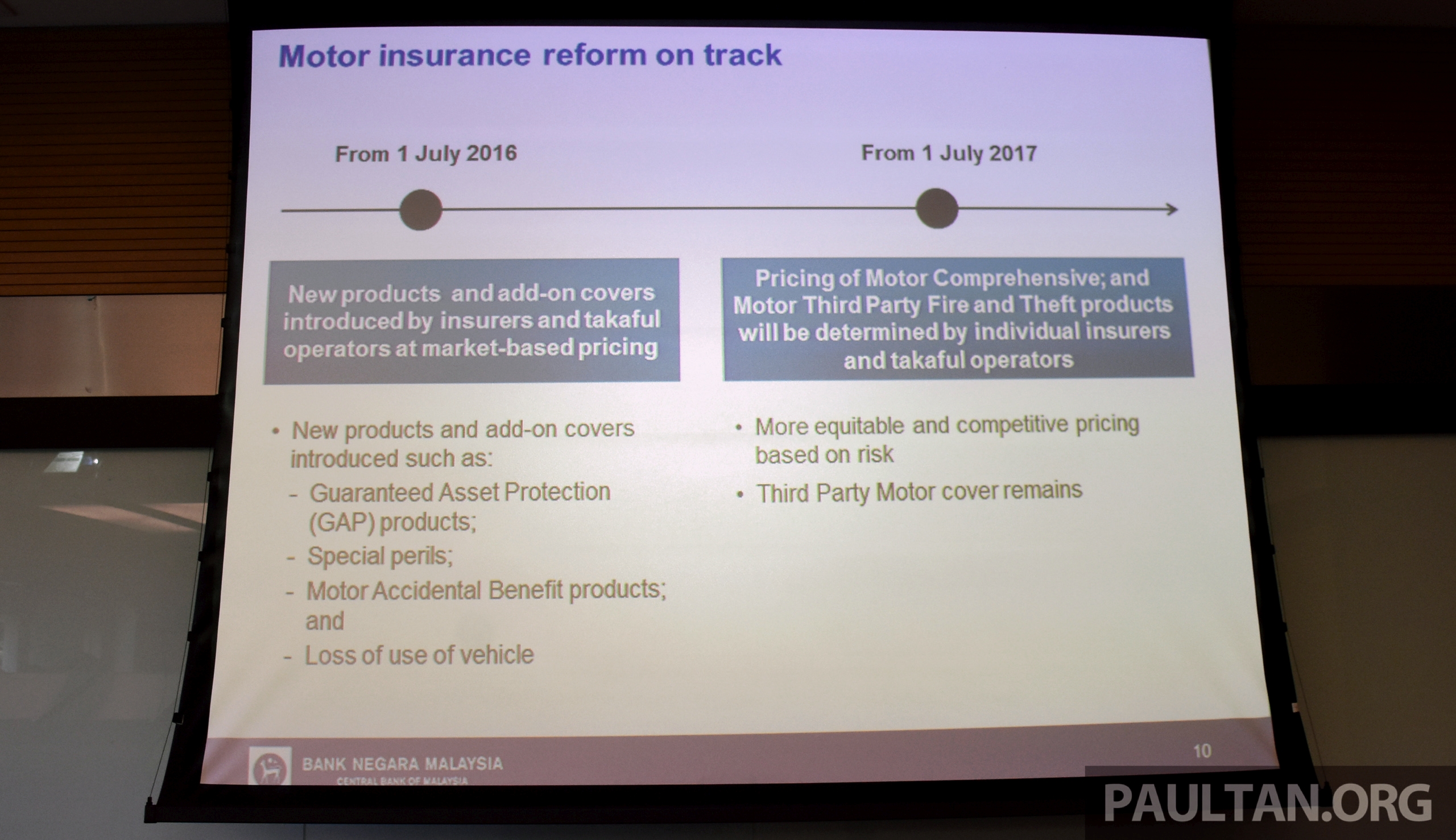

The phased liberalisation of motor and fire tariffs announced by Bank Negara Malaysia (BNM) last year, which kicked off with the first phase on July 1, 2016, is set to move to the next phase on July 1 this year.

Phase two of the programme, which is working towards the eventual removal of motor and fire tariffs by 2019, will see premium rates for motor comprehensive being liberalised, with pricing being determined by individual insurers and Takaful operators based on a risk-based assessment system.

