On June 28, prime minister Tan Sri Muhyiddin Yassin announced a six-month loan repayment moratorium for all Malaysians, like what was announced in the first movement control order (MCO) last year. The moratorium is available to everyone, from the B40 through to T20 segments as well as SMEs and micro entrepreneurs.

The key difference from the first loan assistance last year is that this time, there is no need for applicants to provide proof of a reduction in pay or the loss of a job – no documents are required. Borrowers will however still need to apply with the bank and sign an amended loan agreement form to have the order on black and white. The approval is automatic for individual borrowers, and should come within five days.

To that end, Maybank’s Covid-19 financial relief scheme is now live, and borrowers can now apply for repayment assistance from today. Maybank can be contacted on its customer careline at 1-300-88-6688, or +60378443696 for overseas customers, or via e-mail at [email protected]. Alternatively, customers can make an appointment to visit a Maybank branch, Auto Finance Centre or Regional Asset Quality Management Centre. Customers can also apply through maybank2u from July 20.

Borrowers need to remember that the moratorium is not a loan waiver, and you do not get six months “free rental.” Focusing on vehicle hire purchase, the repayment assistance plan by Maybank for individual customers has two available options – the first is a six-month deferment on monthly instalments, while the second is a 50% deferment in monthly instalments for a period of six months.

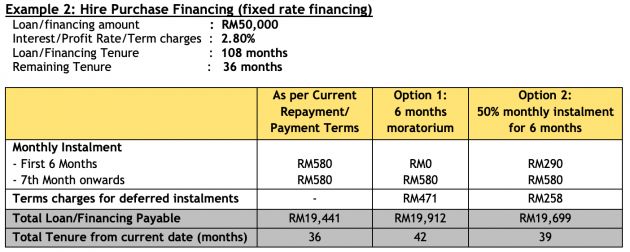

The sample scenario provided by Maybank illustrates a nine-year loan for RM50,000 at 2.80% interest, with a tenure of 36 months remaining. Here, the borrower’s monthly repayment sum is RM580, and the remaining amount payable is RM19,441 over the remaining 36 months, as laid out by the normal repayment terms without the moratorium or 50% monthly instalment rate over six months.

Taking the first loan deferment option, which is a six-month moratorium on the monthly repayment, the customer gets to postpone the monthly repayments for six months, and the borrower’s monthly dues of RM580 is resumed on the seventh month.

Term charges of RM471 are applied for the Option 1 arrangement, and the total loan tenure is extended by six months to 42 months. This comes to a total payable sum of RM19,912 for the loan, which is the RM471 in term charges added to the original remaining loan sum of RM19,441.

For Option 2, this is offered as a 50% monthly instalment, also for a duration of six months. This means the original monthly instalment of RM580 is halved to RM290 for the first six months of taking up the moratorium, with the original RM580 monthly sum resuming when the moratorium period ends six months later.

Option 2 is almost a halfway-house between Option 1 and the original hire purchase arrangement, where it brings RM258 in term charges for the 50% deferred instalments on top of the original RM19,441 remaining amount, for a total of RM19,699.

Here, three months are added to the original remaining loan tenure at the start of the moratorium, for a total tenure of 39 months, compared to the six months added by taking Option 1. In both cases, Maybank says the additional interest or profit will be charged on the principal based on the annual percentage rate (APR), which the borrower will pay at the end of the tenure together with the final instalment. Term charges will vary depending on your loan amount, tenure and interest rate.

Customers of Maybank who apply for either deferment option will only need to sign a self-declaration form in order to submit their application, and will be contacted by an officer of the bank to inform the customer of their application status.

Aside from Maybank, banks that have announced their Pemulih moratorium options include:

Looking to sell your car? Sell it with Carro.

Tengkiu kjaan Penyayang dan Perihatin!

Rakyat terbela.

#KeepCalm&SyukurON

Why is there a term charge for hire purchase when the government clearly stated no penalty or compounded interest can be charged? So do they just change another terminology to charge us?

Well, term charge is neither penalty nor compounded interest. Penalty is for when u dont pay, compounded interest is when u dont pay again.

Legally the bank is right…morally is up to the bank….

This loan moratorium intended to help those in need but in the end those in need have to pay the bank extra for assistance in the long run. what a world we live in :D

bayaran tambahan Rm471 untuk semua jenis pinjaman atau berbeza bagi setiap peminjam. kalau berbeza bagai mana cara pengiraannya?

Above is just an example how the extra interest is calculated, you have to plug in your own loan figures and work out the extra interest for your part.

This is how government treat us. Always got hidden agenda . Nobody to help us. Millionaire getting millions poorer getting poorest. Sorry malaysia

Kalau ikutkan ada persamaan dengan compounded interest. Ini bukan sahaja menolong tetapi mengambil profit diatas permasalahan rakyat. Keuntungan sudah dapat dari perjanjian asal tetapi there are still additional charges levied even if they know people are facing the financial problems & difficulty surviving.

Memang ada persamaan dengan compounded interest. Ini bukan sahaja menolong tetapi mengambil profit diatas permasalahan rakyat. Keuntungan sudah dapat dari perjanjian asal tetapi there are still additional charges levied even if they know people are facing the financial problems & difficulty surviving.

Banks institutions is a REAL! Ah Long.

For sure many people will ignore this moratorium and unable to pay montly installment.

I got 50% reduction 22Aug where my payment date is 7th of the month…so in next month i try to pay 240 through maybank deposit machine but it shows transaction unavailable (main installment -478, after50%-239)..

So my ques is,

1. why they refuse me to pay since o have to pay 50%?

2. If maybank approved u for option 1 moratorium, are they gonna block my car account for those 6 months..

Nedd advice.

Thanks