Remember when the six-month moratorium for loans ended September last year? There were some groans from the rakyat, some of whom had either put the “saved” monthly sum to essential use, or merely enjoyed the extra spending power on treats.

Even until today, there are politicians and sections of the public wanting a blanket moratorium just like the one we had during MCO 1.0, where many businesses were forced to shut. Besides helping those in need, more spending by the rakyat would mean more money going around, which will help businesses too – so the theory goes.

There might be some merit in that argument, but Bank Negara Malaysia (BNM), looking at the larger picture, is in favour of a more targeted approach when it comes to assisting those in need. According to BNM Governor Datuk Nor Shamsiah Yunos, a blanket loan moratorium is not in the best interests of the country’s economy and the rakyat. Instead, a targeted approach puts the choice in the hands of the borrower.

She said last month that so far, 1.4 million Malaysians have applied for repayment assistance, and the approval rate is 95%. Significantly, 45% of these borrowers chose the option of a reduced monthly payment instead of a full loan moratorium.

“They are not asking for moratorium and they do not want a one size fits all solution. What they want are tailored assistance that meet their financial circumstances,” Nor Shamsiah said at BNM’s 2020 GDP data announcement event. The central bank governor also pointed out that a majority of borrowers across different segments have already resumed loan payments, some even before last year’s automatic moratorium ended.

