We continue to look at how each bank is handling the Pemulih six-month bank loan repayment, which was announced last month and is eligible for all Malaysians. This time, we’re focusing on Public Bank, which has released details of its own offerings as applications open today.

As with the other banks, the company is offering either a full deferment of instalments or a 50% reduction – both for a period of six months – under its Targeted Repayment Assistance (TRA+) scheme. This offer is open to all hire purchase and AITAB Hire Purchase-i car loans for individuals (B40, M40 and T20) and micro enterprises, with automatic approvals for those who opt-in. Small and medium enterprises (SMEs) that have been financially affected by the coronavirus pandemic may also apply.

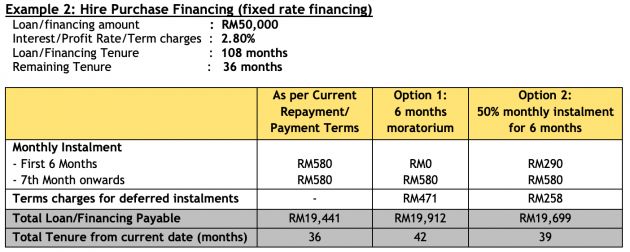

It’s important to remember that the moratorium is not a loan waiver, so you’re not getting six months of “free instalments.” Rather, if you select the first option, your loan tenure will be extended by six months and will be accompanied by higher interest, as the latter will continue to accrue during the deferment period. There is, however, no compounding interest applied.

As for the second option, the tenure will be extended by three months, with the customer paying the usual instalment amount during this period. The bank did not specifically mention when the additional interest is payable for both cases, but it should be included in the final instalment in one lump sump, as is the case with the other banks.

Like RHB and AmBank, Public Bank did not provide an example of the deferment in numbers, but the scheme should work identically to Maybank’s example, as shown above. Of course, the interest will vary according to your loan amount, remaining tenure and agreed interest rate, so you should confirm the details with your bank before you decide to delay your instalments.

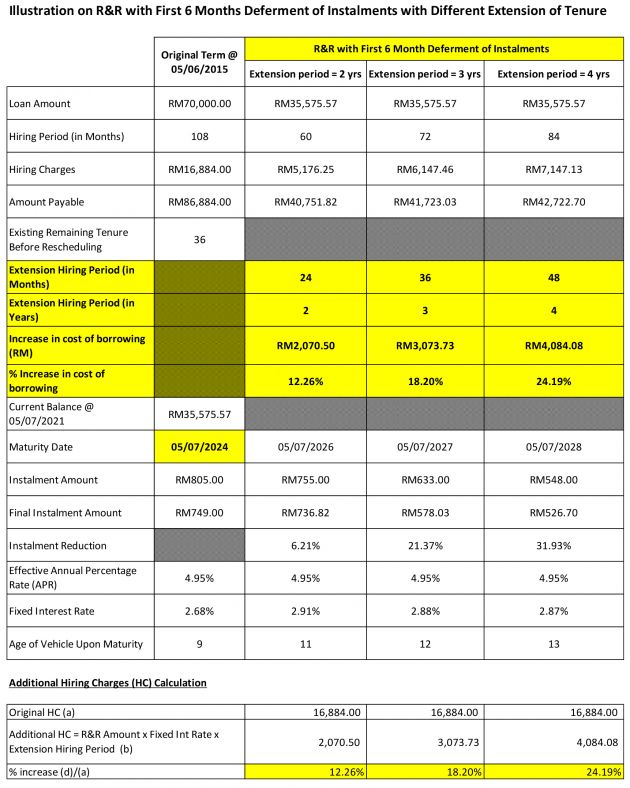

Public Bank is also offering a customised payment schedule that includes a six-month deferment of instalments and reduced instalment payments through an extension of the loan tenure of up to two years. This is applicable to all individual and business customers who have been financially affected by the pandemic, with approvals subject to the bank’s terms and conditions and sole discretions.

This third option essentially means that after deferring your payments, your monthly instalments will be slightly lower, although you will be paying for a longer time. The catch is that your interest rate will also be higher, so you’ll be paying more for your car in the long run.

The example given by Public Bank shows a nine-year loan amounting to RM70,000, with an interest rate of 2.68% per annum and monthly instalments of RM805. The borrower opts for the customised plan with three years remaining; the RM35,575.57 still owed to the bank is effectively refinanced into a five-year loan with an interest rate of 2.91% and monthly instalments of RM755, payable immediately after the deferment.

As the table shows, the borrower will be paying an extra RM2,070.50 due to the additional interest, which appears to be prorated so they won’t be massively shocked by an enormous final instalment. Oddly, the company also provided examples for three- and four-year extensions, even though the scheme is capped at two years.

Unlike the previous targeted assistance offered by banks, you won’t need to provide any documents nor any proof of a pay cut or job loss. All you’ll have to do is apply either online or manually through email (to [email protected]), the account holding branch or the hire purchase centre where the loan was made, using this form.

Aside from Public Bank, banks that have announced their Pemulih moratorium options include:

Looking to sell your car? Sell it with Carro.

Saya dapat ke untuk mohon loan ini

Ada sapu dulu… bayar blakang kiraa

Don’t waste money to buy car if U cannot afford one. Or just buy something cheaper

But my 2015 supercar myvi 1.5 extreme only worth 24k, loan outstanding still 30k.need to top up 6k to sell. I can’t afford to sell my supercar for something cheaper.

Copy paste: “All you’ll have to do is apply either online or manually through email (to [email protected])”

Bagus untukrakyat

Bagus

something wrong with the sample calculation. the balance of the 70k loan (after paying for 6 yrs) should be 35.5k. It should be less than 805×36 =29k.

Same.. I can’t brain the computation part of the additional hiring costs as well..

How can applic 6 month moratorium ?

Copy paste: “All you’ll have to do is apply either online or manually through email (to [email protected])”

For Maybank example;

Total Additional Interest;

= 6*RM580*2.8%*3years

= RM292.32

Even I calculate 3.5 years;

= 6*RM580*2.8%*3.5years

= RM341.04.

But the example shows RM471, significantly greater than both either 3.0 or 3.5 years calculation above. Now please explain how there is no compound interest.

Less is said about the Public Bank calculation the better, as the outstanding amount (RM35,575.57) is already wrong in the first place.

I cant find the 6 months full deferment public bank page

Housing loan

Macam mna nk dapatkan dan nak thu acc bank loan pnjmn kreta yer… Dlm aregmnt cri xjmpa… Sbb nk apply moratorium online kna isi ic kita dan acc bank

Monthly bayar kepada bank apa?

need to apply for memotarium

ALREDY I APPLY FOR MORATARIUM 6 MOUNTH. BUT NEED TO OTP NUMBER,LAST TIME I USE ANOTHER FON NUMBER.THEN I CL HELPLINE BUT NEWER ANSWER MY FON..PLC GIVE ME HOW TO I APPLY…THIS IS MY NEW NUMBER 0127902174 OR EMAIL ME…TQ

moratorium for car loan 6 month

Already opt-in on July 9. As they said the bank will contact you in 5 working days. Until now July 21st, they never did…

I apply this moratorium for car loan use online but the OTP number has been given to my old phone number and is no longer used. Then I use the form provided but when using the e mail address given it is not possible. can you please give me some advice

Hi, I suggest you go to your bank update your mobile number will be better. You may try register this HP moratorium with banker straight away or you print out form to fill up, direct submit to bank.

need to apply 06 month moratorium

Very good