We’re now only a couple of weeks away from the April 1 implementation of the Goods and Services Tax (GST) in Malaysia. Much has been said, rumoured and conjectured since the new tax regime was announced in Budget 2014, particularly with regards to the car industry and the all-important, hotly-debated question: Will car prices go up or down with GST?

Since the 6% GST will supersede the existing 10% sales tax imposed on new vehicles, it’s easy to assume that car prices will drop by 4%. Simple enough equation, but as we’ve found out, that will not be case.

“Generally, I would expect a slight drop for new cars between 1-3%,” said Royal Malaysian Customs Department GST director Datuk Subromaniam Tholasy. Malaysian Automotive Association (MAA) president Datuk Aishah Ahmad, however, isn’t quite so optimistic. “I do know some brands, prices will go up. Not everybody comes down,” she told paultan.org.

Apart from car prices, we also discussed the impact GST will have on other corners of the industry, including used vehicles, pre-registered cars, company-registered cars, servicing and parts. What will, and what won’t change? Clearly, the answers aren’t as straightforward as we may think…

GST replaces sales tax: the mechanism

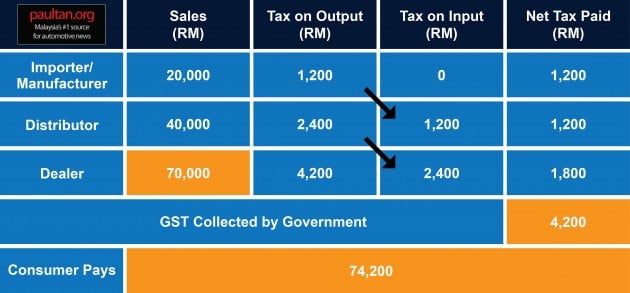

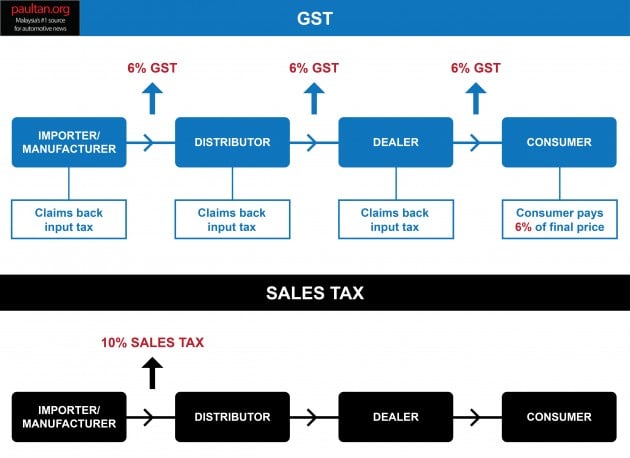

At present, all new cars are subject to a 10% sales tax. This tax is imposed on the car’s Government Approved Selling Price – that is, the car’s open market value (if CKD) or Cost, Insurance and Freight (if CBU) price, plus associated import and excise duties. It is paid only once at manufacturer (if CKD) or importer (if CBU) level, before the car is sold to the distributor. Thereafter, the car may be sold to a dealer who sells it to the consumer, with no further taxes incurred.

Come April 1, this sales tax regime will be abolished, and a GST of 6% will take its place. In its simplest form, GST is a value-added tax, that is, a tax paid on the value added to a product or service. It is applied at each stage of the business transaction, through distribution, retail and finally to the consumer.

It is important to note that it won’t be a 6% GST added on top of each and every business transaction, thereby increasing the price of the car at an exponential rate. GST is indeed imposed on the selling price, margins included, each time the car changes hands down the supply chain, but at each stage except for the final consumer, input tax can be claimed. In the end, it is the consumer who pays the full GST rate.

The basic mechanism is this: say a distributor buys a car from a manufacturer. The distributor pays the manufacturer the price of the car, plus 6% GST. The distributor then sells the car to a dealer for a higher price to account for margins, and charges the dealer 6% GST on top of that.

In filing his tax returns, the distributor will declare his output tax (6% paid by the dealer, bigger amount) and input tax (6% he paid previously, smaller amount). He then pays the difference between the two to the government.

The dealer repeats the process in selling the car to the consumer. The consumer cannot claim any input tax, so he bears the full GST burden, as stated earlier: 6% of the final purchase price. Essentially, each part of the net tax paid in the chain should add up to the 6% paid by the consumer.

How will new car prices be affected?

Subromaniam believes that given ceteris paribus – all else staying the same – the GST system should result in savings for traders, and he urges them to pass these savings down to the consumer. “Based on our computations, there will be some savings, but they will not translate to a complete 4% (10% sales tax – 6% GST). Generally, I would expect a slight drop for new cars between 1-3%, depending on whether it is an imported or locally-assembled model,” he said.

“There is a possibility that for some models there may not be any reduction or we could even see a slight increase in prices, especially for imported cars. Because it depends on the distribution margin, which is currently (under the sales tax regime) not taxed.”

The premise behind all this is such – GST is a value-added tax, which means it is a tax on distribution margins. The higher the distribution margins, the more in GST needs to be paid and ultimately, the more expensive the car becomes for the consumer.

