On June 28, prime minister Tan Sri Muhyiddin Yassin announced a six-month bank loan repayment moratorium for all Malaysians. It’s similar to what was offered in the first round of the movement control order last year, and applications are now open.

While financial institutions have continued to provide targeted loan assistance to individuals impacted by Covid-19 and movement control orders, under the latest Pemulih plan, the moratorium is for everyone – that’s right, from the B40 segment to even the country’s top 20% earners, and micro entrepreneurs.

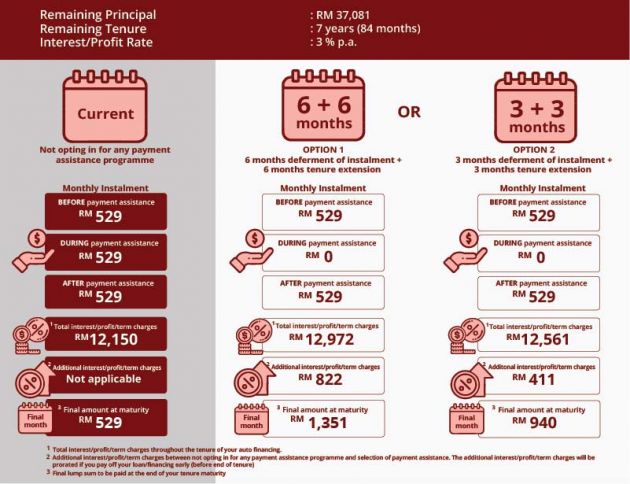

CIMB’s Covid-19 relief measures and support page has now gone live, and here we take a look at what’s required, with a focus on car loans.

Basically, the bank offers deferment of instalments for three or six months, and customers can choose one. If you have more than one loan account, you’ll need tell the bank which one (or all) you want to enter the programme. CIMB can be contacted at 03-62047788 or [email protected]. Depending on where you’re at, some branches may be open, but opening hours have been reduced – check before you head there. One can apply via this eForm.

So, the details. First, you will need to remember that the moratorium is not a loan waiver – you’re not getting three or six months “free rental”; instead, your payment has been deferred, and the loan tenure will be extended by six months as a result. Note that the total interest paid is higher as a result of the tenure extension.

CIMB’s example scenario above is a seven-year car loan at 3% interest rate. The remaining sum is RM37,081 and the borrower’s monthly payment is RM529 per month. Those who take the six-month moratorium will pay a total of RM12,972 in total interest over the loan tenure, as opposed to the original RM12,150 – that’s a difference of RM822. If you pay off your loan early, this additional interest due will be prorated.

This additional RM822 of interest will have to be paid at the final month of your loan tenure, which will total RM1,351 (529 + 822). This is opposed to spreading it out over monthly payments after the moratorium ends. For convenience, you’ll pay the same RM529 that you remember after the six-month pause ends. Pretty straightforward.

So, do opt-in if you need the assistance, but be fully aware that doing so incurs additional interest charges. Also note that this extra interest is from the loan extension and it’s not compounded. Of course, it will vary according to your loan amount, remaining tenure and the agreed interest rate.

Unlike targeted assistance, one does not have to furnish proof of a paycut or job loss – no documents are required. While it’s open to all individuals, and approval is automatic, borrowers still need to apply with the bank and sign the amended loan agreement form because things have to be on paper, in black and white.

Don’t be put off by the application process, because approval will be automatic for individual borrowers. Small and medium enterprises (SMEs) can also apply, but for companies, it’s subject to review by the banks and not automatic. Also, another important point is that accepting the loan pause will not affect an individual’s CCRIS status and rating, so proceed with peace of mind.

If you want to apply, contact CIMB and they will get back to you within five days to arrange for the signing of documents. By default, the loan pause starts the following month after your application, but if you wish for it to start in July, do let the bank know. Also, if you’re already on a payment assistance programme, you can switch to this, but you’ll need to talk to the bank about it.

CIMB also mentions that this programme applies to newly approved/newly disbursed car loans as well – you can apply the same way. Contact CIMB via phone or email (details above) if you need more info, and you can walk into a branch if you wish. You can apply via this eForm.

Aside from CIMB, banks that have announced their Pemulih moratorium options include:

Looking to sell your car? Sell it with Carro.

For borrowers, it help on your cash flows during this moratorium periods. Bank get extra interest income (basically the amount deferred will be charged with interest for the remaining tenure). RM529* 6 mth * 7.5 years * 3%= RM714 (lower than bank calculation).

No free lunch this time…

Reality check, if free lunch is given nobody will appreciate it. At the least this gives options to debtors some breathing room to manage their finances today and only worry later. Those who desperately need the money won’t be quibbling about the terms.

It’s not even a free lunch before, you have to pay more for the same dish.

differing payment still benefits the loaner as you can use the money since the value of money six months after when your loan suppose to expire is less than the value now.

Let’s take first.

RM529 x 6 = RM3174

but…

3174 x 3% = RM95.22

7 years = RM667

8 years = RM762

9 years = RM857

Seems like they are compounding on the interest

It’s rule 78

basically means, just let u die later only

Not much enough for future to die.

Those who desperately need the money won’t be quibbling about the terms.

No win win situation lorr for sure. Bank win, you die.

correction, its Bank Win, you die LATER

Banks are not charity, and like any other profit oriented business, it cannot be making losses or else your money saved within that bank suffers. Think Lehrman Brothers. Unless you are very well of, you are still likely to take bank loans in order to afford that car or that house.

But they always highlighting their so called ‘CSR’ works in television. For marketing purpose or window dressing only?

Only profit driven organisations would do CSR. Banks are no exception. What do you think?

How they get the additional RM822 from?

Hadi said it came from riba.

me too couldn’t get how the RM 822. How about the interest of RM 12,150 ? I’m getting interest of RM 7,781.01 from RM 37,081*3%*7year

Rule 78.

what is rule 78 and how you calculate it?

Menangguk di air yang keruh.

apply moratorium pinjaman kereta.

Bagaimana tidak mahu terlibat dengan moratorium

So if I owe only 10k in my final year of installment with original 100k loan @ 3.5% they will charge me 3.5%x100k =Rm3500 interest?

That will be like 35% interest, ah long level since balance loan is only 10k. Not worth taking unless you are in the first 2-3 years of your hire purchase.

i believe it will be 3.5% of the six months installment x extended duration.

They might be using the principal value for the deferred payment instead of actual repayment and start the calculation from beginning of each month. that’s why the number is weirder than straighforward calculation

JUR1086

Saya nk mohon moratorium

Moratarium kenderaan

What happen to moritorium car department?

I need Moratorium for my car loan because my salary very low

Saya nak tahu bila saya start bayar bulan kereta. Saya ada ambil monitorium yg 6 bulan.