In an announcement by Bank Negara Malaysia (BNM), hire purchase loans and fixed-rate Islamic financing will come with additional interest charges after the six-month moratorium that is effective from April 1 to September 30 this year. In short, if you choose to take up the six-months payment pause, it won’t be interest free, and you’ll have to pay the interest later.

So there are two ways to go about it, according to the Association of Banks in Malaysia (ABM). One is when the half year moratorium ends, you pay the accumulated six months of instalments together with the seventh month instalment. Choose to do this and no extra interest will be charged, although we can imagine that not many will be able to cough out the big lump sum.

The second option – if you choose to take the moratorium offer (remember, you don’t have to) – will see the interest charged on that six-month pause spread out throughout the loan tenure. So you’ll have to pay slightly more than your usual monthly instalment from October 2020 onwards (more on this later). The loan tenure will also be extended for six months, six months because that’s how long “time was paused” for you.

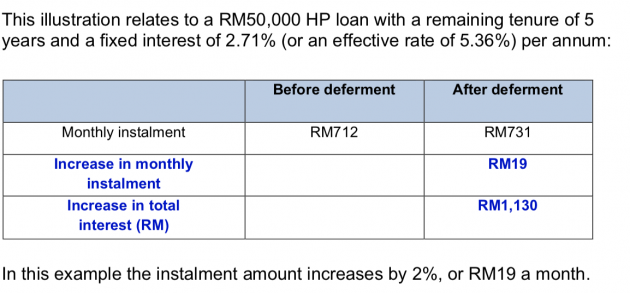

It sounds a lot worse than it actually is, and BNM has given a simplified example above. It says that for a hire purchase loan of RM50,000 with a remaining tenure of five years and a fixed interest of 2.71% (or an effective rate of 5.36%) per annum, the monthly instalment will go up from RM712 before the deferment, to RM731 after deferment, or October 2020 onwards.

This works out to an extra RM19 per month, or a total of RM1,140 over the full tenure (yes, it is that and not what is on the BNM FAQ panel – sure, it could be RM18.83, but you’d think as a bank, someone would get that spot on or round it to RM18.80). BNM also states that for this example, the instalment amount increases by 2%. If we’re counting, however, that works out to an increase of 2.67%, but hey, 2% sounds easier to swallow right?

Exact figures for your own car loans will vary, of course, depending on your monthly instalment, remaining tenure and interest rate (though the rate that is more important here is the effective rate, sometimes referred to as the Annual Percentage Rate or APR, which is not as straightforward). The longer your remaining tenure is, the more you’ll have to pay (as the banks will get the money owed that much later), but the monthly hit will be relatively small, as shown above.

UPDATE 2:The central bank continues to add to its FAQ. With regards to the HP issue, it appended this “additional guidance” in its latest revision (see panel immediately below the update):

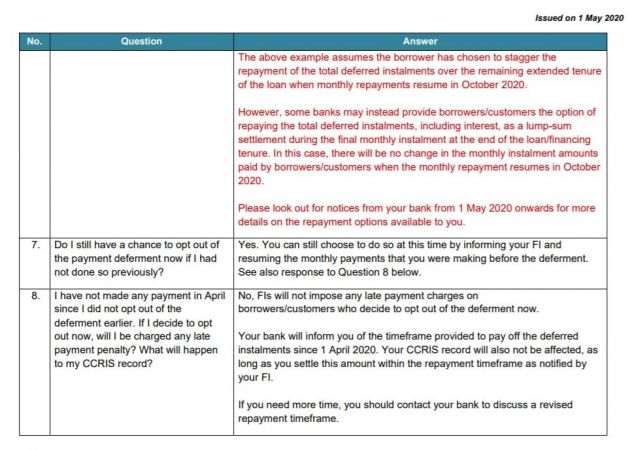

“The above example assumes the borrower has chosen to stagger the repayment of the total deferred instalments over the remaining extended tenure of the loan when monthly repayments resume in October 2020.”

“However, some banks may instead provide borrowers/customers the option of repaying the total deferred instalments, including interest, as a lump-sum settlement during the final monthly instalment at the end of the loan/financing tenure. In this case, there will be no change in the monthly instalment amounts paid by borrowers/customers when the monthly repayment resumes in October 2020.”

The first part is simple enough, as detailed earlier above and a six month extension to the loan period, which is how long “time was paused” for you. The second incurs a huge payment in the final month of the loan repayment, because you will have to pay the final instalment plus the deferred six months instalments, along with interest, at one go. In simple maths, that’s seven months instalment plus interest over the period, one shot.

It is also worth noting that this option will see interest being accrued on the remaining and unpaid deferred instalments, so it could add up to more than the earlier option. You will want to check the terms and conditions as well as repayment options that are provided with any agreements or notices from your bank.

It was previously assumed that those who chose to take up the moratorium would not be charged additional interest on their deferred payments, seeing how hire purchase loans and Islamic financing plans follow a fixed-rate basis, where interest charges are calculated upfront, but this is an unprecedented situation and is not the case.

UPDATE: The original view – and our report on this – that those who chose to take up the moratorium would not be charged additional interest on their deferred payments was correct, as the BNM FAQ on March 27 indicates – there would be no additional interest charged on HP loans.

This mention regarding HP loans was subsequently dropped in the amended FAQ on April 21, and mention of interest being charged emerged, leading to the current developments detailed for May 1. We have included images of the BNM FAQ as reference (see below).

In an official release, the central bank directed banks to inform borrowers/customers on any changes to the terms of their agreements should they choose to take up the moratorium, including the revised payment schedule and any changes to payment amounts – the latter includes those arising from normal interest/profit rate accrued during the moratorium, which is the fresh bit.

For individuals who no longer wish to take up the moratorium, they can can still choose to do so at this time by informing their respective banks and continuing with their scheduled payments based on the terms of their existing agreements.

In this scenario, they will be given “reasonable time” by banks to meet any outstanding scheduled payments that were earlier deferred under the moratorium, which would technically be for the month of April 2020 when the moratorium period began. Banks will not impose overdue or late payment charges on these payments until they are due based on the revised payment schedule agreed with borrowers/customers.

The directive issued by BNM is to to ensure borrowers/customers with hire purchase loans and fixed-rate Islamic financing are provided with all necessary information in relation to the six-month moratorium that was previously announced on March 25, 2020.

This is to ensure compliance with the procedural requirements under the Hire Purchase Act 1967 and Shariah requirements, which are applicable to any changes that are made to the terms of these agreements, including changes to the payment schedules and/or amounts as a result of the moratorium that is effective from April 1 to September 30 this year.

This process will begin from May 1, 2020, where banks will need to notify borrowers/customers with these financing plans via SMS, email or registered mail on the necessary steps that they need to take to complete the process of deferring their loan/financing payments under the moratorium.

What do you think of this latest development? Is it a fair move by banks? On the flip side, we can’t expect banks to fully absorb everything during the moratorium period, although the sudden decision may catch many by surprise given the earlier stand detailed by BNM. Let us know your thoughts in the comments below.

Looking to sell your car? Sell it with Carro.

AI-generated Summary ✨

Comments express disappointment and frustration over the U-turn on interest charges during the moratorium period, with many believing banks are unfairly adding interest on deferred payments, effectively extending loan tenures and increasing costs. Some see this as a betrayal of the original government promise, while others blame banks and regulatory bodies for prioritizing profits over consumers' hardship. Overall, sentiments are negative, highlighting feelings of betrayal, perceived greed, and dissatisfaction with the government's and banks' handling of the relief measures.