Motor insurance premiums are set to be based on a list of risk factors when the industry is de-tariffed in 2016, Bank Negara Malaysia (BNM) has said, according to a report by The Sun.

Various risk factors not included in the current motor tariff, such as residence location, vehicle make and model, use of vehicle, occupation of owner, claims history, gender and age will be taken into consideration, similar to the system employed in countries like the UK.

In other words, the insurance premium rates you pay will depend on how much risk you are perceived to carry – for instance, owners of makes and models with high reported theft rates, owners of high-performance vehicles, owners with fewer years of driving experience or those who live in crime-prone areas will have to pay higher premiums.

The central bank told the daily that it is working together with motor insurance players to come up with a de-tariffing roadmap that will see a more risk-based pricing of premiums.

“As motor insurance is a compulsory cover, it is important that the de-tariffication approach does not significantly impact the motoring public and disrupt access to cover,” BNM told The Sun. Simply adjusting premiums in proportion with increasing motor insurance claims is not sustainable in the long term, the central bank added.

Indeed, according to the General Insurance Association of Malaysia (PIAM), in 2013, motor insurers paid out nearly RM1.3 billion in third-party bodily injuries (+12% over 2012), RM295 million in third-party property damage (+28%) and RM627 million in total for motor thefts (+21% over 2012).

That was last year. This year, in the first quarter alone, net claims paid out for bodily injury and property damage due to road accidents amounted to RM1.384 billion. Clearly, all of these contribute huge losses to motor insurers.

As such, the insurance and transport industries, along with motorists and other relevant agencies, should work together to promote safer driving, reduce accident rates and create greater awareness on road safety, BNM told The Sun, pointing out that in doing so, insurance payouts can potentially be minimised, leading eventually to lower premium rates.

In 2011, the central bank announced the New Motor Cover Framework. Under this framework, Malaysia’s motor tariff premiums would be revised gradually beginning January 2012, to eventually culminate in the abolition of tariffs in 2016. Premium rates will then depend entirely on market forces.

Meanwhile, all general insurance products purchased, including motor cover, will be subject to the Goods and Services Tax (GST) from April 1, 2015, BNM told the daily.

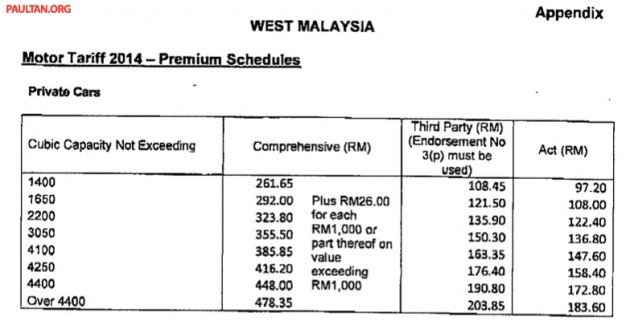

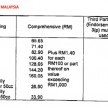

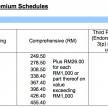

New motor insurance tariffs effective February 15, 2014

Looking to sell your car? Sell it with Carro.

finally…

Yes, buy a Proton then you can smoke this smoke that smoke chicken wings smoke salmon.

You will be smoked by the insurance also soon.

kzm will come here and say that the higher premiums will result in more profit and more taxes paid to our Government. In his pea brain, he will say that the revenue is good for the government because it will solely be used for infrastructure by our Gomen

i support , this is a good idea and in the long term , encourages ppl to drive like humans not like retarded monkeys

this new method of risk based insurance policy is similar to UK motor insurance policy. In UK, the motor insurance policy cost sometime is higher than car price…

oni for high risk people..

What do you think are ‘high risk people’?

For instance, in Germany the 3rd party insurance for a Porsche 911 is actually cheaper than that for a Nissan Micra (Perodua Viva equivalent).

The 911 has less risks for the insurer, as it’s mostly carefully driven by people in their 40s and 50s in good weather conditions only. The Nissan Micra on the other hand is driven by young people who are causing lots of small accidents.

BTW: The theft cover insurance for a 911 is of course much more expensive than that for a Nissan Micra.

Few thousands for a good condition used car at UK but will NEVER happen in bolehland.

eg. 9yrs old used Honda City or Toyota Vios cost RM36k (a new car price w/o tax)

that’s why msia a rising star in asean in transformation towards Used Car Automotive Hub or 2nd Hand Car Automotive Hub.

We msian 1st class citizen mindset willing to pay a new car price but to purchase a imported 10yrs old car either form THAI, INDON, JAPAN, UK, etc.

The actual fact is we are in this mindset that’s the reason we still vote for BN to lead the country.

I hope we follow their method, but not the figures.

Premium will likely jump to the sky solely due to the fact that Malaysia is in high risk of crime anywhere you are.