If you need it, help is there

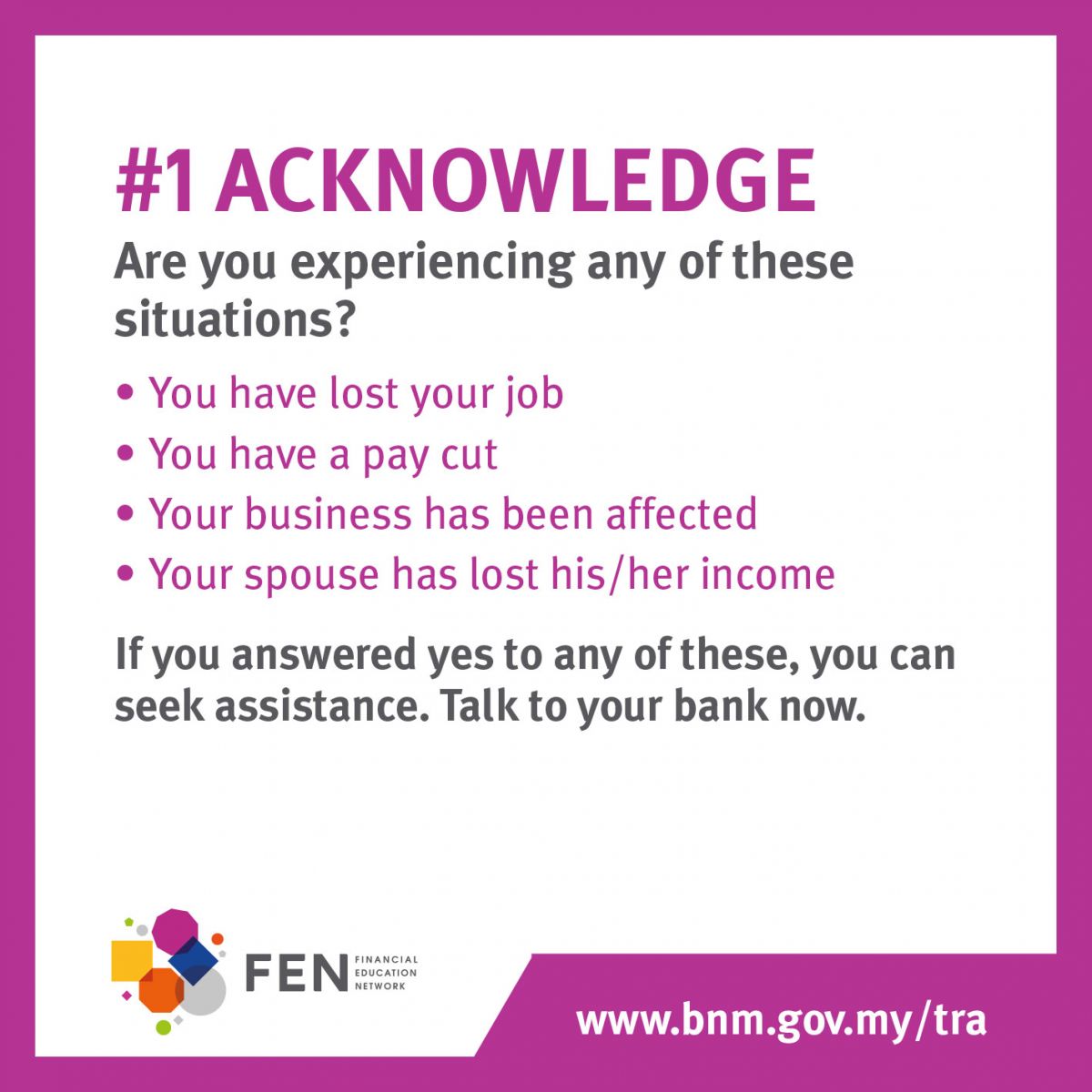

But if you need it, help is there. For borrowers whose income has been affected by Covid-19 and the resulting movement control orders, Targeted Repayment Assistance (TRA) is provided by the banks to ease the burden. Here, we take a closer look at TRA, who is it for, what it does, as well as the pros and cons.

The blanket moratorium-replacing TRA is aimed those whose financial situation has been adversely affected by Covid-19 and the various MCOs. If you have lost your job, received a pay cut, or if you are self-employed and your takings have been affected – TRA could help tide you over this difficult period. If the loan is under your name but your spouse, which normally contributes, has lost his or her income, you can also consider TRA.

