We’ve had some time to look at the 2020 Malaysian auto sales figures now, and we spot a trend within the total industry volume (TIV). All things considered – including Covid-19 and the various phases of movement control to suppress it – market leader Perodua and runner-up Proton both had a good year of sales, aided by the government’s sales tax exemption that started in June.

Perodua sold 220,163 units in 2020. While some way off 2019’s record 240,341 units (original 2020 target was 240k), the final tally easily met the revised target of 210,000 units P2 announced in August. Meanwhile, Proton is settling comfortably into the runner-up seat now after regaining the spot in 2019 – one of the few brands that saw sales go up last year, the carmaker did 108,524 units in 2020, an 8.3% improvement.

In terms of market share, Perodua extended its slice of the pie from 39.8% to 41.6%, while Proton’s sales jump earned it a fifth of the market – 20.5% from 2019’s 16.6%. Combined, the national carmakers hold a commanding 62.1% of the Malaysian auto market, the highest 2003. Last year, six out of every 10 cars sold was a Perodua or Proton, but it wasn’t very long ago that the story was so different.

Rise of the imports

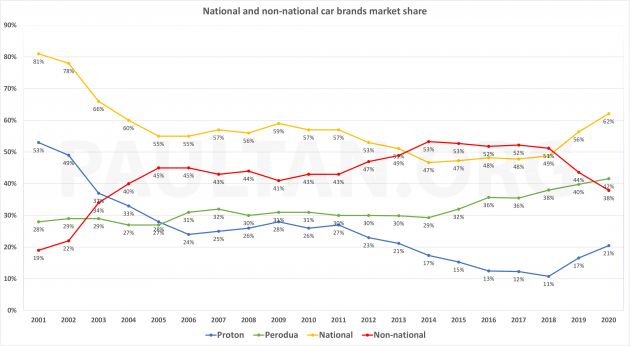

When we were covering the 2014 TIV, the breaking news back then was the non-national brands overtaking Proton-Perodua for the first time ever. Buoyed by an on-form Honda (2014 sales were up 50% year-on-year), foreign brands garnered 53% market share to P1-P2’s 47% (rounded up).

If you look at the trend, the non-national brands taking the lead in 2014 was a matter of time, as they started gaining serious ground from 2011. The national brands’ steady decline was entirely down to the poor performance of Proton. 2011 was the final year that P1 has market share in the high 20s; from there it slid all the way down to just 11% in 2018. At the turn of the millennium, Proton alone controlled over half of Malaysia’s car market, so it’s a spectacular fall.

Perodua’s share of the pie hovered consistently around the 30% mark for a decade beginning 2006. While the market leader was holding its own, the combined national share’s decline still caused concern for P2. Then president/CEO Datuk Aminar Rashid Salleh attributed the shift to market liberalisation.

It was a time when the big three Japanese marques were aggressive in the B-segment, introducing new models with entry prices that encroached into the top end of traditional Proton/Perodua territory. The N17 Nissan Almera in 2012, the “keli” Toyota Vios in 2013 and Honda’s super successful fourth-gen City (and its Jazz sister) in 2014 were all hot sellers. In contrast, the Protons of that period – the Preve C-segment sedan, its Suprima S hatch sister, and the Myvi-fighting Iriz – weren’t sales successes.

In 2016, Perodua chairman Tan Sri Asmat Kamaludin said that a national brand market share of below 50% is not healthy for the local automotive industry. It was a rare strong public statement from a P2 boss.

“While we understand the government’s intention to liberalise the automotive industry in the near term, we believe that the country’s automotive eco-system, consisting of local vendors and dealers, as well as original equipment manufacturers like Perodua, has yet to reach a point where we can fairly compete with other established global brands,” he said.

“This is because we have yet to reach the level of maturity, in terms of economies of scale, cost competitiveness and even quality, with other established global brands. If the percentage continues to slide to below 45% then many of the local dealers and vendors may have to cease operations and this will have a negative impact on the economy as a whole,” Asmat added, stopping short of calling for protection.

Proton, rising from the ashes

Fortunately, the national share never dipped below 45%. Since that statement of concern, Perodua single-handedly took on the imports as Proton continued its slide. If you look at the graph, the turning point for Proton was in 2018, when it reached its nadir of just 11% market share. But the real game changer was the entry of Geely in mid 2017, where the Chinese carmaker took up 49.9% stake in Proton, and took over the steering wheel.

You don’t invest in a company and not push it hard to succeed, and the Geely-fuelled revival was clear for all to see in 2019, when Proton launched improved facelifts of the Persona, Iriz, Exora and Saga. All in one year, which is unprecedented. What more, 2019 was the first full year of sales for the Proton X70, the brand’s first Geely-based product that was launched in December 2018. Internally, they call the four pre-Geely models PIES, and Proton’s share of the pie took a sharp rebound, to 17% in 2019 and 21% in 2020.

Looking at the graph, it’s clear that the national brands’ uptick from 2018 mirrors that of Proton’s revival. Perodua? They’re never the loudest, those efficient folks from Rawang, but they’ve been posting year after year of record sales.

