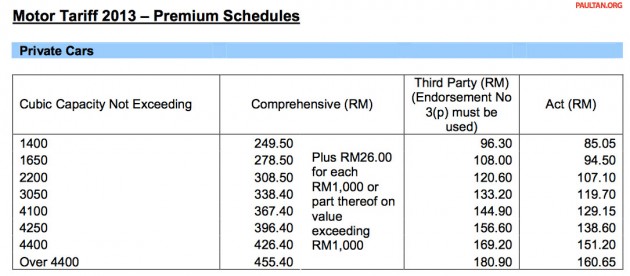

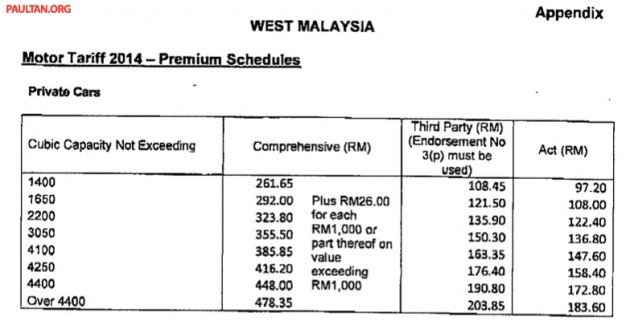

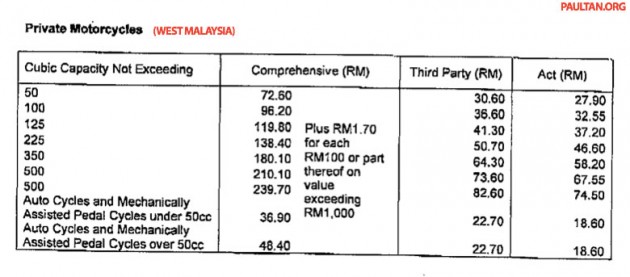

Motor insurance rates have been revised upwards yearly since 2012, and the latest revision to the rates are set to come into effect February 15, 2014.

The second table from top lists the new rates, which are an increase of about the same range as the previous adjustment made on February 15, 2013, which is listed in the top-most table.

These yearly increases will continue until the planned detariffing of motor insurance premiums in 2016, when premium rates will be further differentiated in accordance to the individual risk profile of vehicles, owners, as well as potential pricing differences between insurers.

When the detariffing comes into effect, we might see the emergence of ‘full service’ insurers with higher rates but more perks such as complimentary tow truck service, as well as ‘budget no frills’ insurers.

Looking to sell your car? Sell it with Carro.

AI-generated Summary ✨

Comments discuss various factors influencing motor insurance rates, including age, gender, location, vehicle type, and No Claims Bonus, highlighting that premiums vary based on individual circumstances. Many express frustration over the recent tariff increases from February 15, 2014, blaming rising car prices, inflation, and economic policies, with some critics accusing insurance companies and authorities of corruption and overcharging. Several comments mention the impact of higher premiums on ordinary Malaysians, especially those with lower incomes or older vehicles, and lament the lack of government intervention or regulation. Opinions also reflect general dissatisfaction with government policies, economic conditions, and inflation, linking them to increased living costs across multiple sectors. Overall, sentiments are predominantly negative, criticizing the rising insurance tariffs and broader economic management.