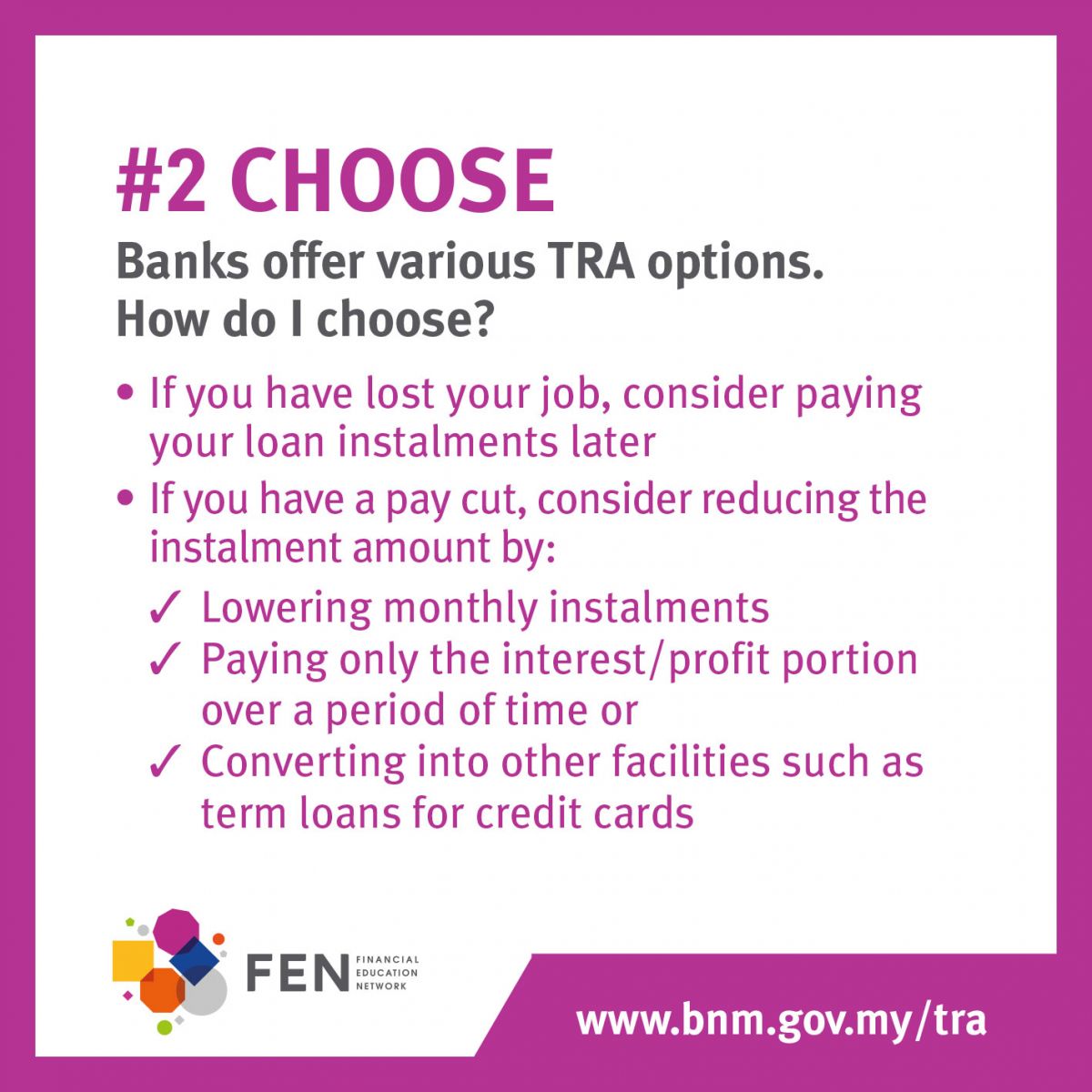

There’s no one size fits all solution here. The borrower will need to approach his/her bank, who will then offer a couple of TRA options.

For instance, if you have lost your job, a deferment of loan payment would be ideal, as there’s no income. Those who have had pay cuts might be better served by a lowered monthly instalment in proportion to their salary reduction, or even paying only the interest (or profit in Islamic banking) portion over a period of time. If you have outstanding credit card debts (which attract very high interest by the way), they can be converted into term loans, for example.

If you’re worried about TRA affecting your CCRIS (Central Credit Reference Information System) record, don’t, because applications for repayment assistance at any time before June 30 this year will not be reflected in the system – these are after all extraordinary times.

