The Covid-19 pandemic has changed many landscapes, and the automotive sector has been one of them. Nowhere is this better reflected in numbers, with the sales data from the first half of 2020 and this year from the Malaysian Automotive Association (MAA) showing the definite impact the outbreak – and resulting measures taken to keep it at bay – has had on the industry.

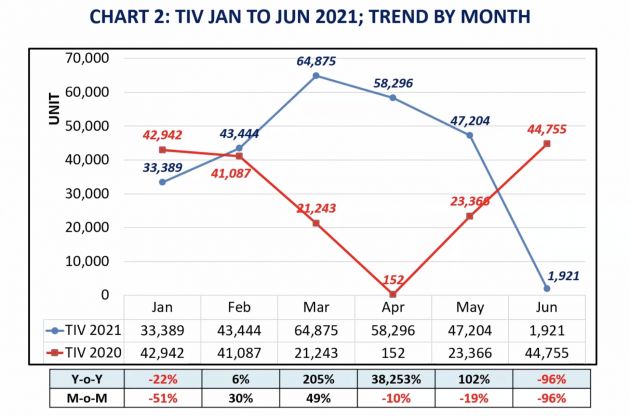

No one could have foreseen what was coming at the start of 2020, at least not the scale or the severity of what would eventually transpire. At 42,942 units, sales in January 2020 began on a softer note compared to the end of 2019, but generally par for the course. February, despite being a shorter working month and with Covid-19 reticence starting to occur, still held up.

Sales in March were impacted following the implementation of the first movement control order (MCO) on March 18, but momentum from the earlier half of the month still carried it to a 21,243 unit result. With all showrooms in the country closed as a result of the MCO, sales in April tanked by 99.2% to just 152 units (orginally reported as 141 units), the worst performing month ever seen by the industry.

By May, sales had resumed, and despite a shorter month for registrations (the road transport department (JPJ) only resumed handling new passenger car registrations on May 13, resulting in a short month for the process), 23,366 units were shifted that month, translating to a 15,272% improvement over April.

The government’s announcement of a sales tax (SST) holiday, made at the start of May and which has since been extended until the end of 2021, undoubtedly helped numbers swell back – in June, 44,755 cars were sold, which was almost double (91.5%) that of May.

Comparatively, 2021 began on a softer note with 33,389 units, not surprisingly given the disruption from the re-implemented MCO on January 13 as well as from sales having been brought forward to December 2020 ahead of the anticipated end to the SST exemption, which didn’t happen, resulting in lower stocks in January for some companies.

That 22% deficit (vs January 2020) was quickly offset by strong growth in February (43,444 units, +5.74% vs Jan 2020) and a booming March (64,875 units, +205.3%). This put Q1 2021 TIV (141,708 units) ahead of Q1 2020 (105,272 units) by 36,436 units, or 34.6%, well on course to achieving the Malaysian Automotive Association (MAA) 2021 TIV forecast of 570,000 units made in January.

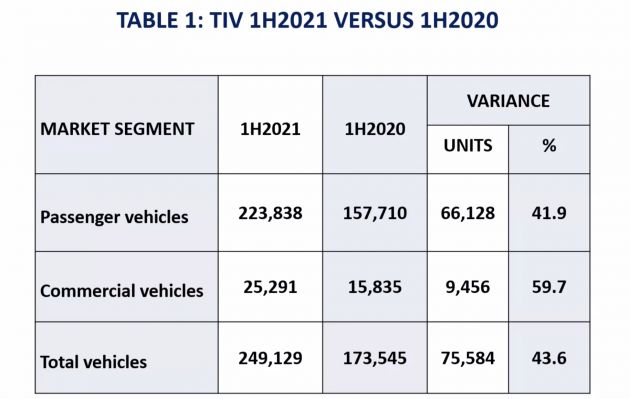

That has gone out of the window at the halfway point. Based on second quarter results (107,421 units delivered, -24.2% vs Q1) and continuing developments, the association has revised its TIV forecast to 500,000 units, slightly lower than the 2020 TIV of 529,434 units. The TIV for 1H 2021 stands at 249,129 units, well ahead of the 173,545 units for the same period last year, so on paper the 500k target looks well achievable.

However, the situation on the ground is telling another story. June 1 saw the automotive sector being shut down when the full movement control order (FMCO) came into effect. Sales in June 2021 amounted to only 1,921 units, and with July almost up and showrooms continuing to be closed, the month can be written off from a sales viewpoint.

More importantly, the closure of assembly plants (together with distribution centres and showrooms) until Phase 3 of the National Recovery Plan (NRP) – which now looks to be a good while away given the rise in daily Covid-19 cases – means that even when sales resume, fulfilling demand (which the MAA says there is no shortage of) may be a tall order.

This is especially so for high-in-demand models such as the Perodua Ativa, Myvi and Proton X50, given that there is already a significant backlog in orders for these. At this point, with zero production at nearly two months and counting, the race is on to see how many deliveries can be accomplished before the SST ends on December 31.

As the MAA has put it, the current forecast is based on an assumption that the auto sector will restart in August – if this isn’t the case, it will have to be revised again. Like it has been for more than a year now, Covid-19 looks like it’ll continue to have the final say in many things.

Looking to sell your car? Sell it with Carro.

With 15-20K covid cases daily,SAs will queue up at foodbanks or sell nasi lemak by the roadside,if there is a delay in showrooms opening.

The gomen most likely will reopen the automotive sector when its workforce has been properly vaccinated,with stringent sops.

You cant lockdown the workforce for 6 months ,can you?

There will not be a return to precovidian good times,where some buying is on impulse.

The virus has changed consumer’s behaviour,make no mistake.

YBAjibkor/YBAlbert. This is YOUR comments is it not;

YB Albert on Jul 02, 2021 at 12:23 pm

The saddest reality is the real total lockdown should have been done in mid May.

Why the flipflop? Just stop. Grow up. Handling pandemic isn’t for kiddies that cannot comprehend the necessary actions taken here.

Which is why I said that MAAs lowered estimated TIV of 500k is a a pipe dream. 1H only managed to shift 240k units.

July and August is a write off already with no end in sight. Coupled with production stoppages and supply chain problems and likely a much softer demand from the market. SMEs are dying and the workforce hired by SMEs are dealing with salary cuts and lay offs. Let’s just say consumer optimism is at an all time low.

I would say the industry would be lucky to hit 450k TIV this year.