But Aishah has slightly different sentiments. She pointed out that GST will be imposed on the final selling price of a car, including handling/inspection fees and accessories, but without road tax (which is not subject to GST). Therefore, the tax will be on a higher base than before.

“Some companies will have a slight reduction, some companies will have a slight increase in price, based on their margins and costs. To say that CBU will not enjoy as much (savings) as CKD is not true. I do know some brands, prices will go up. Not everybody comes down,” she said.

The basis behind this uncertainty concerns current unsold stock for which sales tax has already been paid – what will happen when GST is implemented on April 1? We’ll refer to this as “interim stock,” and this leads us to the next chapter of the story.

Pre-GST and post-GST stock – will “interim stock” be double-taxed?

For stock currently stored in a bonded warehouse that is yet to clear Customs, no taxes have yet been paid. As such, when it is taken out on April 1 it will be subject to a 6% GST instead of a 10% sales tax – no complications there.

“Here, we will definitely see a reduction if the cars are kept in a bonded warehouse. So even for CBU cars, there could be a reduction, depending on how the business is structured,” Subromaniam said.

But what about unsold stock that is already clear of Customs, for which sales tax has already been paid? Will double-taxation occur come GST? Yes and no – under a Special Refund scheme, the sales tax paid will be fully refunded provided the stock is held on hand as of March 31, documented proof of sales tax payment can be shown and the stock was obtained from a “licensed manufacturer.”

A licensed manufacturer is an assembly plant, Aishah explained, so this would mean CKD cars. In the case of CBU vehicles, the full amount of sales tax will be refunded to importers only if they hold the stock – if the stock has been passed on to a distributor then there will be no full sales tax refund.

Instead, they will be refunded a portion of it – specifically 2% (20% of 10%) of the value of the car at its current position. The same goes for distributors that have passed on their stock to dealers. This means the stock is effectively double-taxed.

“Assuming when the car was imported it cost RM100,000. 10% sales tax is RM10,000. But they may have sold the car to the next person, so the distributor may be holding it, after two levels, and the purchase price is probably now RM200,000. So Customs will refund the tax on 20% of RM200,000, which is RM40,000. 10% of that is 4,000, compared to the actual sales tax paid which was 10,000,” said Subromaniam.

“Legally we cannot give you (back) sales tax of 10% – even this, in Malaysia, is a concession. Most countries don’t even give (back) sales tax when they move to a new tax system,” he claimed, adding that the stock on hand is a small number compared to the total industry volume (TIV).

“Yes, we know there is a bit of embedded tax in it, but what we are saying is please try to average it out over the year. It’s going to be negligible.”

The MAA had previously asked the government for a full sales tax refund for affected car companies, but the answer was no, Aishah said. So with regards to those ineligible for full refunds, how will their “interim stock” be priced?

“It depends on whether the company can absorb the increase and is willing to pass it on to the consumer. Some companies may say look, this is a one-off thing, we will not pass it on,” said Aishah, adding that the refunds issue also involves spare parts – not everyone will get their full 10% back. Anyway, the refunds won’t be speedy – they will be given in eight equal installments over a period of two years!

Given the situation, car companies are expected to keep their stock in bonded warehouses and only let them out after April 1, while distributors will try not to shift cars to dealers unless there are ready customers, so the dealers will not be burdened by holding too much stock. There have also been cases of distributors buying back stock from dealers for this period.

Ultimately, the goal is to clear all the “interim stock” before new stock comes in. Whether the “interim stock” – double-taxed though they may be – will be priced differently from post-GST stock, depends on the company.

It has also been said that the implementation of GST could result in cash flow problems for traders as they have to pay the tax up front, and smaller dealers may feel the pinch a bit more.

The effect of forex rates on car prices

There is also the element of foreign exchange rates to consider in defining car prices, something that Subromaniam already intimated at in October last year.

Then, he had iterated that foreign exchange rates pose as the main factor in defining pricing. “We must always remember, the biggest cost for cars are not the tax components, i.e., GST, it is the foreign exchange rate.” This sentiment is also shared by Aishah.

The continued rise of the US Dollar in recent months (in mid-September 2014, RM3.22, and now, at press time, RM3.70 to the Dollar) means that a product priced as it was six months ago is now around 15% more expensive in its base form. Many companies use the US Dollar as trading currency, including Japanese automakers, even for ASEAN intra-network purchases.

If car prices go up or down, it may not be completely attributable to GST given that there are larger components that define pricing. It is also worth noting that excise duty rates can be anywhere from 65% to 105% and constitute the largest chunk of a car’s price. Higher exchange rates would therefore translate to a bigger amount of excise duties paid, which would significantly increase a car’s price. This is also applicable to auto parts.

Used cars – the Margin Scheme

Currently, no sales tax is paid on used cars (because the cars have been previously taxed). Come April 1, GST will not be imposed on the sale of a used car from one individual to another, nor on the sale of a used car from an individual to a dealer.