It’s not debt forgiveness

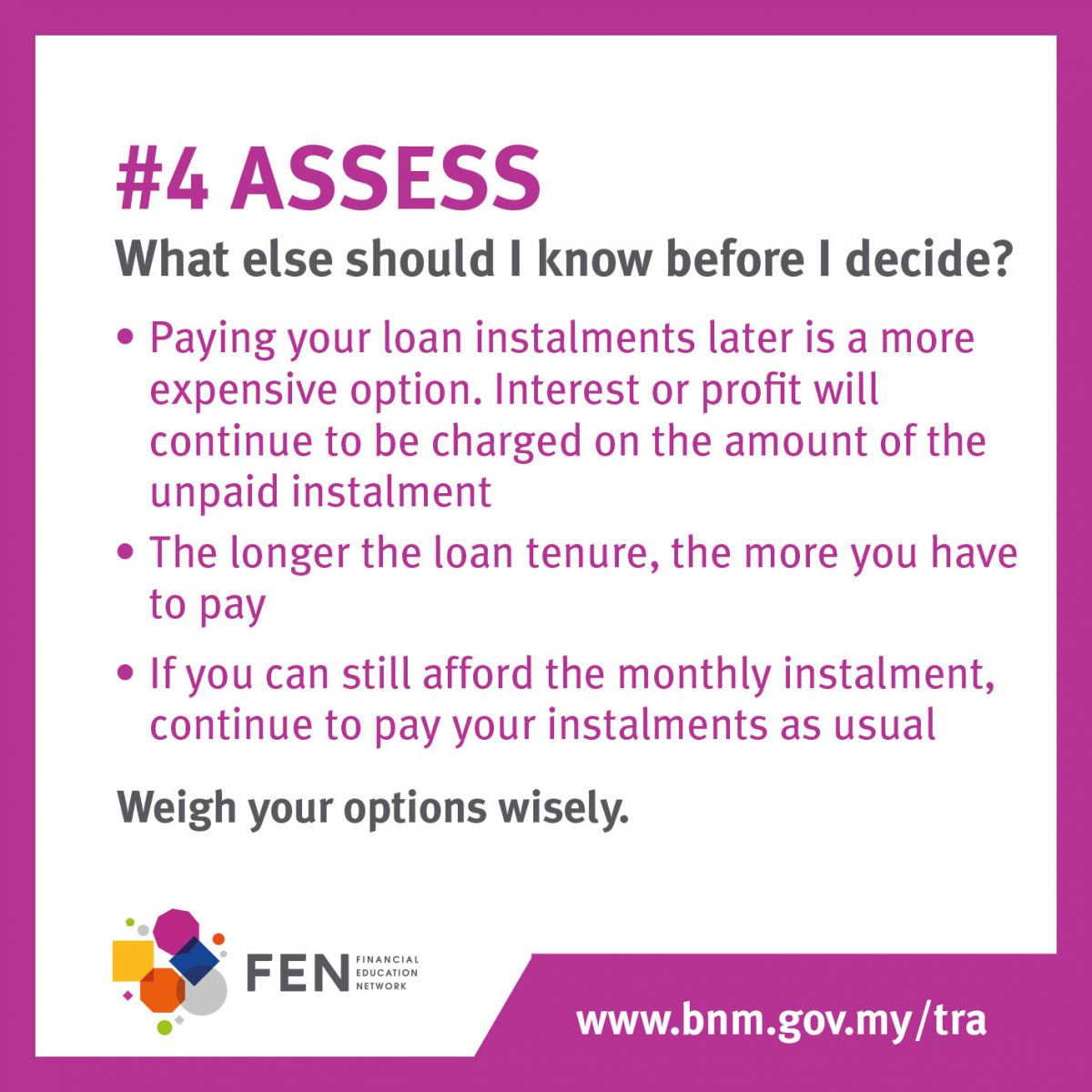

That’s it? Unfortunately, no. As with everything else in life, there are terms and conditions, plus consequences. By allowing you to temporarily pause payments and/or reduce the amount paid, the bank would have restructured the loan, and with that comes a new tenure and a difference in total interest paid. Borrowers need to know and understand the new terms.

Think of it as your company giving you the option of a long break over a holiday period (somehow, you’ve ran out of AL), but those extra days off aren’t free, and have to be repaid back over the coming weekends. Fast forward to when you’re tired from working six full days a week, just remember the long festive break you’ve already enjoyed.

In the context of loans and interest, pausing payment or reducing the monthly instalment amount would certainly mean that you’ll be paying more over the entire loan tenure, versus the original sums before TRA. Interest (or profit) will continue to be charged on the outstanding amount – unlike your instalments, there’s no pause here – and the longer the loan tenure, the more you’ll have to fork out in interest. So, it’s not one replacement work day for every day off that you received, but slightly more.

Nearly two decades of payment for a car?

Now let’s zoom in on hire purchase loans, the kind that we take to buy cars. The situation here is slightly different compared to say, a housing loan. Home loans typically have long tenures, and adding a few years to a 30-year tenure won’t have the biggest of impacts. However, car HP loans typically range from five to nine years, and a similar tenure extension would make it very long.

