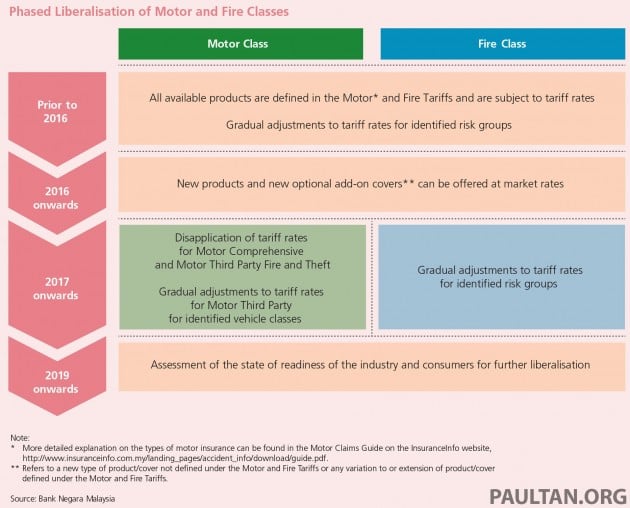

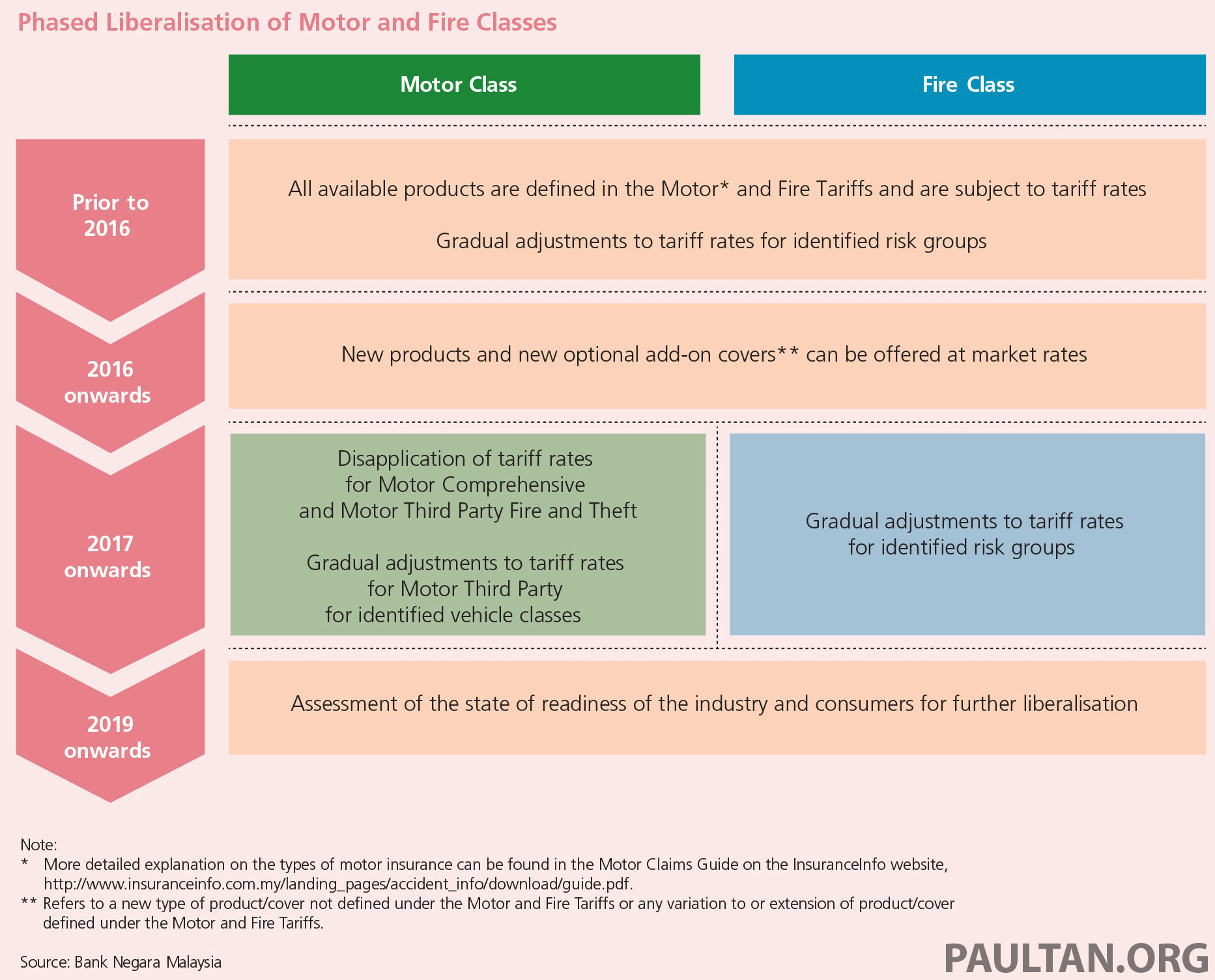

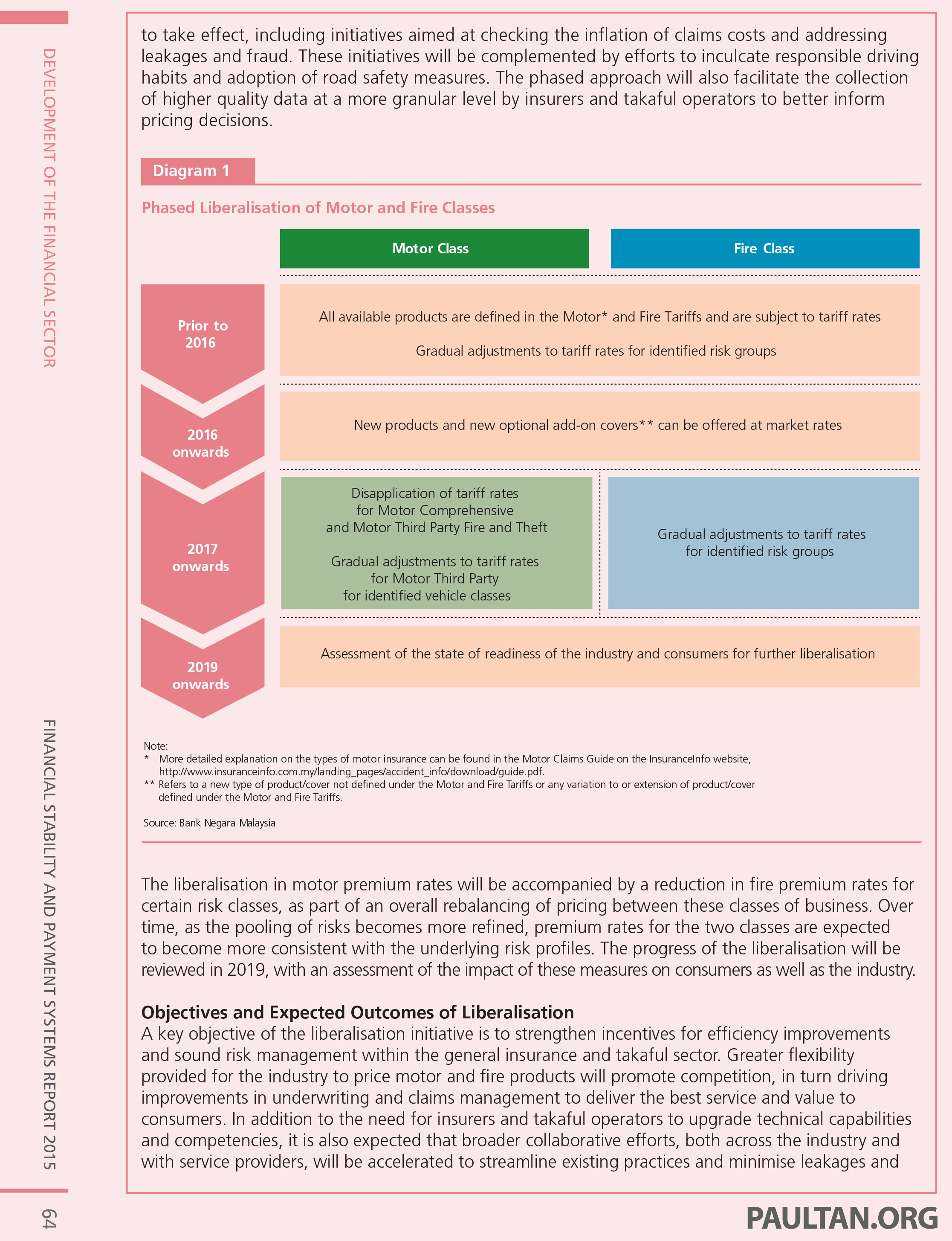

As announced in 2012, and reaffirmed in 2014, the liberalisation of motor insurance tariffs in Malaysia will commence from July 1, 2016. In short, motor insurance premiums will soon be based on a list of risk factors, instead of the current overly simplified and regulated pricing policy.

