The National Automotive Policy (NAP 2014) that was announced yesterday evening is a hot topic and the subject of much debate amongst industry players and consumers. Its aims include making Malaysia an Energy-Efficient Vehicle (EEV) production hub for the region, liberalising the local car market to create one that is more competitive and sustainable, as well as promoting local value-added activities and exports.

To that end, a fair number of strategies have been outlined. Most are mid- to long-term; few go into any significant depth. Still, let’s sit back, consider the main points and discuss the probability of their effectiveness (or otherwise) in dealing with the challenging future of the nation’s automotive landscape.

Energy-Efficient Vehicles (EEV) and “customised incentives”

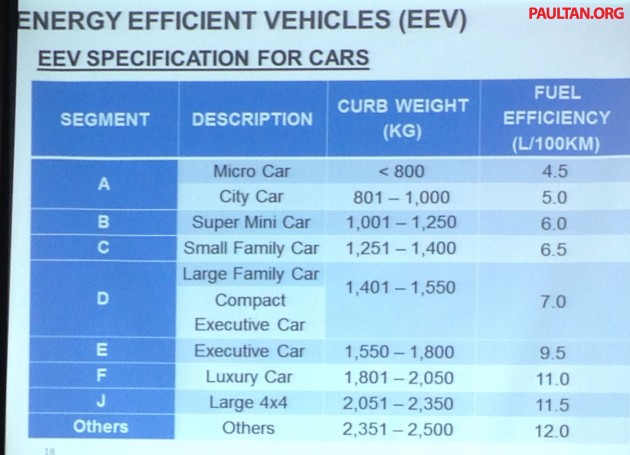

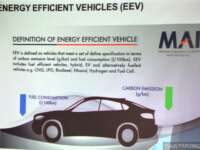

Central to many of NAP 2014’s points is the official introduction and definition of the EEV, which grants carmakers that manufacture them locally “customised incentives.” The EEV classification takes effect immediately.

Regardless of the technologies or method of propulsion used (be it petrol, diesel, hybrid or electric), a car can be classified as an EEV if it meets or performs better than a set fuel economy figure (measured according to the UN ECE R101 standard and expressed in litres per 100 km) for its kerb weight (expressed in kg). For two-wheelers, kerb weight is substituted by engine size.

All well and good, but who will test the fuel consumption of these vehicles? Malaysia does not currently have any certified facilities for this purpose. MITI says such facilities can be privately set up, creating business opportunities, but clearly this will take time, leaving an indeterminate interim period of uncomfortable uncertainty for carmakers. And how does one go about getting economy-testing certification?

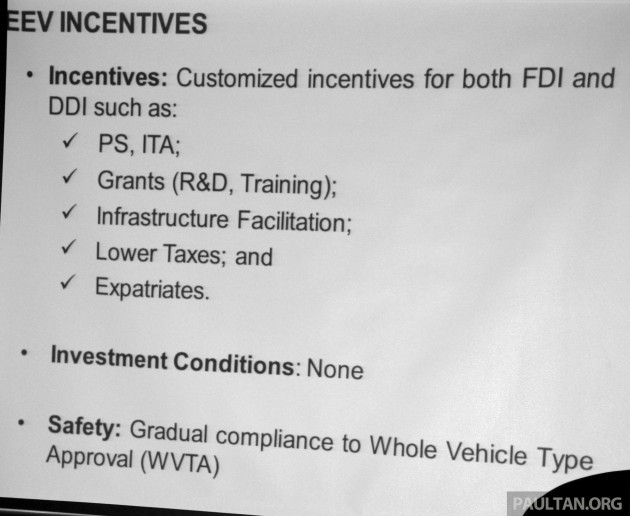

Then there’s the business of “customised incentives.” They come in the form of Pioneer Status, Investment Tax Allowance (ITA), grants, infrastructure facilitation, lower taxes and expatriates, all accomplished without any investment conditions. But exactly how much localisation or value-added activities will a carmaker have to carry out, and how much will there be in terms of incentives? Your guess is as good as ours for now.

The lack of transparency in this matter is of concern to industry players. The last two NAPs were relatively more clear in terms of explaining what kind of incentives were going to be given.