From July 1, 2017, how much one pays for insurance will no longer be determined by fixed price lists, but by his or her risk profile. This means that theoretically, no two insurers will have identical pricing for a motor comprehensive policy.

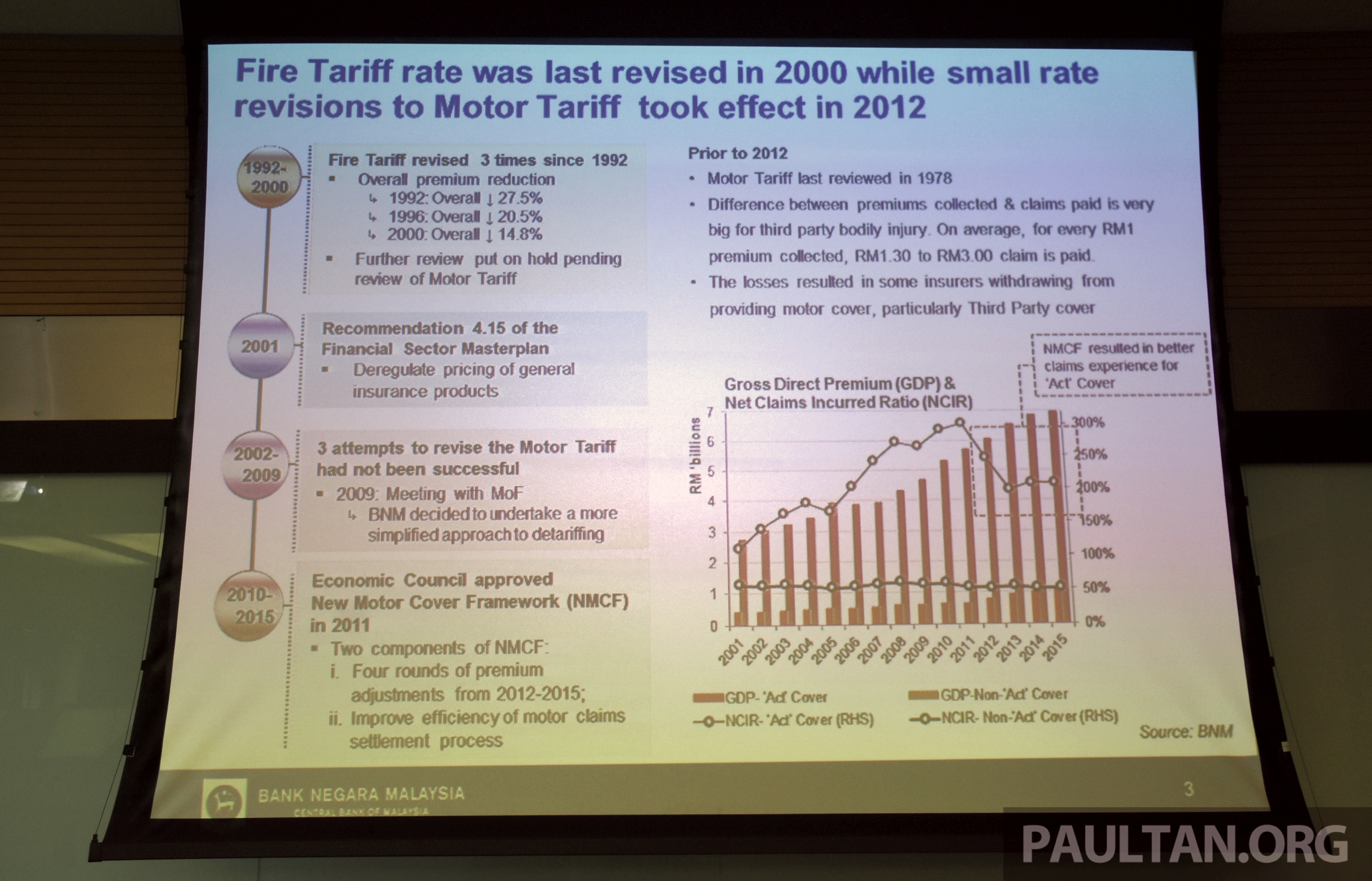

Premium rates for motor third-party policies will however continue to be regulated and subject to tariff rates, with a gradual increase in pricing over time – the insurance industry has stated that the segment is “substantially underpriced” at present and immediate detariffication will result in a sharp price hike.