Bank Negara Malaysia (BNM) confirmed the move in its Financial Stability and Payment Systems Report 2015, released today. The report includes the roadmap towards the full liberalisation of motor insurance tariffs – a gradual move towards pricing of motor policies that is more reflective of risks.

To minimise the impact of the move (to both consumers and insurers), an orderly transition plan has been laid out. The existing insurance tariff requirements – relating to pricing and coverage limits – will be phased out, but not immediately. Refer to the diagrams below for the full roadmap.

In the first phase (the first year of implementation, starting July 1), the industry will be allowed to offer “new products” and optional add-on covers at market rates. This can include, for example, additional policies to cover engine hydro-lock (water entering the engine in lightly flooded areas, separated out from the currently costly flood damage insurance), lost car key replacement, and perhaps even the availability of courtesy cars.

Prices of these new products will not be regulated, and as such will be determined by the market. Insurance providers will be open to price them as they see fit, to attract consumers. This will provide an early platform for insurers to refine their offerings and pricing policy, while consumers get additional choices to fit their individual needs.

The second phase (2017 onwards) will see the disapplication of tariff rates for comprehensive and third party motor insurance. Here, premium rates will no longer be regulated, and will be determined by the market. Risk-based assessments will also be introduced in Malaysia.

As such, various risk factors not included in the current motor tariff, such as residence location, vehicle make and model, use of vehicle, occupation of owner, claims history, gender and age will be taken into consideration, similar to the system employed in countries like the UK.

In other words, the insurance premium rates you pay will depend on how much risk you are perceived to carry – for instance, owners of makes and models with high repair costs, owners of high-performance vehicles, owners with fewer years of driving experience or those who live in crime-prone areas may have to pay higher premiums. And the rates offered to you will not be regulated, so prices may vary across different insurance providers.