In a pre-announcement briefing with the media last week, MAI CEO Madani Sahari explained that despite the incentives being “customised,” players that were serious on making an investment in the country had no issues with approaching them for discussion. That would imply that a lot of the dissent would be from players that are not really interested, but just want to comment.

At first glance it sounds a lot like how B2B sales is normally carried out – talk to your account manager and depending on your relationship and how well you bargain, you might end up getting a better deal. But is this really how a government should be approaching its policies?

This “customisation” is nothing new really. Even though the last two NAPs specified clearly what kind of hybrid vehicle are able to obtain exemptions, BMW Malaysia successfully got a partial exemption for its ActiveHybrid range of cars, which have 3.0 litre capacity engines. This was certainly not part of the NAP at that time, which stipulated duty exemptions for cars with hybrid engines of less than 2,000 cc in capacity. That’s ‘customisation’ right there.

There’s also the Nissan Serena S-Hybrid, which is not really a hybrid at all, but essentially an MPV with a regular combustion engine with a beefed up alternator and additional power storage. That is just stretching the meaning of ‘hybrid’.

Comparison with Thailand’s Eco Car programme

Our northern neighbours’ Eco Car programme has conditions that are more specifically and rigidly laid out – Phase 2’s requirements include a fuel economy under 4.3 litres per 100 km, CO2 emissions under 100 grams per km, engines displacing 1.3 litres and under (petrol) or 1.5 litres and under (diesel), plus Euro 5, R94 and R95 compliance.

Also, a minimum investment of 6.5 billion baht (RM658 million) and a minimum production of 100,000 units per year are required. The excise duty incentive given is 14% (normal 30%), and if the engine is E85-compatible, 12%.

Our EEV classification is more liberal. Incentives given do not depend on engine capacity or propulsion method, so even vehicles that return a fuel economy of up to 12 litres per 100 km can be granted EEV status (providing they weigh between 2,351 and 2,500 kg, in this particular case). No minimum investment or minimum annual production required, either.

But we know the Eco Car programme’s incentive amounts, expressed as percentages, so there can be no dispute. Because the incentive amounts have not (yet?) been revealed for our EEV programme, we don’t exactly know how much carmakers will get.

Comparison with Indonesia’s Low-Cost Green Car programme

For Indonesia’s Low-Cost Green Car (LCGC), fuel economy on the New European Driving Cycle must be 20 km per litre and up. Petrols must displace between 1.0 and 1.2 litres while diesels must displace between 1.0 and 1.5 litres.

Then there’s price – excluding ownership transfer fees, vehicle tax and local tax, the car must not be priced above 95 million rupiah (RM26,300). Once a vehicle satisfies all of the above criteria, it is granted LCGC status and is tax-free.

No Euro standard or safety regulation is mentioned, but a Low-Carbon Emission Project (LCEP) enhances the programme to include all propulsion methods, without any price conditions or limits to engine size. The tax reductions under LCEP are 25% for 20-28 km per litre vehicles and 50% for 28 km per litre and up. Electric vehicles are tax-free.

To sum up, if a vehicle is a 1.0-1.2 litre petrol or a 1.0-1.5 litre diesel, costs under 95 million rupiah and can return 20 km per litre or better, it is an LCGC and tax-free. If the vehicle’s engine is any bigger than those limits, it then relies on LCEP for tax breaks (providing it can still return a minimum of 20 km per litre).

Again, the incentive amounts here are made known.

Excise duties and the Car Price Reduction Framework

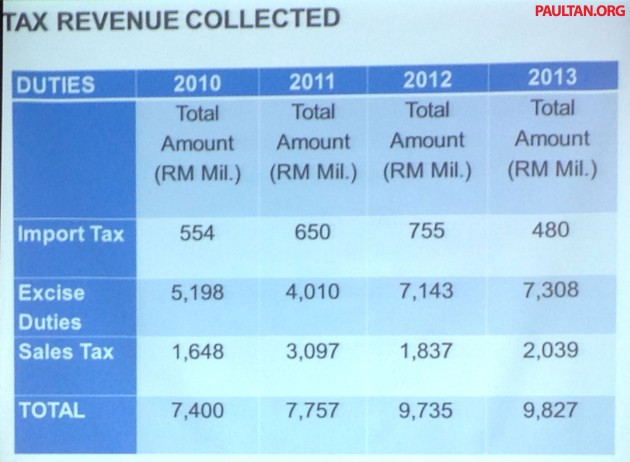

Under the CPR Framework, MITI says car prices will gradually go down in the next five years, culminating in a total price reduction of between 20-30% by 2017. This will not happen through cutting or abolishing excise duties (which provided the government with RM7.3 billion in revenue last year) – at least not for now – but rather, through increased competition brought about by the liberalisation of the industry, which could also see more OEMs entering the market.