While insurance companies haven’t yet revealed specifics of how their motor comprehensive premiums will be tailored and more importantly, how this will translate into pricing for the consumer, BNM has suggested some initial details on how the liberalised landscape will shape up.

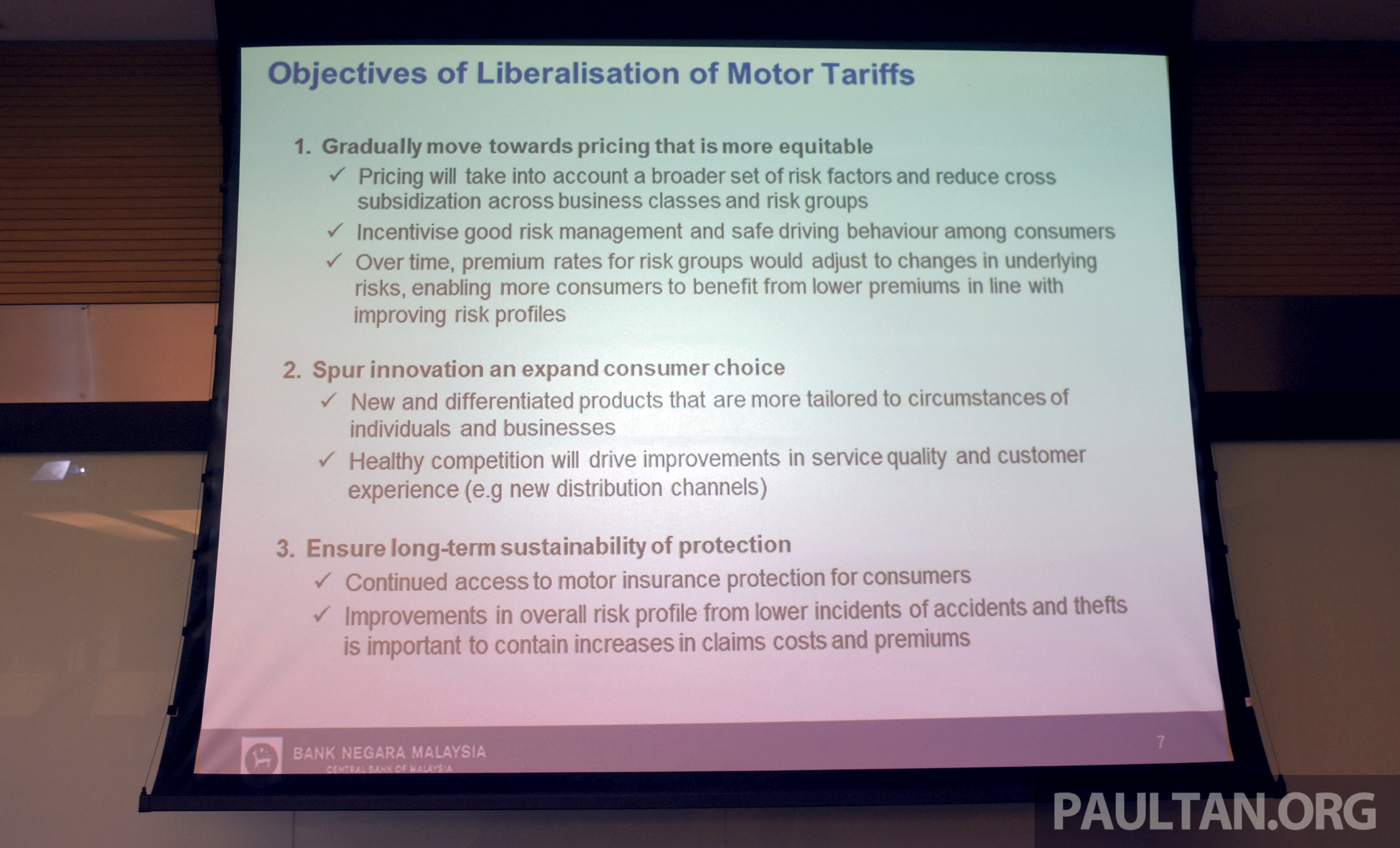

At a press briefing on the subject last Friday, the central bank said that the move towards liberalisation has long been overdue, and the switch to a risk-based assessment system will bring about innovation and be much more beneficial to consumers.

