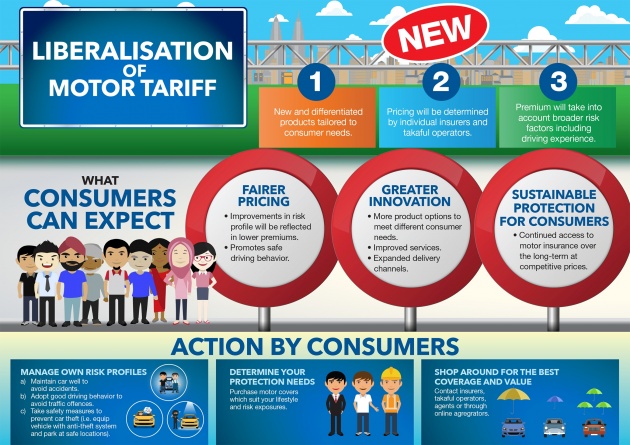

As it gets closer to July 1, when the liberalisation of motor insurance tariffs in Malaysia kicks off, the General Insurance Association of Malaysia (PIAM) has again briefed consumers that many factors will come into play in determining premiums and that pricing is set to differ between insurers. It also said that those with poor driving records are set to look forward to higher premiums.

Speaking to The Sun, corporate communications manager Kuan Shook Quan said that as outlined by Bank Negara Malaysia (BNM), pricing will be determined by individual insurers and Takaful operators based on a risk-based assessment system.

As such, how much one pays for insurance will no longer be determined by fixed price lists, but by his or her risk profile. This means that theoretically, no two insurers will have identical pricing for a motor comprehensive policy.

Kuan said premiums will thus be charged based on the risk profile of the insured, in addition to the present model, age and cubic capacity of the insured vehicle. Risk factors will include driving habits, age of the driver, claims history, usage and safety features of the vehicle.

As mentioned previously, premiums may be driven by other factors. These could be safety and security features in the vehicle, duration that the vehicle is on the road geographical location (areas with higher incidents of theft) and traffic offences on record.

“There is no fixed system of calculation, but several standard risk factors will be considered by insurance companies. Driving behaviour, experience and claims records are expected to be factors for consideration in risk profiling to determine the premium,” she told the publication.

Kuan said this new policy should translate to lower premiums for lower risk drivers with good records on the road, while repeat traffic offenders will naturally have to pay more. However, this can be moderated by risk reduction factors undertaken by the policyholders.

She added that different insurers will have different ways of defining the risk profile group, and as such the price of a motor policy will differ from one insurer to another. “They should shop around and get the best insurance coverage that meets their needs and at a price best suited to them. However, consumers are cautioned that a lower price does not mean a better product. Proper assessment and due diligence must be done,” she said.

More on the subject, here:

Motor insurance liberalisation: how will it affect you?

Liberalisation of comprehensive motor insurance – Bank Negara expects no massive shift in pricing

Tariffs for comprehensive motor insurance to be lifted in July, full liberalisation in 2019 – PIAM

Looking to sell your car? Sell it with Carro.

Modified Saga dan Myvi most high risks.

So what will happen to Axia and Myvi? These cars not only got no VSC BUT no ABS even (Axia)

Malaysian Government said if all cars had VSC, accidents and deaths can be reduced by 45%

This would mean, insurers will hantam higher premiums on cars with no VSC, and even higher premium on cars with no ABS

But it is not the consumer at fault. We consumers want VSC and ABS. It is our national car company that does not give VSC. Saga owners also affected.

I hope the liberalisation puts a hefty premium to >20 year old Wira and Iswara. This will force them to buy quality new Protons. The Iriz, Persona, Suprima all are Volvo-like standard and have coldest aircond in the world.

Ahbeng vios is highest on the list, especially those pre-ESC generations

Our insurans is the cheapest in the world. Why complain?

Our cars also the cheapest in the world. We should be grateful instead of complaining

Betui betui betui!

cheapest? Proof??

no need proof. This is the guy who said Proton Saga all had VSC

One thing I curious, do they still have the NCD structure?

Yes

The Sun newspaper did mention NCD still remain the same.