We can see where they’re coming from, but if the incentives awarded (which could result in lower car prices for the consumer, albeit indirectly) are going to be “customised,” the probability of an uneven playing field emerging is higher, which could put off prospective OEMs as well as upset a few existing ones. If the details of the incentives given were made transparent and clear-cut, this will go a long way towards boosting competitiveness and true liberalisation.

Approved Permits – status quo for now

Open APs are responsible for Malaysian roads being flooded by grey import cars from right-hand drive countries like the UK and Japan. It doesn’t really affect the majority of the Malaysian public who buy cars under the price of RM100k. These Open APs are used to bring in cars like the Toyota Estima and the Toyota Alphard which are purchased by the upper middle-class.

However, it does affect industry players in a way that it hinders market share and investment by the luxury segment. You cannot ignore the luxury segment as in the end the players have CKD operations and they employ Malaysians in the entire chain of operations, from assembly to sales and marketing, to aftersales.

This is because there is a massive number of grey import Audi, BMW and Mercedes-Benz being brought in through Open APs. These models are the same models that are being sold by the principal companies here in Malaysia, who have invested in the homologation process as well as built a support network for these cars. It wasn’t always this way. It used to be that Open APs were only able to be used for the import of models that were not assigned to Franchise AP holders, but this restriction was removed in 2007.

You may think the 3% of TIV limitation is an adequate safeguard. However, measuring it against total TIV is misleading – the TIV for 2013 was 652,000 units. Three percent of that is 19,560. But think about it. BMW Malaysia sold about 7,000 BMWs in 2013, while Mercedes-Benz Malaysia sold 5,809 cars. That’s already about 13,000 cars from these two brands alone, which make up a huge chunk of the luxury segment. If you include Audi and Lexus, estimated at about 2,000 units each, as well Infiniti and the other brands, in the final reckoning the total numbers would be close.

It’d be obvious to state that Open APs are depriving luxury brands of potential market share, and its continuance will be something that will discourage further investment in the country.

Voluntary Vehicle Inspection

There was no mention of the Vehicle End-of-Life policy in NAP 2014, but a Voluntary Vehicle Inspection (VVI) is being proposed. This will involve cars over five years old, in a bid to keep vehicle roadworthiness in check nationwide and improve road safety.

Inspection centres will not be limited to any one agency or company like Puspakom, but we don’t know how many companies will be appointed or the procedures for certification.

Voluntary though they might be, the inspections will, of course, not be complimentary. Some kind of incentive would therefore be given – the word on the wire is some kind of road tax rebate, if your car passes the inspection.

The UK’s MOT system checks vehicles over three years old for lighting, steering, brakes, tyres, seat belts, body structure, exhaust, fuel and emissions. It is mandatory. An MOT certificate lasts a year, after which the vehicle needs to be retested. Without a valid MOT certificate, the vehicle is not UK road-legal.

An ASEAN equivalent is Thailand’s TorRorOr document. Cars older than seven years and motorcycles older than five years have to pass an annual safety inspection in order to be issued with this document, without which the annual tax sticker cannot be renewed.

We’re not quite there yet, but the VVI, if carefully planned and implemented, represents a step in the right direction towards a safer and more mature auto environment.

AI-generated Summary ✨

Comments express disappointment and skepticism over NAP 2014, claiming it lacks concrete policies, transparency, and genuinely lowering car prices. Many feel it benefits cronies and Proton, not consumers, with accusations of protectionism, inflated car costs, and delayed or superficial reforms. Some see it as political propaganda, comparing Malaysia's high prices unfavorably with other countries, and call for government accountability and alternative solutions like voting out incumbents. The overall sentiment is frustration with unfulfilled promises and a call for genuine change.