The overnight policy rate (OPR) has remained at 3% ever since it was increased from 2.75% following Bank Negara Malaysia’s (BNM) monetary policy committee (MPC) meeting held on May 3, 2023. Since then, the OPR has stayed at 3% after 12 MPC meetings, but that changed yesterday when the country’s central bank announced that the OPR would be reduced by 25 basis points to 2.75%.

The OPR affects bank loans, as the lower it is set, the less expensive it is to borrow money. With this change, borrowers may be faced with lower financing rates as a result, which makes things like car loans (hire purchase typically) more affordable and potentially easier to gain approval.

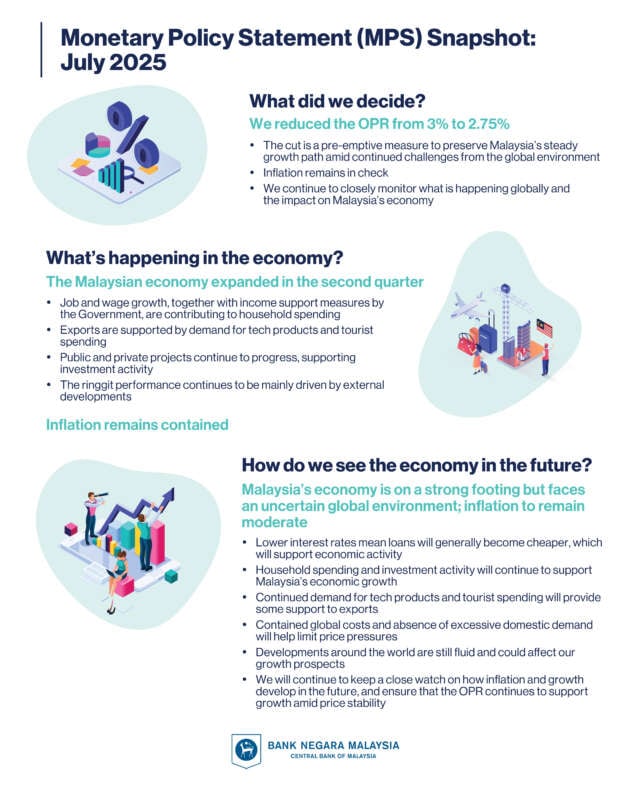

BNM says the cut in the OPR is a preemptive measure to preserve Malaysia’s steady growth path amid continued challenges from the global environment. It added that this outlook is weighed down by uncertainties surrounding tariff developments as well as geopolitical tension, and that inflation remains in check and expected to remain moderate in 2025. The next MPC meeting is set to take place on September 4, with the sixth meeting of the year slated for November 6.

Here is BNM’s full statement:

Monetary Policy Statement July 2025

At its meeting today, the Monetary Policy Committee (MPC) of Bank Negara Malaysia decided to reduce the Overnight Policy Rate (OPR) by 25 basis points to 2.75%. The ceiling and floor rates of the corridor of the OPR are correspondingly reduced to 3% and 2.5% respectively.

The latest indicators point towards continued expansion in global growth, supported by sustained consumer spending and to some extent, front-loading activities. The global growth outlook would remain supported by positive labour market conditions, less restrictive monetary policy and fiscal stimulus. This outlook is weighed down by uncertainties surrounding tariff developments, as well as geopolitical tensions. Such uncertainties could also lead to greater volatility in the global financial markets and commodity prices.

For Malaysia, the latest developments point towards continued growth in economic activity in the second quarter, underpinned by sustained domestic demand and export growth. Moving forward, growth is expected to be supported by resilient domestic demand. Employment and wage growth, particularly within domestic-oriented sectors, as well as income-related policy measures, will support household spending. The expansion in investment activity will be sustained by the progress of multi-year projects in both the private and public sectors, the continued high realisation of approved investments, as well as the ongoing implementation of catalytic initiatives under the national master plans. Favourable trade negotiation outcomes, pro-growth policies in major economies, continued demand for electrical and electronic goods, and robust tourism activity could raise Malaysia’s export prospects. However, the balance of risks to the growth outlook remains tilted to the downside, stemming mainly from a slower global trade, weaker sentiment, as well as lower-than-expected commodity production.

Headline and core inflation averaged 1.4% and 1.9% in the first five months of the year respectively. Overall, inflation in 2025 is expected to remain moderate, amid contained global cost conditions and the absence of excessive domestic demand pressures. Inflationary pressure from global commodity prices is expected to remain limited, contributing to moderate domestic cost conditions. In this environment, the overall impact of the announced and upcoming domestic policy reforms on inflation is expected to be contained.

The ringgit performance will continue to be primarily driven by external factors. Malaysia’s favourable economic prospects and domestic structural reforms, complemented by ongoing initiatives to encourage flows, will continue to provide enduring support to the ringgit.

While the domestic economy is on a strong footing, uncertainties surrounding external developments could affect Malaysia’s growth prospects. The reduction in the OPR is, therefore, a pre-emptive measure aimed at preserving Malaysia’s steady growth path amid moderate inflation prospects. The MPC will continue to remain vigilant to ongoing developments and assess the balance of risks surrounding the outlook for domestic growth and inflation.

Looking to sell your car? Sell it with Carro.

Anwar menang rakyat senang

Too late, tariff inflation ady set in, Chap Fan prices has gone up 20%. Down with PMX!

#TurunAnwar