“The reality is that the premiums that are collected today and the claims that are paid, particularly for bodily injury claims, have a great disparity. It has been there for a long time, when you consider that we have not touched pricing since 1978. Over the long term, this is not going to be sustainable,” BNM assistant governor Jessica Chew said.

She explained that the opening of the market “will allow insurers to take into account a broader set of risk factors, and what it will do is to reduce the cross subsidisation between business classes as well as risk groups.”

It is also targeting at improving safety on the road, incentivising good risk management and inculcate safer driving habits. What this will do is reward good drivers with no history of claims or reckless driving and bring about higher premiums to those with the opposite, ensuring that things – and pricing – are more equitable and fairer than that in place now. “This will allow consumers from the low-risk groups to enjoy lower premiums,” she said.

Under the new environment, more risk factors are set to be taken into account in determining premiums. Other than the sum insured, cubic capacity of the engine as well as the age of vehicle and the driver, premiums may be driven by other factors. These could be safety and security features in the vehicle, duration that the vehicle is on the road geographical location (areas with higher incidents of theft) and traffic offences on record.

Similar to the system employed in countries like the UK, factors such as these will define the risk profile group of the policy holder, which will then help determine the premium. Since insurers and takaful operators will have different ways of defining the risk profile group, the price of a motor policy will differ from one insurer to another.

Enhancements to consumer protection will also be introduced, to ensure proper governance over product design and pricing. Insurers are expected to assess the risks appropriately and consistently for fair treatment of consumers. The standard scope of coverage disclosure will be increased, so consumers can easily compare between insurers to make informed purchasing decisions.

While insurers will be able to determine how their products are fleshed out as well as the rates of the premiums, consumers don’t have to fear a sharp spike in pricing with the removal of tariffs. The central bank will provide the necessary input to ensure that pricing in the new market doesn’t become a free-for-all.

“All insurance companies will have to file their products and their rates with BNM, which we will then look at. This will give us the opportunity to review the risk factors that they take into account and how they are actually being translated into the pricing. We will ensure that the adjustments are both reasonable and gradual. Excessive adjustments are something that we will be seeking to tamper,” Chew explained.

The central bank expects that there will be no massive shift in pricing, and if anything believes that prices may go down in the short term as a result of competition between insurers.

For consumers, this will mean more choices to pick from at competitive prices, with the ability to shop around for coverage that best meets their insurance needs. “Consumers should benefit from the more liberalised market where you have more control over what you pay for,” Chew said.

Modernisation will bring about a more varied and improved landscape, bringing about better service quality and customer experience. “We need this environment because only then can we see more innovation in our market and this will allow consumers to have more choices in terms of the types of cover they want to buy instead of a standardised product,” she added.

Still, mirroring the earlier call made by the General Insurance Association of Malaysia (PIAM), the central bank advises consumers shouldn’t just be looking at pricing as the only factor when purchasing a motor insurance plan, and that they should pay attention to all aspects of coverage, including exclusions.

Looking to sell your car? Sell it with Carro.

this is coming from the same people who said that prices won’t go up, instead will drop once GST is implemented!

The people are suffering from all sorts of price increases and now going to be hit by the biggest conman of all…insurance companies.

Buy P1 get low insurance

Thats quite true cuz P1 has more cars with higher NCAP stars than other makes bar Honda.

According to your logic, Volvo would have lower insurance but why not?

“Moving toward a higher revenue for all the insurance company!”

Thanks to all these new policies, patrol weekly pricing, liberalization of motor insurance. Malaysian’s living cost is keep on rising.

All this liberalisation have no meaning when BNM themselves cannot sort out the insurance fraud in the industry which is so rampant. Basic also BNM cannot do but want to do all this liberalisation.

This new system will eventually raise tariffs and premiums and this is because Insurance companies cannot sort out their own fraud which they know exist.

To all the insurance companies including BNM, pls don’t pretend to be innocent. You all know damn well that every adjuster of yours is working hand in hand with the police, investigation officer and the car workshop to get kickbacks. I myself had many accidents.