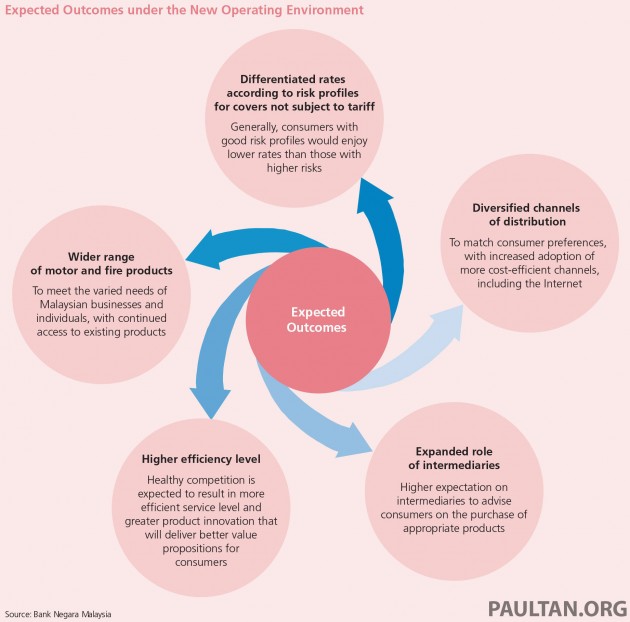

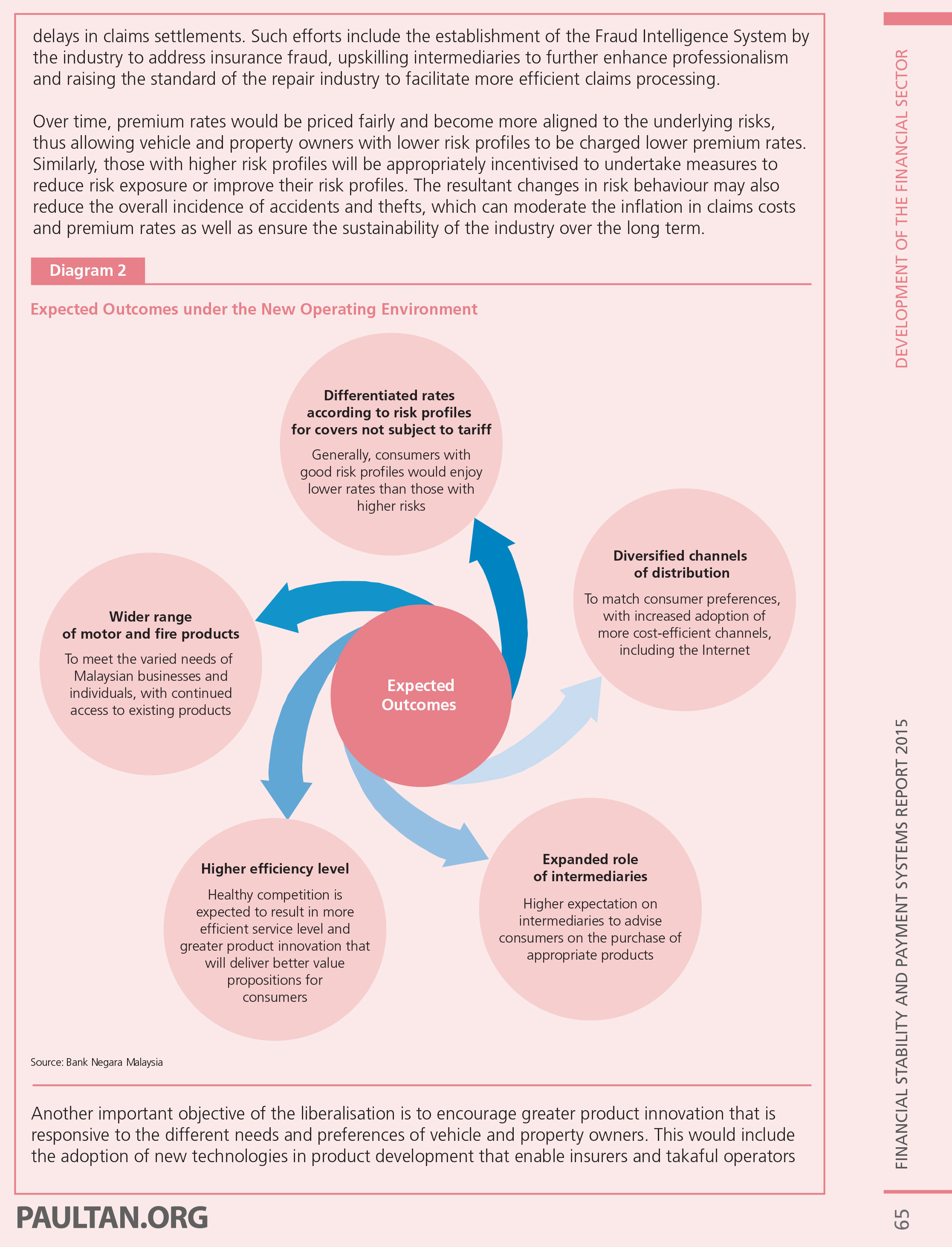

Enhancements to consumer protection will also be introduced, to ensure proper governance over product design and pricing. Insurers are expected to assess the risks appropriately and consistently for fair treatment of consumers. The standard scope of coverage disclosure will be increased, so consumers can easily compare between insurers to make informed purchasing decisions.

However, this will not apply to third-party insurance of certain identified vehicle classes. Premium rates for these classes (unspecified as of yet) will continue to be regulated, with gradual adjustments to be made.

It’s said that currently, there’s a large discrepancy between third-party insurance premium collection (RM520 million) and the incurred claims and expenses of these classes (RM680 million). Given the sizable pricing gap relative to risk, a full deregulation of rates will inevitably result in steep premium increases. Thus, a more measured approach is being taken for these vehicles classes (third-party insurance).

The move to liberalise the motor insurance market is expected to provide greater pricing flexibility between insurance providers, which will promote competition between them. Consumers will largely benefit from this open market, with insurers competing to offer better coverage, services and of course, pricing. More streamlined practices will also minimise delays in claims settlements.

In the long run, vehicle owners with lower risk profiles will be charged lower premium rates, while those with higher risk profiles will be properly incentivised to undertake measures to reduce their risk exposures. Consumers will also be open to customise the coverage limits or purchase optional extensions as they please – pay less for lower coverage, or pay more for a more comprehensive policy.

Looking to sell your car? Sell it with Carro.

AI-generated Summary ✨

Comments express concern that the liberalization and risk-based pricing will lead to higher premiums, especially for older, less safe, or high-risk vehicles, and certain demographics like young or male drivers. Many believe the system favors insurance companies, increases income inequality, and may promote fraud or collusion. There's skepticism about Malaysia's readiness for such a system, expecting significant price hikes and unfair premium disparities, with some viewing it as a means for insurers to maximize profits at consumers' expense.