Very long for a car, which has a lifespan. Some car guys would disagree, and this writer has a 30-year old car himself, but generally speaking, cars aren’t meant to be kept for decades. With rare exceptions, cars are also depreciating assets, unlike property.

With this as background, reducing your monthly car payments via TRA might not be a financially savvy move. As things stand, nine years is already a long time to be paying for a car, so any TRA loan restructure would make it unreasonably long. Compounding this is the flat interest rate nature of HP loans, as opposed to the reducing balance of your home loan – for HP loans, interest is charged on the total loan amount without taking into account the portion already paid.

Let’s take a look at this example. In the scenarios below, both borrowers opted in for the moratorium from April to September 2020 and subsequently applied for an additional three months of deferment under the TRA. After that, they take different paths.

Case 1: Current scenario of what banks are offering, which result in a long extended tenure

Assumptions:

- HP loan amount: RM80,000

- Original loan tenure: 9 years

- Remaining loan tenure (including a 6-month moratorium): 5 years and 5 months

- Flat interest rate: 3%

Borrower applied for a three-month deferment, and after that, a reduction of monthly instalment from RM941 to RM471 (50% lower) for the rest of the tenure. The resulting extension of the loan tenure is nine years and one month.

Total tenure: 5 years and 5 months + 9 years and 1 month

Case 2: New flexible repayment package by the banks

Assumptions:

- HP loan amount: RM80,000

- Original loan tenure: 9 years

- Remaining loan tenure (including a 6-month moratorium): 5 years and 5 months

- Flat interest rate: 3%

Borrower applied for a three-month deferment, and after that, a reduction of monthly instalment from RM941 to RM471 (50% lower) for six months. After the six months, he/she resumes paying original instalment of RM941. The resulting extension of the loan tenure is 11 months.

Total tenure: 5 years and 5 months + 11 months

In the two scenarios above, both borrowers (on equal terms) took up the six-month moratorium, plus a three-month deferment. As they were still affected financially, both approached the banks for further assistance. This is where the two paths diverged.

In Case 1, the borrower receives a 50% lower monthly instalment for the rest of the tenure. In Case 2, the borrower also pays 50% lower instalments, but only for six months. His financial situation improves and after the six months of halved payment, he goes back to paying his pre-Covid original rate of RM941. The resulting extension to his original remaining loan tenure is 11 months. That’s much shorter than the extension of 109 months for Case 1.

For Case 1, that’s over nine more years of interest he/she would be paying to the bank, and the overall loan tenure for the car would have gone close to two decades! Financially, that’s not ideal, and we should get back to normal payment as soon as possible to avoid such an outcome.

Make an informed decision

So, choosing to reduce your monthly payments will also increase your overall borrowing costs – there’s no running away from this. However, sometimes one has to solve the problem of today before worrying about the future, and we’re living in unprecedented times after all. Just keep the overall picture in mind and go for TRA only if you really need assistance.

Remember, this scheme is meant to offer temporary cashflow relief. Once your income has improved and if you wish to pay down your loan more quickly, talk to your bank to adjust your instalments. This will help to reduce overall borrowing cost.