Infact the last accident I had, I sent my car to my own friend workshop, he said he will repair everything for RM1000. I tried another workshop, he assessed the repair to about RM1200. I thought, nevermind, I will send for insurance claim and I can save the RM1000.

So, I sent the car to the panel workshop. After repairs and all that, out of curiosity, I simply called the insurance company up to find out how much was the bill, it was shockingly RM8000. Yes, 8x the actual amount if I had the car repaired by myself.

We all know what happens. The IO (Investigating Officer), the Adjuster, as well as the bengkel and the ulat ulat runner boys will get their kickback. Biggest kickback would be the adjuster. At least he makan few thousand for his personal pocket.

The Insurance companies know about all this. Hundreds of cases happen everday. But they close an eye. They pass the problem and burden to the consumer with higher premiums. This BNM cannot sort, they want to do liberalisation?

BNM, you know this happens but you too close an eye. This results in higher burden and premiums for the public and now, this new liberalisation, which is utter bogus.

Bank Negara, please read the above. I repeat, you also know about all this. But BNM just keep quiet. You all just close an eye because the problem now goes back to the consumer with higher premiums.

With all this shit going on the Insurance industry dare to increase the car premiums for the motor industry every year and now, do this system which will make them more money.

That is Malaysia for you. The rakyat suffer the most because there is no proper enforcement and the insurance industry is full of cheats.

Everybody suffers when everybody along the line gets kickbacks from the police office, the police cameraman, the adjuster, the bengkel and the runner boys (ulat ulat).

The Motor Insurance Industry collected no less than RM100 billion in premiums last year. It is not fair that we public have to pay higher premiums because they cannot sort out the fraud in their own backyard. Trust me, premiums will go up no matter what BNM says.

Bingo.

I’ve personally seen Perodua’s own body and paint branch charge to insurance RM 8,000+ for Myvi’s front bumper, a (1) headlamp, the rest reuse back, knock and respray fender and bonnet.

Never knew Myvi has become luxurious car. No wonder perodua after sales’ revenue having a good year, just slaughter insurance company, and the repercussion is now we have to bear higher interest.

Only ulu people would believe premium will not increase or can even reduce after this.

Based on this logic, we must be better off with closed off system, with no freedom or innovation like North (Bestest) Kimchi. And here we have pipu who clamour for more liberalisation and freedom….

Bank Negara(BNM) can makes nice slides and vids to promotes this liberalisation moves but what consumer really wants is lower insurance premium!!! f those bloody panel workshop and adjuster!(they are leeching insurance industry until it dries) BNM must improve consumer banking too!!! (not just 2 counter for consumer banking while the rest 8 counter are for investment/insurance/corporate banking!!! without consumer theres no bank at all!!! but now, after banks grown larger they seem forgotten its base customer which is consumer, plain rakyat! BNM should open up new license for new players that really cares about consumer banking! wake up BNM else remove that M! just call Bank Negara(BN) instead!

more regulations should be enforced on this scam industry….too many con cases where people are duped into buying useless policies

Let’s hope for some good news.

Smart move indeed.

Syndicates cheat insurance companies through bogus motor accidents, fraudulent and inflated repair claims.

Ya la….syndicate cheat insurance companies but in the end the customer will still have to pay for the cheating.

Kolos all cheating workshops!!

Uh oh… no more NCD

We’ll see how the rates going to be after July, but knowing the gov, I am guessing the premium going to increase. But who knows…

Yup, base premium was increased when I renewed my insurance yesterday.

If you want to pay less for annual car insurance renewal in the near future, make sure that your next new car has electronic stability control (ESC) and as many airbags as possible. Only buy 5-star ASEAN NCAP rated cars, don’t settle for less.

Yes, it might be true that safer cars tend to be more expensive, but it’s a one-time investment and over many years, you will save more money under this new insurance policy. Plus, nowadays, there are many affordable cars under RM100k with ESC and 6 airbags.

Also, buying a safer car can only be a good thing. If you value your life, you wouldn’t put a price tag on it.

Actually, its no longer expensive for safer cars now with P1 newer models.