They think we born yesterday.

Naik, jangan tak naik.

All this liberalisation have no meaning when PIAM themselves cannot sort out the insurance fraud in the industry which is so rampant. Basic also PIAM cannot do but want to do all this liberalisation.

This new system will eventually raise tariffs and premiums and this is because Insurance companies cannot sort out their own fraud which they know exist.

To all the insurance companies under PIAM pls don’t pretend to be innocent. You all know damn well that every adjuster of yours is working hand in hand with the police, investigation officer and the car workshop to get kickbacks. I myself had many accidents.

Infact the last accident I had, I sent my car to my own friend workshop, he said he will repair everything for RM1000. I tried another workshop, he assessed the repair to about RM1200. I thought, nevermind, I will send for insurance claim and I can save the RM1000.

So, I sent the car to the panel workshop. After repairs and all that, out of curiosity, I simply called the insurance company up to find out how much was the bill, it was shockingly RM8000. Yes, 8x the actual amount if I had the car repaired by myself.

We all know what happens. The IO (Investigating Officer), the Adjuster, as well as the bengkel and the ulat ulat runner boys will get their kickback. Biggest kickback would be the adjuster. At least he makan few thousand for his personal pocket.

The Insurance companies know about all this. Hundreds of cases happen everday. But they close an eye. They pass the problem and burden to the consumer with higher premiums. This PIAM cannot sort, they want to do liberalisation?

PIAM, you know this happens but you too close an eye. This results in higher burden and premiums for the public and now, this new liberalisation, which is utter bogus.

I repeat, you also know about all this. But PIAM just keep quiet. You all just close an eye because the problem now goes back to the consumer with higher premiums.

With all this shit going on the Insurance industry dare to increase the car premiums for the motor industry every year and now, do this system which will make them more money.

That is Malaysia for you. The rakyat suffer the most because there is no proper enforcement and the insurance industry is full of cheats.

Everybody suffers when everybody along the line gets kickbacks from the police office, the police cameraman, the adjuster, the bengkel and the runner boys (ulat ulat).

The Motor Insurance Industry collected no less than RM100 billion in premiums last year. It is not fair that we public have to pay higher premiums because they cannot sort out the fraud in their own backyard.

Trust me, premiums will go up no matter what PIAM says.

No wonder kickbacks, corruption and donation so rampant these days.

No shit.

Only via insurance claim can Myvi bumper + knock/respray costs RM8k to fix. I personally saw the tax invoice before, and that was done in one of Perodua’s body and paint branch, registered on Perodua’s website.

Otherwise, who the hell wanna fix bumper for RM 8k? Don’t say RM8k, RM2k also people will think is bloodsucker price if they had to pay for it themselves.

Complaint to MACC with evidence.

In short, U are saying “The end does Not justify it’s mean”. Thanks YBK.

Whatever the pricing to be determined, I am very sure it will go UP, UP and more UP……

Depends on ur driving profile. A lot of factors in play, similar to banks wanna gip u loan or not or loan with super high interest.

just how low is possible with this new pricing standard? or this is just another reason the provider to charge more

YB Kunta Kinte, you hit it on the nail. You are my man! We consumers in Malaysia are constantly being penalized for the weakness in our system

So consumer paying more just for that free payung and mug

The bright side is the Payung helps U when it rains & the mug helps 2 keep your Coffee warm.

complaint also no meaning…must renew insurance… maybe the goodies from insurance company will come back…

20ish old boy can kiss goodbye to their Golf GTI. The premium will be higher than the car itself.

“With liberalisation, many factors will determine pricing of comprehensive motor insurance premiums – PIAM”

So it means lot of reasons to charge you higher!

meanwhile the 40 year old incompetent accountant driver gets low premiums while they very competent 23 year old fresh graduate gets penalised for being a “fresh graduate”….used car sales will also suffer as the premiums for them sure will skyrocket

Meanwhile, women drivers get cheaper premium because they’re safer driver.

While on the internet, we see women drive on wrong side of the road causing deaths, fail at simple task like side parking an auto Myvi, etc.

Vision but do you have the big data to support this? What about personal privacy?