Just look at these scenes from Shah Alam yesterday evening. According to Selangor bomba chief Norazam Khamis, the flood around the Shah Alam Stadium in Seksyen 13 was around 1.2 metres high. It was reported that water rose up to chest level following heavy downpour that went on from 3pm. Other areas affected by the flash flood included Seksyen 9, 10, 4 and 7.

Everyone knows that this isn’t an isolated incident; it was Shah Alam yesterday and it could be Cheras, Puchong or KL city tomorrow. Some areas are more susceptible to flash floods than others, but development and new infrastructure has introduced flooding to more areas now, and weather seems to be more severe these days, and not just in Malaysia too. Experts have pointed to global warming as the cause.

When we come across news articles or forwarded WhatsApp pictures of floods, the usual reaction is along the lines of “wow, it’s quite bad” or “finish la all those cars”. It feels like someone else’s problem if your home is not in a historically flood-prone area, but what about where you’re going?

Whether a parking lot in the city centre or on the Federal Highway en route to Klang for makan, you could be walking into the eye of the storm without realising it. And these things happen fast, usually too fast for one to escape, and that is if there’s a way out.

If you have been renewing auto insurance yourself, as opposed to handing it to a runner or agent, you would be familiar with flood coverage or special perils, which includes cover for natural disasters and acts of God. Tick these optional boxes and you’ll be reimbursed by the insurer should your car suffer damage from natural disasters, at a fee of course.

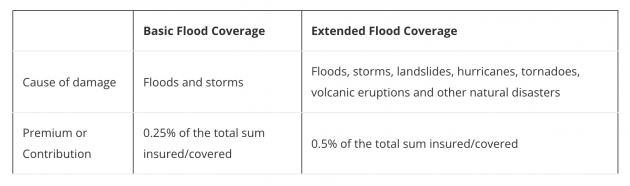

What’s the typical cost? Allianz offers special perils coverage for 0.25% of the vehicle’s sum insured, and this includes cover against floods, typhoons, hurricanes, storms, landslides, landslips and other convulsions of nature. Etiqa offers the same for 0.5% of the sum insured, but there’s also a “basic flood coverage” (floods and storms only) for 0.25%.

From my own plans with Etiqa, basic flood coverage seems lower at 0.225% – see the samples above. Basically, at 0.25% of insured value, it’s an extra of RM125 for a RM50k car and RM250 more for a car valued at RM100k.

An example is your car being crushed by a fallen tree caused by a storm. You won’t get a cent from the insurer if you did not go for the optional special perils cover. If you did, and the car is declared a total loss, you will be compensated based on market value at the time of incident, or agreed value if you paid more for that fixed sum option.

If getting caught in a flood can happen to anyone, then why doesn’t everyone add on flood or special perils coverage to their car insurance? Of course, it’s to save money, and I have been guilty of that as well back in the day. We think that it won’t happen to us because our area is low-risk, and if we’re careful about where we park.

When you’re deciding whether to tick the box, you might also remind yourself that nothing ever happened the times when you did go for extra cover, and the premium went to waste. The same goes for windscreen cover.

“As a claims professional I cannot emphasise enough how important it is to always add-on special perils cover to your motor insurance. Sure, you would be spending a little extra on your motor insurance premium, but in hindsight, it is an investment that protects your vehicle against unplanned events and calamities,” said Damian Williams, head of claims at Allianz General Insurance Company.

“Just because you do not live in a flood-prone area, it does not mean that a flood will not happen. Every year, we see a lot of these incidents, and unfortunately, only a fraction of people can experience a claim when it comes to flood damage,” he added.

If you’re an uninsured victim of flood damage, is there any form of recourse? The government and DBKL have went on record to say that they will not compensate flash flood victims because it’s an act of God. One can argue the last point – pointing to insufficient drainage, poor planning, etc – and try to sue the local authority, but that would involve much time and resources, not to mention legal fees – better to just pay the 0.25% of sum insured in the first place, no?

It goes without saying that the more protection you have, the better, but that’s assuming that protection is free. Extra cover for your car comes at a cost, as you’ll discover by ticking all the option boxes available, but seeing how frequent, unpredictable and severe flash floods can be here in Malaysia, basic flood coverage should be the first name on the team sheet, as they say in football – in other words, a must have.

Ask yourself this: is the likelihood of your car being stolen so much higher than it being caught in a flood, so much so that protection for the former is maximum, and zero for the latter?

Looking to sell your car? Sell it with Carro.

Just drive Toyota Hilux then don’t need to worry about flood….

Toyota Hilux failed to tackle 1.2m level flood float like a wandering rubbish and not forgetting embarrassing result on moose’s test as well ….

Which model Hilux are you referring to that failed the Moose’s test? DOn’t confuse ppl with your outdated info la pls.

every year model came out has not been rectified, sweeping under the carpet marked as outdated info. dont be lazy go search youtube latest was one month ago

Need to understand why you buy Hilux in the first place. Majority Hilux owner use it on highway and private car. Occasionally with some cargo at the back. This is a pickup truck meant for working environment.

The car is tall and quite narrow. With a powerful engine. Every Hilux driver think they are driving a Ferrari on highway.

Don’t drive so fast when come to corner, you know know it!

People will go to this extends. Bring all the cars to an old secluded workshop. Set it on fire including the workshop. Claim for fire damage.

Sediakan payung & perahu sebelum hujan lebat

Seems like tadium Shah Alam is also the detention pond.

So any housing or office nearby not affected.

park on upper floor carparks if u can

yup i always include special peril during ins renew after witness flooded open car park near klcc/pavilion. and then flash flood just can occur anywhere anytime in msia season.

im suprised more people that i know rather take windscreen protection than special peril

To those advocating special perils and flood coverage, be clear of the terms and conditions. They don’t apply if your car is parked and you’re not in the car.

Just curious effects on EEV.

Woohoo, more ‘accident’ free used cars on sale at unbelievable price .

during rainy season, better ride kapchai…..At least, if damaged, it wont cost a bomb to repair.

Badan basah boleh kasi lap.

time for malaysia to legalize hovercraft on the road.

Ever since I worked for an insurance agent and also worked near Pavilion before, plus knowing that Malaysians started to have the tendency of having demonstration, marching and etc, I’ve included all special perils in the first year of car ownership, yes including potential demonstration turn riot and burning cars around.

Just in case, you might think it’s not necessary but you’ll only need it to protect you once to appreciate it.

Flood*

2nd car dealer –

mechanic –

Spare part dealer –

Natural disaster or due to human activity will happen in no time or sign.

Even in KLCC area also there is a flooding case and damage a lot of cars in the basement.

At the end, if you can afford to have extra insurance coverage, why not. Otherwise take the risk.

Choose your parking wisely from experience.

Sue DBKL collectively. Share legal fee with many victims. Sure win one