From what i read theres personal risk assessment system. While theres no clear description on this, i believe this similar to our health insurance thing. The more riskier you are the more you pay. Well thats allright when u are 19 or 25 or 35. However aged people will pay more than say a 28 years old. Well this is my opinion and lets hope i am wrong.

you are right that eventually there will be a personal risk assessment. however unlike health insurance, in motor insurance it is more likely that the older drivers will pay less. this is because younger drivers at about 18 – 25 years old are deemed to be higher risk compared to older drivers at 40 years old.

If follow western overlords, there shud be a bell curve where the riskiest r from the young drivers and the older/senior aged drivers. At there, the insurans premium for beginner drivers is more than the car price!

And it deincentivise old pipu to continue driving.

Temper, not tamper

Tamper, not temper

The word should be temper, not tamper

This is a good move to “penalize” risky group and to offer carrot to decent motorists. It could be better if the fundamental element of the pricing mechanism (car price) to set lower like other developed economies instead of maintaining the status quo of one of the world highest price cars nation.

Don’t milk money from us sudah lah

Sapot P1 sudah boleh lah

Wow..now everything also let to rakyat to manage themselve. Gov institution just plainly watch from aside. This proposal somehow have cons to customers which may cause higher premiums. E.g. u bought favorite car in theft list, your car lack of safety feature, ur motor vehicle age..all this which is out of customer control sooner or later..

there could be beneficial outcomes for consumers with this method. if a vehicle is in the theft list, lacks safety features, and has other bad characteristics, insurance premiums will be higher for the said vehicle. and when premiums are higher, sales of the vehicle will reduce as customers would not want to purchase a vehicle with higher premiums. this will pressure vehicle manufactures to ensure their vehicles are safe and secure while being affordable.

Everyday, Malaysians are being played for fools where the system allows the rich to become richer, middle class struggle to hang on, those living in poverty would never seem to have any chance at all. Fed by the very propaganda that almost all sneered but to no avail.

I agree with you. Slowly but surely some power top of the pyramid will make sure the 99% pays for all, takes all the burden and the 1% enjoys their life like heaven on earth.

99% can vote though

Haha..do you think you have any choice.the candidate is selected by the ‘party’…they serve the party not you..even worse the party serve their lobby master..same master for all the party..sorry to disappoint you..you actually have no voice..

Whats going to happen are those who frequently caused accidents will not be able to afford insurance & will thus continue to drive without one. Not having license & roadtax doesn’t stop people from driving nor are they affraid of the law. So what is the government going to do about that?

One hand say , current premium grossly undervalued , other side say expect no big increase , I think we know what it means

This is inevitable. Insurance cannot sustain the high claims ratio anymore especially THIRD PARTY CLAIM.

Here is my hypothesis. It is based on my own assumption ya.

The biggest problem is third party claim where we have ulat, corrupt IO, corrupt lawyer, corrupt adjuster and corrupt repairer working in league to scam the Insurance.

In an accident, the Ulat (works with corrupt Lawyer) will identify the innocent driver and persuade them to file a THIRD PARTY CLAIM instead of OwnDamage-KnockForKnock.

Ulat then get the corrupt adjuster to come over the get an estimate of the damaged car. Ulat then send car to a corrupt repairer (normally non panel and small repairer). Lawyer then gives money to Repairer to repair first. Receipt is then given to lawyer. Once car is done, innocent driver happily sign all necessary documents and take his away. Then all docs is passed back to lawyer. Lawyer then compiled all docs, receipt, adjuster report and with the “Keputusan Kes” file a LIABILITY CLAIM against the insurance company. When the insurance got the claim, it is too late. Car is repaired and collected. THey have no say as to the cost of repair. Common sense will tell you that the cost of repair will be many times higher. Btw, BNM has no say in this because the lawyer file a LIABILITIY CLAIMS which is outside the scope of insurance claim.

Again, the above is just my assumption. If I have erred forgive me. Do add if you have any feed back.

That’s our insurance company, giving rubbish claims on car accident and keep taichi pressure and explaination to adjuster and repairer. Understand repairer nowadays not like last time since it’s panel repairer by insurance but insurance still refused to pay or cut money till repairer change a cheaper quality. Then keep said is adjuster recommendation but common sense, would adjuster want so much trouble try save money for insurance in the expense of getting complains from customer?