2018 was the first full year of sales for the third-generation Myvi, and P2’s small range (applicable to both vehicle size as well as the number of models) expanded upwards with the Aruz seven-seater in 2019. Those two models, plus the facelifted Axia, propelled Perodua to record 240k sales in 2019. So, it’s clear that Proton’s rise is not at the expense of its counterpart from Rawang.

Instead, both the market leader and Proton are chipping away at the gains the import brands have built in recent times. Let’s take Honda for instance. With a late surge in 2020, it pipped Toyota to be the best-selling non-national brand for the sixth consecutive year, and third overall.

However, the 60,468 Hondas that were sold last year is 29% lower than in 2019 (85,418), which was also a big drop from 2018’s 102,282 units. The all-time record for Honda Malaysia was in 2017, where it sold 109,511 units to breach the 100k per annum mark for the first time. Unless a miracle happens, that will forever be the brand’s high point, much like Arsenal’s Invincibles or Leicester City’s miracle title. Ditto the overall No.2 spot, which Honda somehow managed to occupy for three years (2016-2018).

What does this trend mean for Malaysia’s auto industry? As pointed out by Perodua’s chairman, the rise of national brands will benefit the automotive ecosystem, consisting of local vendors and dealers. P1 and P2 share many local parts suppliers, and higher volumes would be a win-win for all. This is on top of the higher localisation rate of national brand cars.

However, the overall pie isn’t getting larger, as Malaysia is a fairly saturated car market. The TIV for 2020 was close to 530k units, and while the Malaysian Automotive Association (MAA) is forecasting 8% TIV growth this year (to 570k), growth is projected to moderate to 3.0-3.2% from 2023 to 2025.

The new normal?

If the pie isn’t expanding much, the rise of the national brands would mean that the non-nationals will have to get used to a smaller shared portion.

Honda, for instance, is not likely to be a 100k per annum company again, and will have to scale its business here accordingly. CKD operations require a certain volume to be sustainable, and if the sums don’t add up for local assembly, they may just avoid the hassle altogether and import from sister factories in ASEAN. Toyota has already done that – the Camry and Corolla sedans used to be locally assembled, but are now CBU imports from Thailand.

Needless to say, with less CKD projects, the need for local parts and staff would also decline. For consumers, carmakers going the CBU route would translate to higher prices, and/or less equipment, depending on the price strategy for the model.

Personally, I find the Toyota C-HR to be the best illustration – it has looks, X-factor and even driver appeal on its side, but the price gap/value between the CBU Thailand C-HR and the Melaka-assembled Honda HR-V was too big to ignore for most SUV punters. Ultimately, this would mean less choice for the carbuyer. However, this only applies to the mass market non-nationals; the premium players are used to small scale assembly.

Expect this national vs non-national gap to further widen in 2021, as the long-awaited Perodua D55L SUV is set to debut this year. Proton has said that it is capable of launching one new product every year, and there are rumours of either a C-segment sedan, MPV or big SUV joining the range this year. Even if a new model doesn’t materialise, this will be the first full year of sales for the hyped X50.

AD: Drive the Proton model of your dreams. Submit your details and Proton PJ will get in touch with you.

Looking to sell your car? Sell it with Carro.

Perodua Traz

from RM 76,100

Perodua Traz

from RM 76,100  Perodua QV-E

from RM 80,000

Perodua QV-E

from RM 80,000  Perodua Axia

from RM 38,600

Perodua Axia

from RM 38,600  Perodua Alza

from RM 62,500

Perodua Alza

from RM 62,500  Perodua Myvi

from RM 46,500

Perodua Myvi

from RM 46,500  Perodua Ativa

from RM 62,500

Perodua Ativa

from RM 62,500  Perodua Bezza

from RM 34,580

Perodua Bezza

from RM 34,580  Perodua Aruz

from RM 72,900

Perodua Aruz

from RM 72,900

2021 belongs to Perodua Rocky D55L SUV …

You forget that Proton’s new MPV will await to continue their slaughter on the car market as did X50 & X70 prior.

Fuh. “….slaughter…”. Ayat dia memang powder. Tapi kalah jugak kat Perodua. Peee lah.

2020 and 2021 still belong to covid la.

Congratulations to Perodua and Proton

Almost 90% market is actually dominated by UMW (T, P2) and DRB-HICOM (H, P1).

My friend who had an accident with his Proton X70 could not get a replacement front bumper and was advised to wait 2 months for the part to arrive. This is a local assembled car with a vast pool of local parts manufacturers. So, why is there an issue to get a replacement front bumper.

Various automotive bumpers have been made in Malaysia for years and this is not a high technology item like a computer chip or an engine part. The issue of long waiting time for exterior parts for the Proton X70 is not new. So frustrated when decided to trade in my previous BMW 330e for this local Proton X70.

Akoolm,is it your x70 or your friend”s ?Anyway,x70 bumper replacement problem is not new.

The problem is not Dr.Li at proton.

The problem is due to the dead wood from the DRB faction.Remember they own half of P1 ,but allow Dr.li to be CEO.