Nowhere is safe here. Even the diplomat car also ppl dare to steal.

Syukur Malaysia Aman!

true that..and they will have the authority to rate EVERY car as high risk.. Hence the Age Risk Factor will be brought into place..zzz

walauwehhh after this sure many people cheat their own home address, occupation, KM per year use and use of vehicle.

Then when it comes to claim they will be rejected, so not so smart in the long term.

how to fake ur occupation? ur data already inside EPF…

i already did that when im live in uk, all my insurance data is fake to minimized my insurance cost… only real my name and phone number…

Toyota’s so-called high RV will be offset by the high insurance premium once this is enforced. Take this Sam Loo!!!

Then Toyota got to improve on their security. Maybe install GPS tracking and free steering lock for all cars. This will reduce the theft but not prevent, then maybe premium for toyota makes will drop.

Everyone must be responsible for something.

Dream on, toyota here not even willing to give you more safety. WTF makes you think they will upgrade on security? HILUX RV will go down the drain as its the most targeted by thiefs. Too easy to steal. RM10k insurance per year?

Dream dream dream…….

Soon UMW can offer security package upgrade for RM9999 for premium anti theft alarm and immobilizer. Currently Hilux and Camry can be stolen in less than 60 seconds. lol

I agreed with das auto…Toyata on safety and security ? dream on la meh..

Look like toyota will have high insurance premium since not only god car status (accident prone) but also super high wanted list among thief.

I agree. Most toyota drivers here drive like maniacs and crash. Easily crash due to no VSC. Its double whammy for them. RV will be worse than volvo or citroen when its implemented.

The G Should revise the road tax calculations next. Engine capacity alone is not justified!

I honestly cannot fathom why someone gave you a thumbs down

all the G related parties@cronies are enjoying their “shopping” even when the rakyat still can coupe with fuel hike, GST & everything. How the hell are they going to justify all the aspect and come out with the exact figure individually???for those who has been living long enuff in this country sure know how these monkeys work!!!I HATE NAJIB!!!

Why is so hard to think about this…UK already use it long long long time ago! And yet GOV claim M’sia is the best this and this…the hub of this and that…and finally only left paper work only!

Government should impose ESC/VSC & 6 airbags as compulsory for vehicle to be sold locally. Give the manufacturers tax breaks & duties exemption based on safety equipment installed & emission output. Trust me, the number of accidents and bodily injuries will decrease a lot, life insurers also will have less compensation payout, and less emergency accident cases to be handled at hospitals. Why can’t our policy makers think of this simple yet effective solution??? Our insurers claimed they lost billions due to claim payouts, but hides the fact that they net profited a lot more billions.

no everyone can afford on new car, especially fresh grads. and most of accident involved vehicle is old car rather then new car.

This is good.

Hope it increases the competition among insurance companies. The regulatory bodies should also make sure that switching between insurance companies is standardized and simple.

Another thing is to have MyCC monitor any price fixing among insurance companies.

This means that, the young people will not able to pay high premium and most probably need to borrow their parent’s name for insurance.

Got pro and cons.

it doesnt stay long because case will happen again if the driver do not take responsible on road! How many people can help to purchase insurance?

i think this would only bring more problems than solutions

Finally. Risk based insurance is the only fair way to insure cars. Why should I pay the same insurance as a 21 year old rempit that drives a wiralution and has had 4 accidents while I have not had a accident in 15 years. The problem is that rates will rise for bad drivers/young drivers and they will not be able to afford it, leading to uninsured cars on the road.

I agree with what you said. I have a friend who is an idiot driver and he even claim he had total 8 cars during the last 10 years of driving and he seems to be proud of it. This kinda inconsiderate drivers should be penalised with hefty loading.

U say this. Wait a few years when you have to shell out 10k/yr for insurance for your kids.

base on gender?hihi

Give incentives/discounts for those who have car DVRs installed.

This is another form of subsidy. Clean record drivers paying subsidy for careless drivers. And I’ve been paying subsidy for them for 25 years.

10q PIAM. Bunch of retards handling the industry.

its not the insurers fault, insurance tariffs are controlled and set by the Gov. If it was up to the insurers, they would have done this years ago, they arnt stupid

A rich people living in a gated and guarded area will pay less than a poor people…good idea

Kampung area got Rukun Tetangga. So consider safe also.

well, it take time to prove the result as driver do not feel pain if they do not claim or be claim their vehicle insurance. Like Singapore, most of the driver do not wish to involve into claim case, otherwise they will face multiple increment on premium at following years. Until the system found that your record is clean then will adjust back to normal premium.

Woot, all the modified ah beng already crying lol good

Finally our vehicle insurance is going down the correct path. We still got the road tax, petrol subsidy and excise tax/AP issue!

