In August, the Malaysian Automotive Association (MAA) announced that it was changing the format in which vehicle sales data is reported to subscribers, switching the frequency from a monthly basis to quarterly, effective from mid-year.

The association released its Q3 2020 data earlier this week, and we’ve reported on the sales breakdown by brand for the months of July, August and September. Now, we take a look at how brands have fared in the first nine months of the year, compared to the same period in 2019.

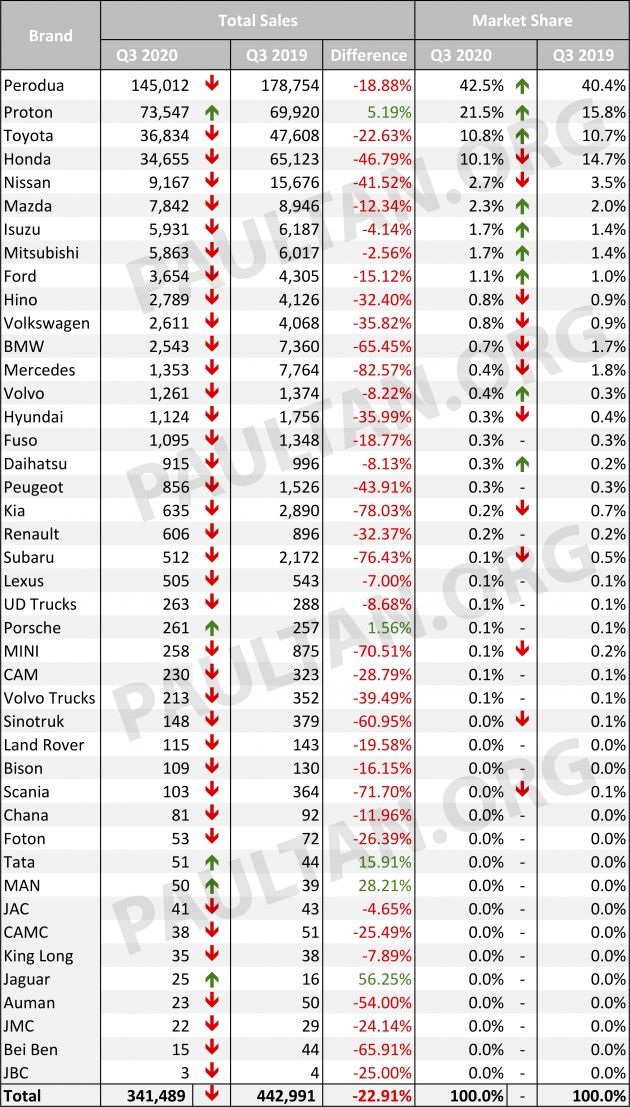

It’s no surprise to find that things haven’t been all that rosy in 2020, as reflected by the sea of red arrows and digits in the accompanying chart. The ravages caused by Covid-19 have been far reaching, both psychologically and economically.

On the automotive front, the numbers would likely be far less than that seen below had the government not announced a SST exemption on the sales of new CKD and CBU cars – until December 31 – to aid the segment.

As things stand, total year-to-date sales for 2020 is at 341,489 units in the first nine months, which is 101,502 units or 22.91% less than the 442,991 units accomplished in the corresponding period last year.

Nonetheless, the third quarter performance has been strong, and has regained a fair bit of ground for this year’s total industry volume (TIV), if you consider that at 1H the TIV stood at just 174,675 units, which was 121,642 units or 41.1% less than the 296,317 units achieved in 1H 2019.

If vehicle sales continue at the pace as seen in the past three months and production/supply can keep up, there should no issue meeting the 300,000 sales target set by the MAA for the second-half of the year. As it stands, total registrations in Q3 amounted to 166,796 units (57,552 units in July, 52,800 units in August and 56,444 units in September).

The Q3 numbers also suggest that the the industry will easily meet the current 2020 TIV target of 470,000 units that was announced in July, up from the previously-revised 400,000 units MAA had set in May following the coronavirus outbreak and resulting movement control order (MCO). Just over 128,000 units have to be sold in the last three months of the year to reach that goal.

