Toyota Capital Malaysia, a subsidiary company of Toyota Financial Services Corporation (TFSC), has launched a website detailing three new car financing schemes for prospective Toyota owners. Depending on your preference or financial situation, you can choose from the Toyota EZ Beli plan, Toyota Flexi plan or Toyota Drive, the last being an Islamic leasing plan.

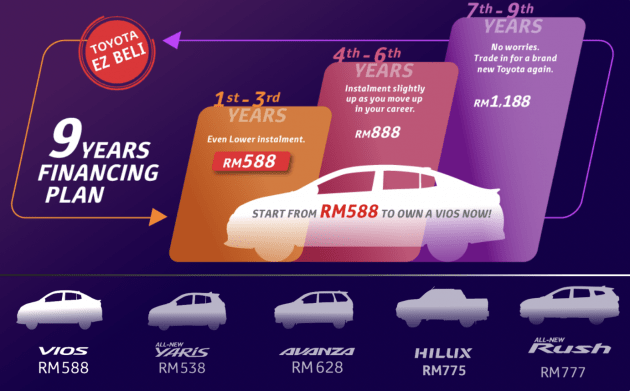

Let’s start with the EZ Beli plan, which will arguably be the most popular choice for car buyers. Basically, it’s like a conventional hire purchase loan, but staggered into three tiers. The loan tenure is fixed at nine years, but monthly instalments for the first three years (36 months) is the lowest.

For example, under the three-tier EZ Beli plan, an entry-level Vios 1.5J (AT) – which costs RM69,400 – can be had from RM588 a month (based on the maximum 90% loan rate). This sum is fixed for the first three years. For Tier Two, which is from year four to six (also 36 months), the instalment goes up to RM888 a month, and in Tier Three (year seven to nine), it’s RM1,188 a month.

At the end of the second tier, customers get the option of trading in the car and upgrading via EZ Beli once more. If you’re not inclined to service the higher instalments in Tier Three, then you can trade in your car for a new model, because the trade-in value of said car can be used to offset the outstanding balance of the loan.

According to Toyota Capital Malaysia, other instalment plans may be closer to RM800 a month for the Vios. What the EZ Beli plan does is lower the entry point for aspiring owners, before the repayments increase in anticipation of the customer’s career progression. Like regular car loans, the maximum loan for EZ Beli is 90% of the car’s retail price, including insurance and road tax.

Of course, you get the option of paying more at any point of ownership, and the additional payment will be considered as advance payment. However, keep in mind that not all Toyota models are available via the EZ Beli plan.

The Flexi Plan, on the other hand, is applicable for all Toyota models on sale today. It’s a plan that lets you adjust monthly payments or tenure when the Base Lending Rate (BLR) changes. For example, if you pay a little extra on months when you can afford it, the compounded effect means you get to settle your loan earlier and save on accrued interest.

Let’s say you’ve decided on the new Corolla Altis, with a loan amount of RM123,100 that you wish to service over nine years. Based on a BLR of 6.75% (this is variable), the fixed monthly repayment is RM1,472. By paying just RM50 more (RM1,522) every month, your loan term is reduced by four months, and the savings on interest is RM1,642. If you pay RM3,000 annually (or RM250 extra each month), the loan duration is shortened by 18 months, and the interest saved is RM6,185.

Another benefit of the Flexi Plan is the choice to switch to conventional, fixed-rate hire purchase financing at any point, for free. Those on the Flexi Plan must remember that a 2% interest rate will be imposed for late payments, which is compounded over the contracted BLR. Also, if at any point the BLR climbs or falls, the agreed spread (monthly repayments) will not change.

Lastly, there’s the Toyota Drive plan. This is essentially an Islamic leasing programme (based on the Sharia banking principles) with zero downpayment (terms apply), and you won’t have to worry about choosing an insurance panel or deal with annual road tax renewal. All of those will be arranged by Toyota Capital Malaysia, plus the renewed road tax will be mailed to your residence for free.

Under this plan, the leasee is covered with Guaranteed Auto Protection (GAP; at no extra charge), which prevents customers from having to pay the difference between the insurance settlement amount (based on the car’s market value) and the outstanding amount to settle in the event of a total loss. If insurance proceeds exceed the settlement amount, customers are entitled to a refund (conditions apply).

Also, Toyota Capital will determine the lease-end value of the vehicle at the point of purchase, so customers won’t be affected by depreciation or fluctuating market prices. At the end of the lease, you get to choose whether to trade in the car for a new Toyota model, return or purchase the existing car (subjected to the guaranteed Lease End Value) at the end of your lease period.

However, at this point, there isn’t a breakdown on available models for lease, nor pricing structure. For more information regarding the three new financing plans, click here to visit Toyota Capital Malaysia’s new website. So, what do you think?

Looking to sell your car? Sell it with Carro.