You cant expect Dr,li to put his head into every detail like spare parts.It is the besok lusa tidak apa dudes thats spoiling the party. [

the dead wood from the DRB faction. Very simply, langsung tak berkaliber & not competent to the max. They should be fired now! let others & young dudes to make it work.

these besok lusa tidak apa dudes, made other ppl lifes the owners so feddup & inconvenient. just when chances are given to protong. (

Yeah again with creating the fake stories and replying yourself. Don’t you ever get fedup when people raised the jig on what your up to?

Non national brands kena sapu d by the government. So much for trying to woo investment into the country but in the end go give the best package to Proton behind closed doors. Don’t cry when the non national brands start scaling down production and cut jobs since it’s more economical to import vehicles from Thailand or Indonesia. Why continue when you can’t make enough money despite all the massive investments? ROI out of the window.

If both Perodua and Proton are doing well, most non-national companies will do better too. I say this because most of our 600+ automotive vendors are directly or indirectly supported by Perodua and Proton. P1 and P2 spend the most on local parts and R&D, and hire the largest workforce (many of which go on to work with other auto companies both local and foreign).

On the other end, the vast majority of non-national companies here depend on the same few vendors for their CKD assembly ops. For example, the engines in some CKD Toyota models are sourced from Perodua’s engine plant. Only a few large vendors, like UMW’s Toyota Auto Body and Tan Chong’s APM are not dependent on P1 or P2 (but they still supply parts to them).

If things become unsustainable and unprofitable, Perodua and Proton can shut down their plants and downgrade their operations to a CBU only business model. If this happens though, it will be the end of our auto industry as we know it.

My point is, the ‘Perodua’ and ‘Proton’ names may live on indefinitely (in Malaysia at least), but our auto industry may not. Whether our auto industry remains sustainable moving forward will depend on the competitiveness of the local vendors, and by extension, the competitiveness of P1 and P2.

On another note, in the coming decades, our auto industry will become increasingly dependent on our E&E industry. Fortunately, our E&E industry is much larger, more export-orientated and generally less affected by government policy. Our faltering auto industry can still reinvent itself by leveraging on our proven E&E industry. No need for flying cars, but rather IoT-enabled self-driving cars instead. P1 and P2 are already moving in that direction with their ADAS systems and ‘Hi Proton’… but we’re still a long ways off from Tesla Autopilot levels.

P1 yes, P2 no. P2 only takes in what Toyota gives them, no development needed whatsoever.

Don’t call Tesla Autopilot, it’s misleading. It’s just driver-assistance system.

another segment our national car manufacturers (p1 and p2) missed is the accessories and modifications. Now chinese company in China has moved on this. We have quite a few innovative designers for our accessories design and development eg headrest “bantal”now fully incorporated in Conti cars, our Mr Zulkifli had come up with rain activated wiper eons before foreign car manufacturers came on board etc. Maybe this is another way we can support our automotive industry?

National cars are getting better the looks and styles now. I can see that the National cars are most on the roads compare to other brands. We Malaysians should support our own National cars. And I’m proud to say that our National cars is improving every year in all aspects. Congratulations.

The very existences of National Cars is the cause of the high prices of non-national brands(Japanese/Europeans/etc).

You could have gotten a Japanese/Europeans/etc car for half the price if it’s not for them. Or maybe even at the same price you are paying now for a Proton/Perodua.

Remember that the next time you purchase a Proton or Perodua.

Higher prices how? In Thailand, Indonesia & Vietnam car prices of equivalent models are pricier than here. Where’s the justification for your statement? Even if it were true, what goes into their cars doesn’t justify the high prices. We still see our national cars with far more safety features and kit included. This is not Proton or Perodua fault, this is from Toyota, Honda, Mitsubishi, Mazda, et al.

Mat, do you even realise the main reason cars from P2 and P1 are cheaper is due to ILP incentives that local manufacturers get for sourcing locally and their R&D spend in Malaysia? If the Japanese or Europeans did the same they would get the same benefits. If Proton or Perodua imported some parts they would get a reduction on ILP benefit. Also, have you taken the TIME Value Of Money calculation in to consideration. A RM90,000 Honda City from 2008 is much more expensive than a RM90,000 Honda City from 2021. It only doesn’t seem cheaper because the purchasing power of the RM is not lower and our growth in oncome has not matched the increase in living expenses. Look at what Danny wrote about the Toyota CH-R vs Honda HR-V and you’ll understand, though in this case, needing to go through TMAP in Singapore who bump the prices up to make a profit before selling to UMW Malaysia is also a contributing factor.

MAT I agree with you Proton n Perodua now have more stylish design n afordable price for advanced technology,even Perodua rebadge with Daihatsu & Toyota but Perodua have more stylish design n more technology from Daihatsu & Toyota.Actually,we have great & intelligent car designer for Proton & Perodua n we can export to global market.We know Proton have stylish & luxury look design & Perodua have affordable price.So it great for global market.

No surprises that Proton’s growth did not come at Perodua’s expense, after all Proton had long moving up the segment chain to compete with non-nationals. This results show ample proof that Proton can take them on and come out victors. Perodua bila lagi? Still crowing the bottom feeder segment?