Finance minister Tengku Datuk Seri Zafrul Abdul Aziz has waded into the issue regarding banks charging interest on paused hire purchase (HP) loan payments (or profit from fixed-rate Islamic financing) in the government announced six-month moratorium to ease financial burden and improve cashflow in these difficult times.

Before we go into what the former top banker turned cabinet member said on his Facebook page, here’s a recap on the issue. This week, it was announced that HP loans (we’ll use the term to cover fixed-rate Islamic financing as well) will come with additional interest charges after the six-month moratorium effective from April 1 to September 30.

Basically, if you choose to take up the half-year payment pause, it won’t be interest free, and you’ll have to pay back the interest later. The confusion, and anger for some, is that many expected the six-month payment moratorium to incur no interest, just a pause and nothing else.

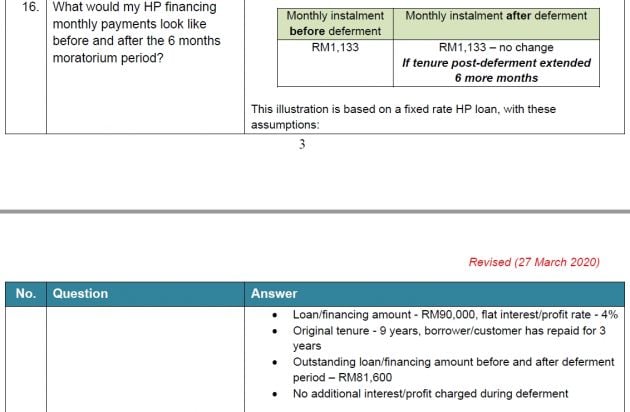

A Bank Negara Malaysia (BNM) FAQ released on March 27 indicated that there would be no additional interest charged on HP loans. This mention regarding HP loans was subsequently dropped in an amended FAQ dated April 21, and mention of interest being charged emerged. Refer to the screenshots to compare.

Basically, there will no free lunch now, so to speak, but Tengku Zafrul is requesting the banks to consider abolishing the accrued interest for HP loans for the six months.

“Lately, there has been confusion regarding the interest or profit rate charged during the six-month moratorium scheme offered by banks. Among the causes of this confusion are various sources that delivered inaccurate information. With that, BNM on May 1 published an FAQ document that has been updated. BNM has also conducted a press conference to clarify the confusion faced by borrowers,” he said today on his Facebook page, translated into English here.

“For your information, there are indeed banks that offered loan moratoriums without charging accrued interest or compounded interest. However, it does not cover all loan products. Also, every bank has its own approach regarding charging interest in the moratorium period.

“Taking into account that there’s a possibility for it to be implemented, and after considering the rakyat’s request, I would like to suggest that all financial institutions, especially those involved in the moratorium, consider abolishing the accrued interest (for HP loans) or profit (for fixed-rate Islamic financing) for the six-month moratorium period,” he added.

The minister acknowledged that this matter is under the purview of BNM, but said that the finance ministry has started proactive steps to find a solution for the issue via discussions with BNM and the banks, to find the best solution for the people.

“We at the finance ministry are ready to work together with BNM and the banking sector to ensure the implementation of this call. The government is always sensitive towards the needs of the rakyat, especially those from the B40 and M40, and is taking this matter seriously. In such a challenging economic situation caused by the Covid-19 pandemic, I hope that this view will be given fair consideration by BNM and the financial institutions.

“I am confident that this move will bring positive impact to the rakyat,” he ended.

Yesterday, BNM released a statement acknowledging the public’s confusion. “We sincerely regret any confusion and anxiety that this announcement may have caused. The deferment of loan repayments is meant to ease cash flows for borrowers/customers affected by the Covid-19 pandemic. This intent remains the same. The confusion arises because of the misperception that the repayment amounts for a HP loan cannot be changed,” BNM said.

The central bank added that the misperception came about due to an illustration provided in an initial version of its FAQ, “where certain assumptions and caveats were made.” BNM said that it had later removed the illustration when the banks provided their own.

Earlier, we’ve also seen a few banks confirm these “assumptions” of monthly instalments staying the same after the moratorium period, in both their own FAQs and official responses to customer queries. We were among those who reported this original scenario, based directly on the information available, which – at the time – was accurate.

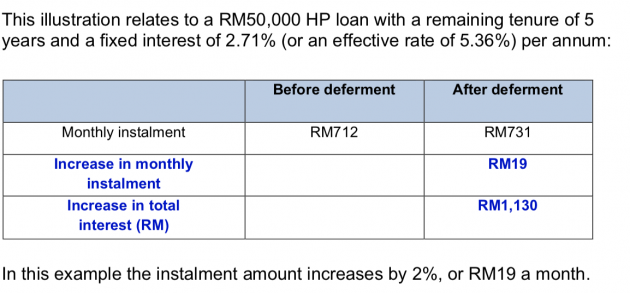

Yesterday, BNM also released an example of a RM50,000 HP loan with a remaining tenure of five years, on a fixed interest of 2.71% per annum. The original monthly instalment was RM712. Should the borrower opt for the payment pause, the monthly instalment will be RM731 in October once the moratorium ends. This is an increase of 2%, or RM19 a month.

Read what BNM said and the latest official status on the issue here.

Looking to sell your car? Sell it with Carro.

AI-generated Summary ✨

Comments express frustration over the government's announced 6-month moratorium on interest charges, highlighting communication issues and the banks' financial resilience. Many believe banks will benefit from ongoing interest collection, especially on housing loans, and will not suffer losses. Some see the government and BNM as ineffective or overly influenced by banks, with concerns about fairness and economic impacts. Overall, there's skepticism about the sincerity of the government's promises and a call for more coordinated and ethical financial aid.