Toyota Yaris Cross

from RM99,900

Toyota Yaris Cross

from RM99,900  Toyota Hilux

from RM226,300

Toyota Hilux

from RM226,300  Toyota Urban Cruiser

from RM198,000

Toyota Urban Cruiser

from RM198,000  Toyota bZ4X

from RM220,000

Toyota bZ4X

from RM220,000  Toyota GR Yaris

from RM315,600

Toyota GR Yaris

from RM315,600  Toyota GR Corolla

from RM368,950

Toyota GR Corolla

from RM368,950  Toyota Camry

from RM221,800

Toyota Camry

from RM221,800  Toyota Corolla Cross

from RM133,800

Toyota Corolla Cross

from RM133,800  Toyota Hiace

from RM169,000

Toyota Hiace

from RM169,000

Hidden due to lowcomment rating. Click here to see.

But now, toyota won’t desperate for now. UMW are concentrating on safety features, reliable and quality in order to ensure that consumers to save lives. Even now, you can see so many people are also buying p1 & mazda with more safety, instead of using honda. Right now, honda is not doing very good job by not solving problems about quality, under specced safety features and reliable.

Honda are so desperate and so greedy now because customer service are not friendly, Honda CVT also utterly expensive, quality got problems too and SC always never improve yet still want to sell more honda cars with poor safety to the consumers with discounts promotions and always concentrating on their honda profits.

Yup. These fanbois used to laugh at Proton for providing easy n flexi financing but now? Toyota have to jilat everything. Wahahahaha

three affordable car financing schemes… No use UMW, we are more care about the quality and the car price.. As long following the global standard and price, everybody happy.

Let us ask a simple question: If u dont have a plan B or C,are you going to plunge into a new round of 9 year hire purchase loan,just to satisfy the new car itch?

Now,musang king exporters are also having a hard time,cos of falling demand from China.Tourism ,airlines are facing serious cutbacks due to the virus.

So,ask yourself..DO U NEED TO BUY A NEW CAR?

The buying of cars as if tomorrow never comes,has ended.

UMW can afford to make less money.But u cant afford to make a mistake without a Plan B.

Well, toyota improves quality than honda.

Wow, amazed

Kudos to Toyota. Now everyone, can Toyota…

fresh grad rejoice. now can show off orang kampung they ‘made it’

The EZ Beli sounds very interesting. Make it available for the Corolla than you’ll see Corolla everywhere in the street.

Freaking high average annual interest for the Vios over 9 years, higher than used car interest rates.

what about vellfire?

This is a never ending debt pit created by Toyota for our new generation! Irresponsible. You have to pay dearly RM1.2k for 8 years old scrap? BNM, are you just looking at this? Meanwhile the trend today actually the youth prefer using Grab instead of owning a car. Ask Chef Wan.

Conventional fix rate would still work out cheaper in long run.

The interest payment for the plans above is way higher than conventional fix rate. It’s only good for those people who can’t get fix rate loans with banks, which begs the question, if you can’t afford it in the first place, why get yourself into a situation where you can get into serious financial trouble?

A creative way to make the car look more affordable.

Sounds like a win win say a myvi salary band guy could now drive a toyota! Car manufacturer sell more, this will fuel our economy!

On the flip side, the commitment get snowballed for an aging car. Buyers will get into trouble if their salary do not grow as fast as their commitment. It is a good way to motivate the buyers to make money if i try to think of this positively.

I think there is an error, AiTAB offer up 90% finance only Toyota Drive which is shariah base offer zero downpayment (terms apply)

That’s a huge cut from banks income stream. First Merc, now Toyota. Well as long as things are cheaper…

Does it include T&C like have to do service on time? as Toyota has high tendency to forfeit customer’s warranty coverage.

Creative ways to make people part with their money. Some of these people cannot afford the monthly payments and should be buying cheaper cars to begin with.

Yes you might criticize UMW for this, but many other car companies are doing the same.

EZBeli = SusahBayar?

If follow example above, total 9 years payout is RM95,904.

If take Public Bank car loan rate today, monthly installment is rm750 X 108 months = RM81,000.

Wow… do the maths… you are paying rm15k extra to Toyota over 9 years. And bear in mind, they also make tons of money selling car to you.

But then, u get the option to trade in the car for a new one with a new EZBeli plan (start from tier 1). Two tiers before trade in would total up to RM53,136 for the Vios. Sounds like a good bargain considering you could upgrade to the latest car after 6 years and start the programme all over again. However, you’ll be in a never ending loan for life if you want to play that game

every home should have at least one Toyota!!

Time is bad. Can’t blame Toyota. Those foreign brand exploiting and benefiting from protectionism have no right to condemn.

Yeah, we should instead condemn those talibaruters that are working with these foreign brands to exploit and benefit from us, more so when times are bad.

So basically the Toyota Drive Plan is actually a lease hire program? Come on lah. Don’t BS like we know nothing.

And the 3 tier program reminds me of similar plan by Naza some 15 years ago. For its Spectra and Citra

What will happen if we sell the car before tier 2 or tier 1. Haha…