On March 25, Bank Negara Malaysia (BNM) issued a directive to all banks to grant an automatic six-month moratorium (deferment) of all loan/financing repayments effective from April 1, to September 30, 2020. Here’s a simple explanation of how the payment holiday works, from an auto perspective.

UPDATE: On April 30, BNM issued an announcement stating that hire purchase loans and fixed-rate Islamic financing will come with additional interest charges after the six-month moratorium that is effective from April 1 to September 30 this year. This latest update throws the original ‘no additional interest on deferred HP loan payments’ point as outlined in this story out the window.

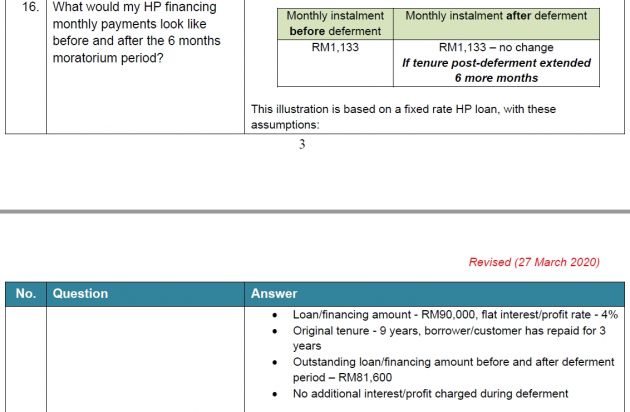

From April 1, all conventional hire purchase (HP) car loan monthly instalments will automatically be put on hold for six months. You don’t have to service or repay your loan instalments during this six-month period, and only resume paying from October 1 onwards.

For example, say you’re paying RM1,000 a month now until December 2021. From April 1, you’ll pay nothing until the end of September. Come October, you’ll continue paying the same amount, which is RM1,000, till the end of your loan term, which has now simply been extended by six months to June 2022, with no extra charges.

This payment holiday will be done automatically, so you don’t have to apply or do anything about it. If you wish to continue paying your loan instalments, then you have to inform the bank that you wish to continue payment uninterrupted – some colleagues have already gotten messages about how to do this (see image above).

There’s no interest compounded during the six-month period, because conventional HP loans are already set at a fixed rate, so you don’t pay anything extra. In short, it’s a true payment holiday for all car loans through banks for six months. There’s no penalty, and there’s no catch. There is also the much rarer variable rate HP, which sets things up differently – you might want to check with your bank if the deferment still accrues payable interest.

As for loans from non-bank credit providers, these are not banks and so aren’t tied under the BNM directive, so they’re not bound to offer any deferment. So far only Toyota Capital Malaysia has said that it will, while the rest will look at things on a case-to-case (TC Capital Resources) or customised (BMW Credit Malaysia) basis.

Looking to sell your car? Sell it with Carro.

The more you borrow, more you saved. Ohsem

Mana kunci kereta malaysia ni ni. Shame on you!

Mana kunci kereta P1 & P2 ni ni. Shame ni

What the f*ck is wrong with you

Wtf is wrong with you

Orang macam ko ni tak payah sembang lebih. Memalukan.

Can I ask, what if I overpaid installment for 2-3 months? Will those early payment been out on hold until October 1st 2020?

For my understand, put it simple. Say you got 36 months installment left, you can put on hold installment for the the next 6 months, resume after that, you settle your loan on the 42nd month from now.

You’d overpaid, say 6 months advance, then you have 30 months installment left, and no intention to hold (it’s freedom of choice), then you just continue your monthly or advance payment as usual.

Any financial specialist, correct me if I’m wrong here or any left out.

No. Car loan repayment, if let’s say you pay 2-3 month for this month. the extra 1-2 month will just count as extra pay. you next month still have to pay.

example you have 36 month left, you pay 3 month worth then 33 left months left. you next month still have to pay. or else the bank will give you a friendly call.

No lah. If you already pay upfront 2 months, so for the next two months you need not to pay lorr. But the bank are porofitting from that upfront payment.

many thanks both, I think I better call to Hong Leong bank and ask about this issue.

Any clause to say that bank will cut short the deferment period, say from 6 months to 3 months?

The bank u-turn from 6 months to 3 months.

Let’s say COVID19 problems all settled under 3 months but unfortunately the car owner lost his job and unemployed during 4th month. Jialat liow.

No, unless Bank Negara changes its standing instructions.

What about standing instructions for auto debit.. Will that automatically be on hold and re activated after 6 months?

Yes it isn’t.

Yes would like to know the same. Anybody can clarify for us with auto debit? Thanks

Yes it isn’t. For hire purchase, auto debit = standing instruction.

How about hire purchase at variable rate?

All variable rate … i.e. reducing balance loan, Interest will be charged but not necessary compounded (depends on which bank)

So there’s really no additional interest for the next 6 months if you opt in? Sweet.

Could we just ignore the message and keep paying?

Just keep paying if you so rich

Even rich ppl don want to pay for six months. Cash can be used to their advantage.

What if my hp loan is on a auto direct debit? Do I need to call in to apply?

The image about the text message asking for reply with car plate numbers and your ic numbers could be a scam. Just beware.

Somebodybtold me it is a scam. Cos the bank will not ask for your ic but until i get clarification from the bank, im not going to do anything yet.

It’s real.Coming from the same number of Maybank.The Maybank website alredy mentioning about this sms.Do some research.

Is it apply to all SME conventional and islamic loan?

Know some are effected, so my comment do not apply to them, there are some willing to pay and do not want extension seeing that it effects the cars RV and furthermore like to take advantage of low rates.

I would like to continue auto debit for my car loan monthly instalments

Note to the post. The SMS seem to be scam. I read in somewhere. Can writer verify it?

All bank should be grant the deffer loan automatically

The SMS is not for applying the moratorium. The SMS is for the opposite, tellling the bank you are NOT ACCEPTING the moratorium a.k.a want to pay just like usual.

I just bought and got my car in mid March, haven’t started paying my loan yet since due date is mid April. Am I eligible to this payment holiday too. Thanks.

Yes

Is it confirmed information from the banks that they will not stack on interest based on the extra six months?