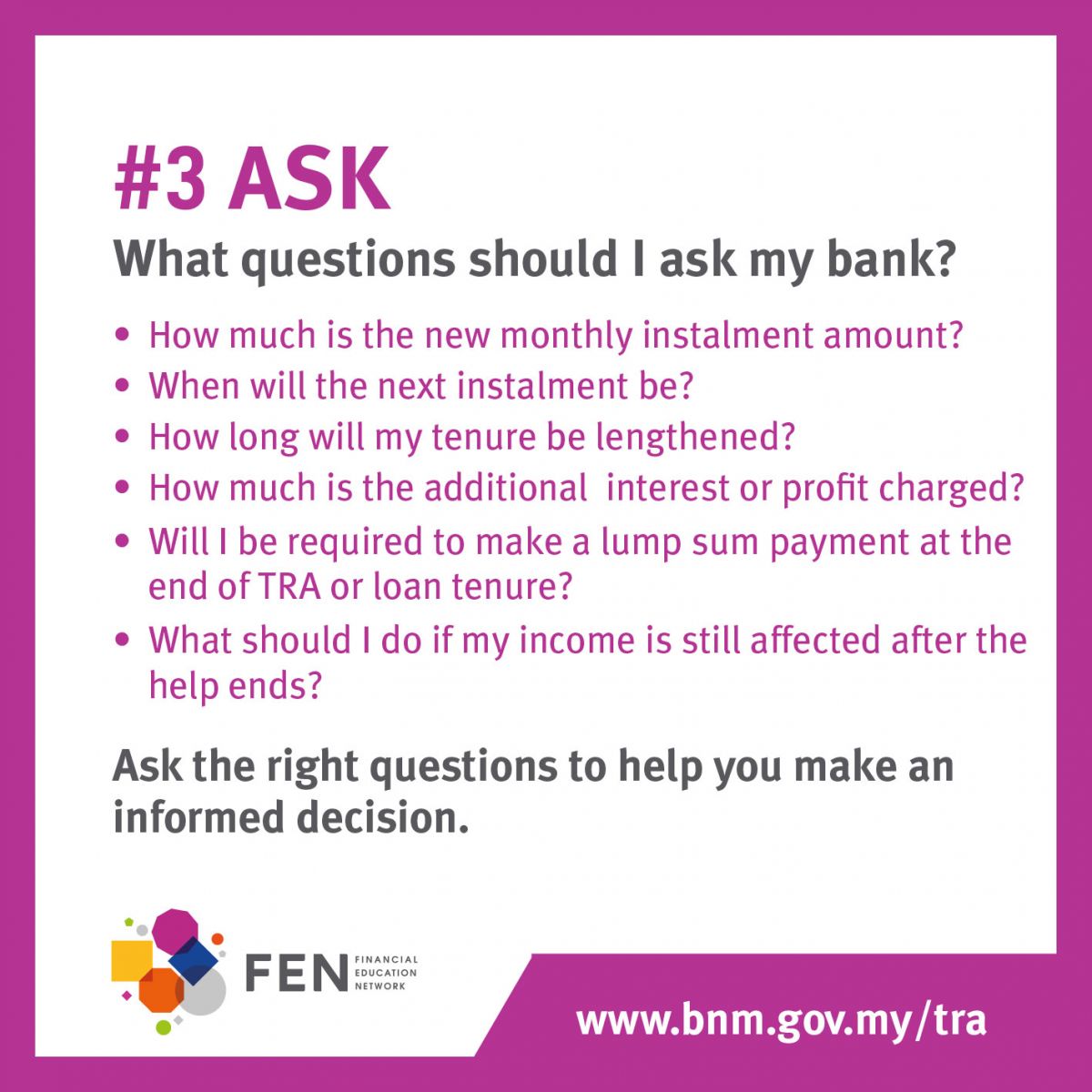

If you feel that TRA might help your current financial situation, don’t be shy to shoot any question you might have to your bank officer, and ask for the overall terms plus the added costs for comparison – they’re obliged to furnish the figures and explain the T&Cs. With the numbers in hand, you can make an informed decision.

Note that once approved, “opting out” of TRA is as simple as paying your original instalment amount (or anything higher than the TRA figure), without the need to notify the bank. But that’s for home loans. For car HP loans, once the loan is restructured with TRA, it’s effectively your new loan package and you’ll have to stick with the terms. However, if the financial situation permits and you’re ready to repay more, contact the bank.

If debts are mounting and it seems like there’s no room to manoeuvre, contact AKPK (Agensi Kaunseling & Pengurusan Kredit), an agency set up by BNM that provides a debt management programme. The programme, which seeks to develop a personalised debt repayment plan in consultation with your bank, is free of charge.

Looking to sell your car? Sell it with Carro.