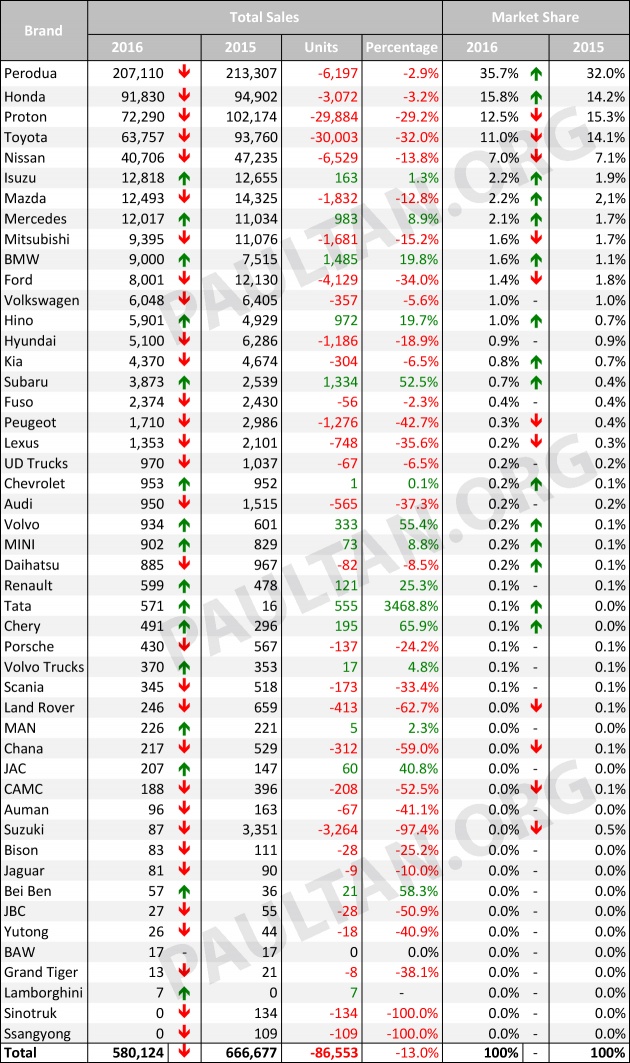

After six consecutive years of growth, including the highest ever total industry volume (TIV) in 2015, Malaysian auto sales finally saw a downturn in 2016, when registrations fell 13% to 580,124 units.

The final tally is remarkably close to the 580,000 revised forecast announced in July 2016 by the Malaysian Automotive Association (MAA), which means that everyone saw it coming – players and pundits alike (the original TIV forecast for 2016 made in January was 650,000). Consumer sentiment has not be rosy for awhile now, with a sluggish economy and a falling ringgit dominating the business pages.

“This could be attributed mainly to the slowdown in our country’s economy which impinged on consumer sentiment and business confidence. As a result, consumers and businesses were wary of purchasing big-ticket items such as new motor vehicles,” MAA president Datuk Aishah Ahmad told the press at a briefing today. Exactly what the REHDA boss would also say in a 2016 review, one can imagine.

Along with the lower sales, production of new vehicles decreased in tandem – at 545,253, output went down by 11.3% in Malaysia.

Aishah and the MAA committee members say that this year would be as challenging as the one before, and have set 590,000 units as the forecasted TIV for 2017, which would represent a marginal 1.7% increase from 2016 sales.

The club of manufacturers and distributors arrived at a flat growth based on a combination of macro and local factors. In the former category is the global economy, which is facing uncertainty surrounding the post-Brexit era and also the protectionist policies of US president-elect Donald Trump, who loves to aim threatening tweets at carmakers. Emerging markets such as Malaysia have been affected by these trends.

Locally, Bank Negara expects the economy to expand by around 4% to 5% this year, which isn’t stellar, but is something most would take given the circumstances. Private domestic demand would continue as the key driver of economic growth.

Malaysian household debt is the highest in the region though, which is why banks will continue the stringent approach when it comes to approving hire purchase loans. This has affected car sales in the lower end of the market, and is expected to continue to do so, Aishah said, pointing out that those earning below RM3,500 have found it hard to get HP loans.

Of course, the continued depreciation of the ringgit is not good for both rising import costs of MAA members, as well as consumer sentiment. Should inflation rise, buying a new car would naturally drop down priority lists. Another interesting factor cited by MAA is the rise of app-based ride hailing services such as Uber and Grab. This trend could have a “slight impact” on auto sales as some urban commuters might see a reduced need to own a car.

On a brighter note, the multiplier effect of mega infrastructure projects like the MRT (first portion of Line 1 in operation now), LRT extension and new highways could give a boost to the local economy, which in turn might lend a hand to car sales. Of course, the introduction of new models at competitive prices will also sustain buying interest.

Less than three weeks into the year, and we’ve already seen Honda (which overtook Proton to be No.2 in sales) introduce the new seven-seater BR-V, while Perodua’s facelifted Axia is now in showrooms. While the top national and non-national brands are strengthening their positions, this will be a busy and challenging year for all players. Expects aggressive promo campaigns and innovative strategies designed to lure punters into showrooms.

So, are we looking at signs of stagnation and a saturation point? Are car sales heading down for good or are these just speed bumps? “The auto industry is a cyclical business,” was Aishah’s reply. Looking forward, “there will be growth, but don’t expect double digits… it (car sales) will correct itself, but it will take some time,” she said, pointing out that the current crunch is nowhere near the what the industry faced in the depths of the 1998 financial crisis.

MAA’s TIV forecast for 2018 to 2021 show annual growth of between 2% to 5%. Lean times, yes, but one suspects that the car industry – and Malaysians’ love for the automobile – is merely taking a breather.

Looking to sell your car? Sell it with Carro.

AI-generated Summary ✨

Comments reflect concern about flat or declining car sales in Malaysia, with some criticizing industry predictions and government policies. There is skepticism about Proton's competitiveness, debates over car prices and government promises, and calls for local automakers to innovate. The overall sentiment shows worry about economic challenges affecting the auto industry, but also pride in local brands and a desire for better value, with some optimism about new partnerships and market opportunities.