Motor comprehensive insurance has moved into the second month of its phased liberalisation, and according to Bank Negara Malaysia (BNM), some early trends have emerged in the first month since the switch began on July 1.

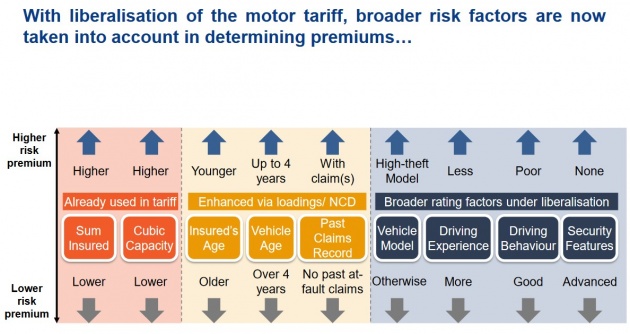

Full detariffication will only take place in 2019, but the short of it is that vehicle insurance premiums are now no longer calculated on a fixed rate basis, but on a risk-based assessment system. A number of factors will determine how insurers and Takaful operators price their premiums, and pricing is set to differ between insurers.

This means that theoretically, no two insurers will have identical pricing for a motor comprehensive policy, and consumers will have to shop around for competitive pricing rates and coverage that best meets their insurance needs.

The central bank has revealed some observations of some things that have come about in the first month of detariffication. Based on pricing models of 11 out of 26 insurers sampled as at end July 2017, it said that premium increases and decreases within a range of +/-10% were observed across all risk pools.

This suggests insurers are appropriately differentiating between lower and higher risks consistent with more equitable pricing. It added that a reasonable dispersion of premium adjustments that were less than +10% was observed, suggestive of more refined pricing models by some insurers.

Meanwhile, downward adjustments in premiums were more prevalent for newer cars compared to older cars, but no significant differences were observed across vehicle makes and models, which may

indicate a more cautious approach taken by insurers before fully reflecting risk factors in price adjustments.

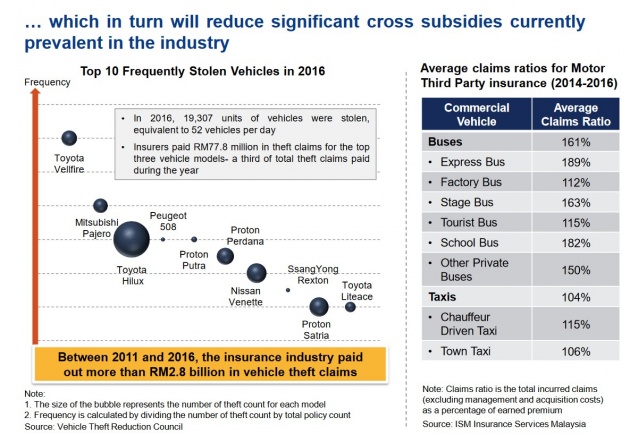

It added that in the initial phase of liberalisation, this is likely to tamper the effects of premium adjustments across risk groups, though an exception was observed for high theft-prone vehicles, which are likely to attract higher premiums.

The central bank also noted that premiums generally decline with age, reflecting higher risks associated with younger and less experienced drivers, in particular below the age of 25 years. It however added that some policyholders within the age band of 40 and 50 years old might experience marginally higher premiums, which is partly attributed to the use of their vehicles by young adult children of driving age.

Interestingly, in the first month of liberalisation, higher premiums were observed for vehicles in West Malaysia than those in Sabah and Sarawak – BNM attributes this mainly due to differences in risk levels and risk exposure arising from traffic density and road conditions.

It added that the observations do not take into account more specific individual risk factors that insurers may apply in calculating premiums for individual policies, where an insurer can apply additional factors to adjust premiums either higher or lower than that indicated by their pricing models.

If you’ve started paying for a motor comprehensive insurance policy from July 1, has there been an increase or decrease in your premium, and was finding the right policy a fuss-free affair? Share your views with us in the comments section.

Looking to sell your car? Sell it with Carro.

AI-generated Summary ✨

Comments highlight concerns over increased minimum third-party insurance premiums and the need for clearer, more comprehensive policies that include wider coverage like LLP and LLOP. There’s support for risk-based underwriting, discounts for long-term NCD holders, and mandatory excess for young drivers, but also criticisms about potential inequality, especially for lower-income owners. Some mention difficulties comparing premiums and advocate for transparency and better mobility options. Overall, users are cautiously optimistic but want reforms to make insurance fairer and more understandable.