On to the specifics. Market leader Perodua saw its sales contract by 18.88% to 145,012 units from the 178,754 units it managed up to September 2019. Its market share however grew by 2.1% to 42.5% from the 40.4% slice of the pie it had last year. Its revised sales target of 210,000 units for the year should be easily met, if its performance in September – where it recorded its best-ever monthly sales in its history – is any indication.

Only five companies saw a better first nine months this year than in 2019, and two of these were commercial players. In the category which we’re all intent on, Proton was the only major brand to show growth. It managed 73,547 units into September, 5.19% higher than the 69,920 units it achieved in the same period last year.

Its market share has also increased from 15.8% in Q3 2019 to 21.5% this year, and notably, national brands now have 64% of the market share. With its new X50 SUV set to hit the showrooms at the end of the month, the last two months looks full of promise for the brand.

In Q1, Honda was ahead of Toyota, but the latter has now overtaken it into third in the overall standings. While Toyota’s sales are 22.63% lower than last year, its 36,384 units managed so far this year puts it ahead of Honda’s 34,655 units, which is 46.79% less than the 47,608 units it did up to Q3 last year.

Nonetheless, the fight for third isn’t done and dusted, because Honda outperformed Toyota last month, and the race to the tape still has three months to be counted. However, we really won’t know until early next year how both have finished, because the actual sales breakdown will only be known when the next data set for Q4 (October to December) is circulated in January 2021.

Elsewhere, others showing significant year-on-year contractions included Nissan (-41.52%), Peugeot (-43.91%), Kia (-78.03%) and Subaru (-76.43%). As for gainers, the two other brands in the passenger car segment that showed growth in a soft year have been Porsche, which has sold 261 cars so far in 2019, up by 1.56% from the 257 units it did in 2019, and Jaguar, which now has 25 registrations this year, a 56.25% increase from the 16 cars it sold up to Q3 2019.

Finally, mention has to be made about Mercedes, BMW and MINI numbers and the high percentage drop for them in the chart. Mercedes-Benz has stopped reporting its numbers since the earlier part of the year, and BMW – together with MINI – had said it was switching to reporting on a quarterly basis. However, it looks like it too has stopped reporting numbers, because Q3 has come and there is no update in sight.

Looking to sell your car? Sell it with Carro.

Habislaa MAA, market slows… emergency.

Proton buck the trend and skyrocket upwards while everyone else fell down. Now with X50 incoming, sales will go thru the roof. Well done Proton!

Copy paste: “Tak payah pikir, tak payah pening, beli X50”

This October, City, Jazz, HRV, BRV and Civic will be eaten by X50 soon

Congratulations to Perodua and DAIHATSU Toyota JDM, growing to 42.5% + 10.8%

Congratulations to Proton, Geely China, growing to 21.5% and Volvo 0.4%

Perodua market share growing 2.1%, sales drop 18.88%; Toyota market share grow 0.1%, sales drop 22.63%.

Proton market share growing 5.7%, sales up 5.19%; Volvo market share grow 0.1%, sales drop 8.22%.

Honda market share dropping 4.6%, sales drop 46.79%

is time to go Maa freeloaders… only main tikam with tiv sales no. my cucu excel way better beb

Among the top ten, only Proton performed better than last year and Jaguar has improved a lot.

SST exemption Conlanfirm will extend to next yr, just like cmco. Unless the ministers want the automotive industry to da bao faster. Rm 50 on the table now!

Used car dealers lah the one who improve a lot.

Now Proton sale figures are half from Perodua although Proton barely giving pure 10% SST discount compared to Perodua.

Overpriced Proton?

Still a better buy than Volvo

For those who cannot afford a Volvo can buy the Proton and if for those who still cannot afford a Proton better buy the Perodua .

Buying a new Perodua is better and problem free compare to buying a second hand worn out Toyota or Honda.

That’s because PROTON didn’t add back SST to the price of its local cars (Persona, Iriz, Exora and Saga) after the zero GST period in 2018. The company absorbed the tax. They can’t afford to do it for the X70 due to the lower ILP so that’s why you see a bigger savings for the SUV,

Ya’all know it’s YOLO time when people starts buying their dream car Porsche & Jaguar.