However, when the dealer sells a used car to an individual, the dealer has to pay the government 6% GST on the margin made. This is referred to as the Margin Scheme. It is one of the few exceptions where the amount of GST payable is not specified – for the individual, GST will be inclusive of the price he pays.

Here’s how it works. Say a dealer buys a used car from an individual at RM40,000. The individual cannot charge GST. The dealer then sells it on to another individual for RM60,000. He makes RM20,000 out of the sale, and this is subject to 6% GST, so he needs to pay RM1,200 to the government. This cuts his effective margin down to RM18,800, but the buyer will not be aware of the numbers within the sale.

Clearly, if the dealer wants to retain his profits as before, he will have to increase his prices to compensate, but there’s competition to think about – some other dealers may be able to comfortably absorb the GST component. Whether used car prices really go up or not on April 1 is anyone’s guess – market forces may yet prevail.

Pre-registered cars

Pre-registered cars are cars that have been ‘bought’ and registered by brand dealers, usually for the purposes of boosting sales numbers. For the consumer this can mean big savings, as he is essentially buying a used car that may not have been used all that much.

Still, they are considered used cars, so the same Margin Scheme should apply – the brand dealer buys and registers a car (for less than the retail price, of course). The book value of the car drops. When the consumer buys the car, GST should be inclusive of the price he pays, and the dealer will pay the government 6% GST on the margin made.

Company-registered cars – blocked input tax

If a company buys a car for private use (to be used by the director, for instance), the company pays GST on the purchase of the car, but the GST paid may not be claimed as input tax. When the company sells the car, the company may not charge the buyer GST. It’s the same rule as applied to individuals when they buy and sell a car.

Input tax can be claimed on the purchase of licensed public service, tourism, commercial, rental and driving school vehicles. This is the general rule – only when a car is acquired and used wholly for business purposes can input tax be claimed. Input tax cannot be claimed on the purchase of goods for private use. In such a case, a company-registered vehicle sold on later does not incur GST.

Accessories, spare parts and servicing

Accessories and spare parts are subject to the same tax structure as cars. Import (if applicable) and sales taxes are also imposed on them at the first level, although the excise duties paid are much less (or even zero for certain components). As such, stock brought in on or after April 1 will be subject to a 6% GST instead of a 10% sales tax.

But for existing stock that has already had its sales tax applied and doesn’t meet the conditions for a full refund, the “interim stock” problem faced by cars is mirrored here. Trouble is, the volume of spare parts is much larger than that of cars, so exhausting the double-taxed stock is going to take a significant amount of time. Somehow, this needs to be factored into the costs – there’s a possibility that parts prices may not come down in the immediate term.

With regards to servicing, maintenance and repairs, the 6% service charge will be replaced by the 6% GST come April 1 – all else remaining equal, there should be no change there.

Running costs

As has already been reported, RON 95 petrol and diesel will not incur GST, nor will toll charges, driving licence renewal and road tax. Motor insurance, meanwhile, will be subject to a 6% GST.

GST/VAT in other countries

Malaysia’s GST introduction will make it the eighth ASEAN country to implement the value-added tax structure – only Myanmar and Brunei remain as member countries that have not done so. How does Malaysia’s 6% rate stack up against neighbouring countries, and elsewhere?

Indonesia was the first ASEAN nation to introduce GST, doing so in 1984, and its initial 10% rate has remained in place until today. Thailand followed suit in 1992, with a starting rate of 10%, which has since been reduced to 7%. Singapore began its GST scheme a year later, with an initial rate of 3% (now, 7%). The Philippines currently has the highest GST rate in ASEAN, at 12%.

In all, 160 countries around the globe have implemented GST (or VAT, as it is also known by). The GST/VAT rate can vary globally – for example, Australia has a 10% rate, while Germany has a VAT rate of 19%, and the UK, 20%.

Regardless of living costs (which of course differs from country to country), the 6% rate is among the lowest in the world. Still, this rate can be considered a starting point, and it is early days yet – there is always the possibility that the rate will increase in the future.

Conclusion

There is no doubt that the implementation of GST will have a significant effect on the Malaysian automotive landscape, with particular emphasis on the market and its economics. Each carmaker works on different business models, different distribution margins, different principal requirements – the disparities are endless – so the issue of whether car prices will go up or down come April 1 is certainly not clear cut.

Regardless of how the effect of GST will be, it remains a small component of the contributors to Malaysia’s car prices; dwarfed by excise duties and foreign exchange rates. And if prices do go up (or down), it may not always be a direct result of GST. Of course, there will be teething issues, but once the difficult transitionary period blows over, the market is expected to adjust and normalise. We can only hope we get there sooner rather than later.

Looking to sell your car? Sell it with Carro.

AI-generated Summary ✨

Comments reflect mixed feelings on GST's impact on car prices, with many expecting prices to rise due to added taxes and manufacturer markups, while some believe prices may stay stable or decrease slightly depending on dealer practices. Several comments highlight concerns over inflated car costs, the political implications, and the broader economic effects like increased living costs and traffic congestion. There’s a general sentiment of skepticism about whether GST will genuinely benefit consumers, with many urging Malaysians to remain vigilant and question official promises.