I think this is going to contribute to higher number of uninsured cars on the road. Currently many bikes on the road are uninsured & with cars joining the pact, the law abiding citizen is going to suffer. My brother inlaw’s Lexus was smashed by an uninsured car which ran a red light & driver claimed to be jobless. End up he had to claim own insurance & top up repair cost himself as they did not pay for the full cost.

“THose in crime prone areas” have to pay higher premium> does this make sense in Bolehland?I heard a cop lost his private car while having roti chanai in a mamak shop 5 meters from the Balai.Where do you consider safe and where do you say is crime prone?

Is Bangsar safer than Sentul?

They usually base it on historical data. If a lot of cars have been stolen in the past in a particular area then of course the risk is higher if you insure someone that lives there, so they charge more.

BN cronies area = safe

PR cronies area = extremely unsafe, over 9,000X premium vs BN area. Govt gonna say balasan tak undi BN. PDRM gonna say PR people prone to be seditious, ulama will calm your jimmies say this is all ketentuan Tuhan, syukurlah negara aman.

Good opportunities for the insurance companies to jack up their revenues and profits

All I see are $$$.

Rates are going to go up for people that can ill afford it. Namely;

1) live in a not so safe area

Sorry if u live in a flat and park on the street

2) drive an old car

Too bad if you cant afford a new car. Right now we have 100% loading on old cars already. Expect worst.

The only silver lining is seeing high insurance

premium slapped on new cars with little or no safety gear. A car with vs and a car full of airbags would be inherently safer and minimizes claims when the occupants are less injured.

Thinking of buying a new car? Better think carefully. You are going to keep your car for at least 5-10 years… hope you don’t get one in a high risk group.

Good direction but need to double check on some existing problem and future problem.

If it was a case of hit and run or accident where the wrong party is gone and we proceed with the claim,it wont be fair to us if we are force to pay higher premium next year.The database must be comprehensive instead of a yes and no column on previous claim.

some existing issue is to improve the time needed for claim settlement.Insurance provider are just lame enough to only employ adjuster at some state.People at other state have to wait and wait for the adjuster.

If BNM willing to implement this,it should also look on the education side.The people need to be educated on what is their right on the policy and what to do when there is an accident.

Also,dont let the insurance company run riot on the people’s pocket.

I am expecting a lower premium for my 12yrs old Waja and 14 yrs old Pajero.I mention ‘expecting’ because knowing this is Malaysia and anything can happen.In the end the insurance compamy ould demand higher premium than before by saying my car is old and prone to accident compared to a new basic spec myvi or axia…heh…

Guys, don’t be too happy. Our gov will find ways to con us. They will give us less (ciput) and take away more from us. I’m eager to wait for more moronic political statements from one of the ministers to kill all these excitements. Die, die, die….

Umno bn people never think the rakyat they only idear is how to make their own pocket full of money taken from the rakyat. Thats why we must change the goverment to pakatan rakyat at least our cost of living will change to a harmony way of life with all races.

Brilliant. Open market will force-reduce all unnecessary claims, reducing the premiums for normal people. One thing I’d like to see though is people buying less safe cars are penalized.

Since there’s already aseancap, they can set up insurance groups based on ncap star ratings. I think its the quickest way to educate Malaysians to buy safer cars, if you are literally penalized financially for buying a less safe car.

If premiums are risk based, then Korean Car owners will be charged 10X the amount compared with Jap cars.

Otherwise, these hailat face fellas will just crash their cars instead of selling them to me

I agree with this. Our tariff rate has been around for far too long (20+ years?). The way i see it, it will promote healthy competition between insurance companies. And unfortunately (or fortunately) smaller players (local insurance companies) will get eaten alive by giants.

Was sharing this to my friends parents yesterday and they said this would instead promote more hit and run….. to avoid claiming and paying more for car insurance…. somehow… i hope this will be in the minds of Malaysian drivers…

stewpeed system…

just an excuse for the insurance company to earn more from people. also young drivers will be charged more which is NOT FAIR, sports cars will be charged more, NOT FAIR, once u make a claim you will be charged double NOT FAIR… just give the insurance company an excuse to charge more. what will happen is many young drivers will buy the insurance using their father s name just to pay less.

the system now is more fair because the insurance is based on the car price regardless. u buy a more expensive car, u pay more for insurance cos the cost of the part and repairs are more.

its very fair. Theres no reason a 18 year old in a 250k 250bhp Golf GTI should pay the same insurance as a 40 year old in a 250k BMW320i. If i choose to buy a safe, non flashy car, why should i pay the same insurance as a 18 year old driving a hot, flashy , powerful, car?

conclusion : we will pay more. period.